China: New Technologies, Old Challenges

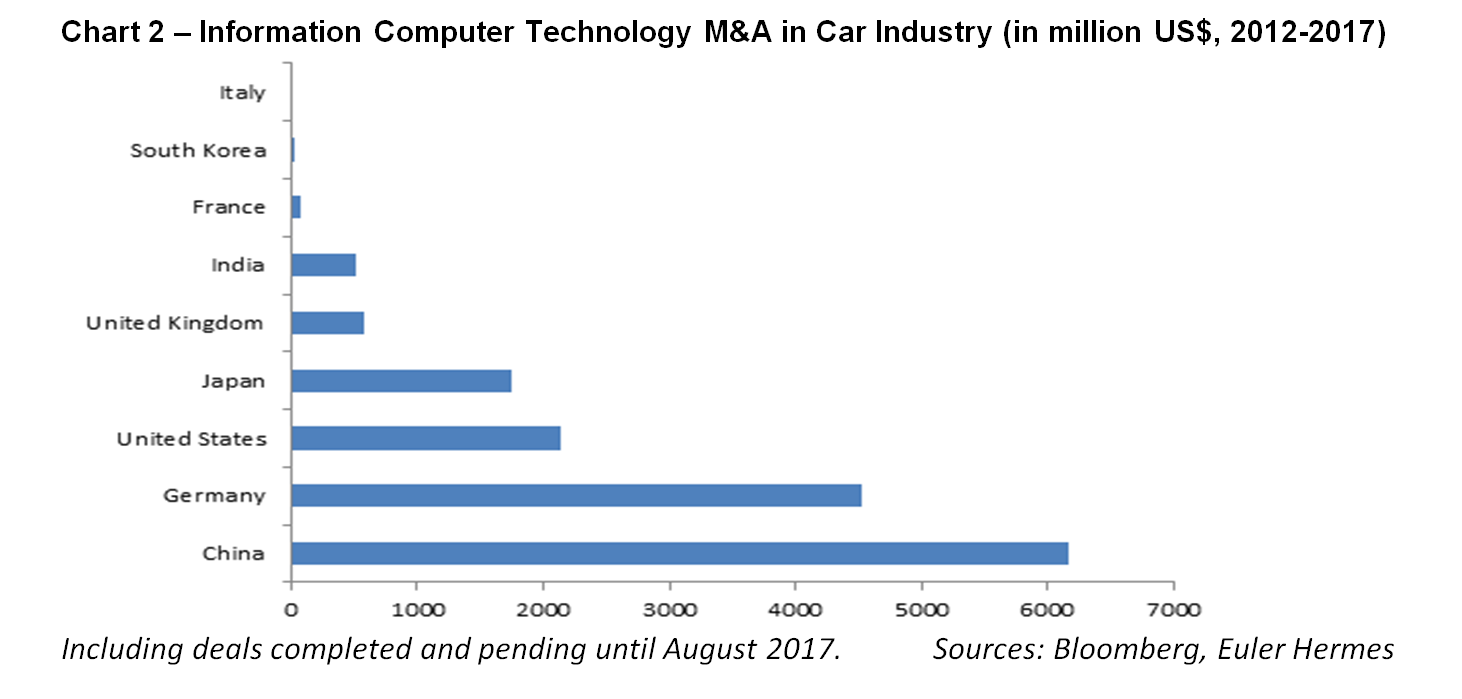

The world’s largest auto market is forecast to expand by +2.0 percent in 2017 and +3.2 percent in 2018. By 2019, more than 30 million vehicles are expected to be sold each year in China. Despite slowing growth from tax hikes on pollutant emissions and the lifting of used-car trading restrictions in January 2017, new sales are expected to grow at a moderate pace due to demand in smaller cities and rural areas. The emerging used-car market in China is forecast to double to 24 million vehicles in 2020 - which could dent new car sales in the medium-term. While leading the way with the world’s largest electric vehicle fleet, consumer demand is supported by a generous 23 percent government subsidy. Aside from battery technology, however, China’s R&D and patented technology lags most advanced countries. Aggressive growth has made China the world leader on Information Computer Technology M&A, with $6.2 billion of deals between 2012 and 2017.

France: Revving Up

Domestic economic recovery boosted sales growth by +4.4 percent year-on-year in the first seven months of 2017, Sales are forecast to grow +3.0 percent in 2017 and +2.0 percent in 2018, to 2.5 million and 2.6 million new vehicles, respectively. French manufacturers and suppliers maintain their strong financial standing with the second most efficient operating cycle in the country panel. French suppliers remain proactive in forging strategic partnerships on connectivity and autonomous driving technologies. In July 2017, the government announced diesel and petrol cars would be banned by 2040. EV sales, including 20,000 in the first six months of 2017, are expected to continue at double-digit growth - currently underpinned by generous subsidies.

