Life is looking up for the insurance markets.

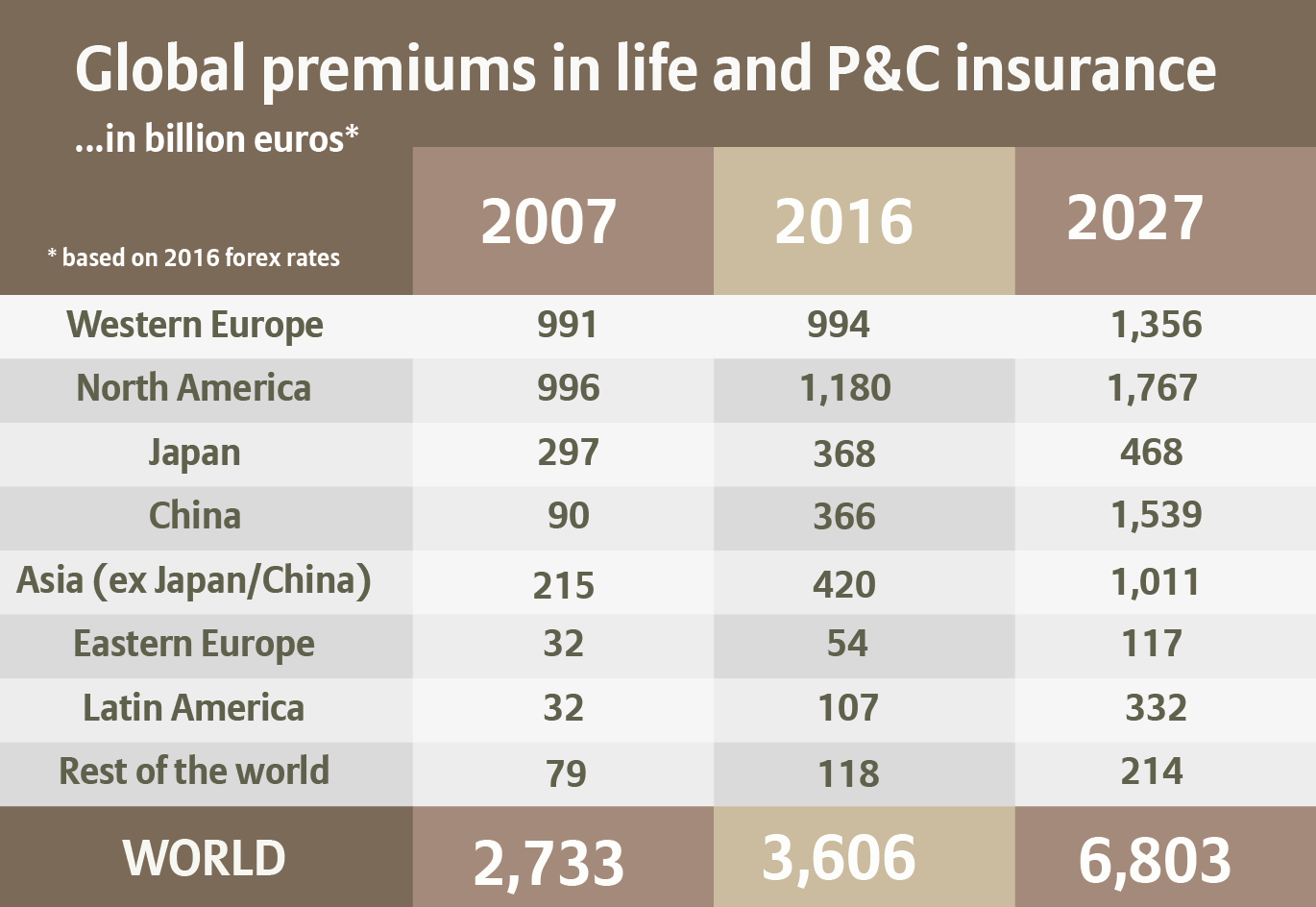

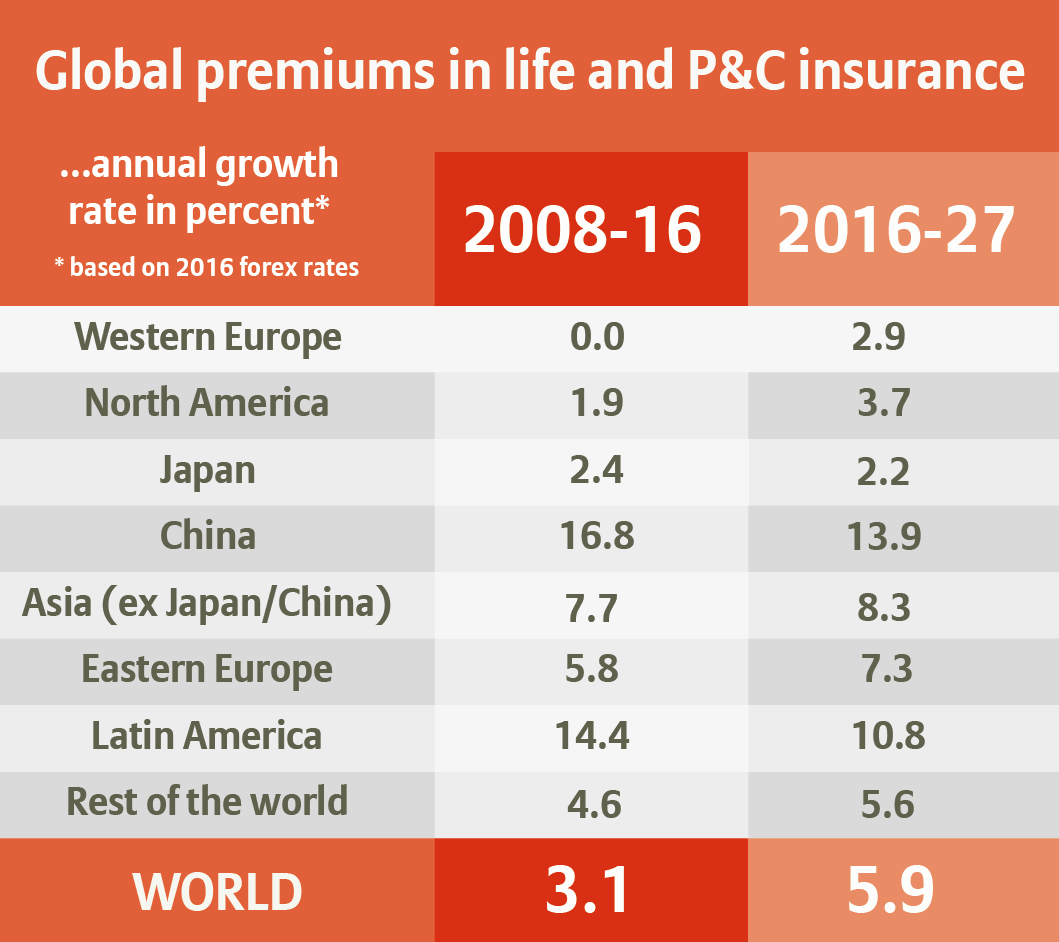

Global life and property and casualty (P&C) insurance premiums are set to grow by almost 6 percent annually over the next decade from 3.1 percent per annum between 2008 and 2016, estimates an Allianz study titled ‘Global Insurance Markets – Current Status and Outlook Up to 2027’.

In value terms, this means the global insurance market could be worth 6.803 trillion euros by 2027 versus 3.606 trillion euros in 2016 – evidence that the global economy is limping back to normal growth and inflation after the financial crisis.

Interestingly, the recovery is most pronounced in mature markets. Emerging from nine years of stagnation, Western Europe is set to grow by 3 percent per annum – Germany’s growth is also expected to be around the same. “The long lean spell of the crisis years is finally behind us,” says Allianz Chief Economist Michael Heise. “In particular in Western Europe, many markets look back at a lost decade, in terms of premium income they are today smaller than before the crisis.”