Germany: Down with Diesel?

Despite the emissions scandal and cartel allegations seeing diesel market share drop from 46.9 percent in H1 2016 to 41.3 percent in H1 2017, new vehicle sales totaled 2.4 million in the first six months of the year, up +2.1 percent year-on-year. Sales are forecast to grow +2.2 percent in 2017 and +1.7 percent in 2018. The flexibility of German manufacturers, which remain among the most profitable in the world, to switch to diesel alternatives will determine medium-term growth, especially for European sales. As a global leader in engine patents and R&D spending – in 2015, the German automotive industry invested $37.0 billion compared to Japan’s $29.4 billion – electromobility and hybrid driving systems have been a major focus of this shift. Electric car sales, boosted by the diesel scandal, surged by +115.5 percent to 22,453 cars in H1 2017 and are forecast to exceed 50,000 this year.

India: Engines On

With one of the fastest growing automotive markets in the world, India’s vehicle sales are expected to increase by +10.7 percent in 2017 and +13.5 percent in 2018 (4.1 million and 4.6 million units, respectively). Boosting short-term sales, the harmonization of tax form the Goods and Sales Tax launched in July 2017 led to downward pricing in some car segments. Government commitment to infrastructure investment, combined with rising demand from a large and young population, support India’s favorable medium-term growth prospects. Nevertheless, India lags on innovation and R&D spending, while the lack of energy and transport infrastructure has hindered electric car adoption – 10 percent of China’s EV fleet, at 115,000 vehicles by the end of 2017.

Italy: In the Fast Lane

As Western Europe’s fastest growing automotive market, Italy’s new vehicle sales are set to jump by +7.0 percent in 2017 and +5.0 percent in 2018 (2.2 million and 2.3 million units, respectively). Driven by an intense battle for market share and improved consumer and business confidence, high levels of government debt and a looming banking crisis could rein in credit provision and dampen consumer confidence in the medium term. In an industry primarily consisting of SMEs and thus limited financial resources, just 4 percent of worldwide automotive patents were secured by the Italian industry in 2015. R&D totaled 5 billion euros compared to Germany’s 37 billion euros and France’s 6.1 billion euros. With little government promotion and a slowly evolving charging infrastructure, electric cars are at an early stage of adoption in Italy.

Japan: Safe and Sound

After two years of contracting sales, Japan’s vehicle market is expected to grow +2.0 percent in 2017 and +0.2 percent in 2018 at some 5.0 million units per year. Despite the lingering effects of the 50 percent increase in ownership tax for minicars in 2015, sales growth will be fueled by the extension of “eco-car” tax benefits. Global economic recovery and a weak Yen could also boost Japanese car exports in the short-term. Japanese manufacturers are the most profitable car makers worldwide, while being heavy investors in the sector spending 29.4 billion euros on R&D in 2015 and filing 1,854 patents in 2016 – second only to Germany. With generous subsidies to competing technologies from hybrid to hydrogen fuel cell, electric car sales are subdued and in 2016 accounted for just 0.5 percent (24,000) of new registrations.

The UK: Confidence Brakes

Marking the end of five years of strong sales growth fueled by cheap financing deals, new vehicle sales growth is forecast to plunge by -5.0 percent in 2017 (to 3.0 million vehicles) and -6.0 percent in 2018 (to 2.8 million). While plummeting used car prices have had a dampening effect on new vehicle sales, both markets have slowed markedly since last year under persistent Brexit uncertainty, the weak exchange rate and waning business and consumer confidence. With half of cars produced in the UK exported to Europe potentially impacting sales already, there may be secondary consequences with the bulk of the sector’s funding provided by EU R&D investment. It appears Brexit will continue to loom large, particularly in a sector where British R&D totaled just 1.8 billion euros in 2015 – the lowest of the countries reviewed. Nevertheless, electric vehicle sales, subsidized at a below-average 15 percent, have benefited from the government’s ban on the sale of diesel and petrol cars by 2040. Despite a patchy charging network, EV sales are expected to expand at a solid double-digit growth rate.

The U.S.: Growth Sputters

Facing a major shift, the U.S. auto market is expected to shrink by -2.5 percent in 2017 (17.4 million sales) and -1.8 percent in 2018 (17.1 million). Auto loan defaults have been surging, denting credit lending and sales; a booming used car market is putting downward pressure on pricing and declining consumer demand for new cars. Swelling inventories are also contributing to declining profit margins for car manufacturers. The U.S. remains a global innovation leader, especially for battery technology patents. In 2015 R&D totaled 16.8 billion euros, putting the country third after Germany and Japan but ahead of both on worldwide patents - at 29 percent compared to 23 percent and 15 percent respectively. Below average government support for electric vehicles and varied adoption across states has left California far out in front with significant tax incentives and fast charging networks.