Today, Allianz unveiled the fifth edition of its "Global Wealth Report", which puts the asset and debt situation of private households in more than 50 countries under the microscope. Based on the findings of the report, the global gross financial assets of private households grew by 9.9 percent in 2013, the highest rate of growth since 2003. This brought total global financial assets up to a new record level of EUR 118 trillion. Growth was driven by the exceptional stock market performance witnessed in Japan, the US and Europe: assets held as securities gained 16.5 percent - even more than in the years immediately prior to the outbreak of the financial crisis. This is not, however, testimony to a sudden rediscovered passion for equities among savers. The US was the only region in which a substantial volume of fresh funds was pumped into shares or other securities. Europeans, in particular, continued to pull their money out of this asset class.

Allianz Global Wealth Report

Highest asset growth since 2003

Download

Not all regions were able to benefit from the strong growth witnessed last year to the same extent. On the emerging markets, particularly in Latin America, asset growth slowed due to the turbulence on the local capital and currency markets. By contrast, growth picked up speed in North America (+11.7 percent), Japan (+6.1 percent) and also in western Europe (+5.2 percent). This did not, however, prevent western Europe from falling behind Japan last year and coming bottom of the growth league in 2013, with its chunk of global financial assets shrinking by 1.2 percentage points. In a long-term comparison, too, western Europe is at risk of being sucked into a vortex, at least if we look at developments in real terms, i.e. less the rate of inflation: from this angle, per capita asset growth slips back to 1 percent a year since the end of 2000 - which still puts it behind Japan (1.3 percent p.a.). "In an environment characterized by extremely low interest rates, deflation isn't the biggest problem facing savers", said Michael Heise, Chief Economist at Allianz. "The low inflation rates in Europe reflect necessary real economic adjustments and are boosting citizens' purchasing power. They do not justify any further easing of monetary policy."

In actual fact, the ECB's policy is already having a real impact on households in the eurozone. The low interest rates are not only hindering long-term asset accumulation, but are also having a direct impact on income in the form of lost interest income and reduced interest payments on loans. A hypothetical calculation based on the average interest rate level for the period from 2003 to 2008 can be used to put a figure on these income effects. All in all, German households, with their relatively low levels of debt, are left with substantial losses for the period from 2010 to 2014: the "interest rate losses" add up to just under EUR 23 billion or around EUR 280 per capita. The biggest winners, on the other hand, are primarily the southern Europeans, who have benefited from "interest rate gains" of more than EUR 1,000 per capita on average over this five-year period. "It is not surprising that monetary policy has had this effect", said Heise. "The strain that has been taken off debtors in southern Europe, in particular, is very much in keeping with what was intended. But it is important not to lose sight of the side effects of the policy, especially for German investors and their retirement savings."

Germany – growing slower than the European average

In Germany, gross financial assets grew by 4 percent last year - slower than the European average. Since 2007, the last pre-crisis year, the increase has come in at 15.1 percent, which is exactly in line with the European average. At the same time, Germans savers are the only ones to have upped their saving efforts during this period; in all other European countries, on the other hand, asset accumulation has dropped dramatically. "Wealth development in Germany is truly mediocre in the truest sense of the word", commented Heise. "At the same time, the Germans are above-average savers. But it is also the case that almost nobody invests quite as much money with banks as the Germans do, even though bank interest rates are far lower than in the rest of Europe. German savers would appear to be stuck in crisis mode and shying away from making investment decisions. But the "wait-and-see" policy is tantamount to giving money away. Six years after the collapse of Lehman, it's high time to start thinking about the long term and investing again."

It was not only assets which experienced strong growth worldwide in 2013; debt growth (including mortgage debt) also moved up a gear. At 3.6 percent, debt growth was faster than in any other year since the outbreak of the crisis. Nevertheless, the global debt ratio, i.e. personal liabilities measured as a percentage of nominal economic output, fell again slightly last year, dropping by half a percentage point to 65.1 percent. The drop in the debt ratio since 2009 comes in at 6.4 percentage points. This deleveraging is, however, solely attributable to the developed countries, and first and foremost to the US, where 15.5 percentage points have been sliced off the ratio over the past four years. In the emerging markets, on the other hand, the debt burden is rising more or less continuously, also in relation to economic output, particularly in Asia (excl. Japan): in terms of the regional average, the debt ratio climbed by 2.8 percentage points in 2013 alone, pushing it up to almost 40 percent. In some countries like South Korea or Malaysia, the debt ratio is already well beyond the 80 percent mark - putting it ahead of the US level.

This meant that global net financial assets (gross financial assets less liabilities) actually witnessed double-digit growth of 12.4 percent in 2013. In the ranking of the richest countries (net per capita financial assets, see table), some countries switched places due primarily to exchange rate effects, e.g. Japan comes in two places lower. Switzerland continues to top the table with a clear lead over the US. Germany, however, swapped places with Austria and now comes in 16th in a global comparison, with average net per capita financial assets totaling EUR 44,280 at the end of 2013. Nevertheless, no fewer than eight European countries are ranked higher than Germany, including Italy and France.

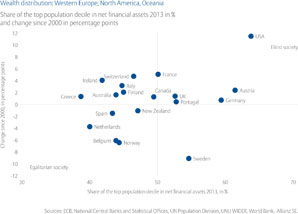

Wealth distribution under the microscope

This year, Allianz has also, for the first time, put the development of wealth distribution within individual countries under the microscope using a "wealth matrix". The results are not necessarily consistent with the theory of ever-deepening inequality. In actual fact, there are more countries among those included in the analysis in which the distribution of wealth has, in the main, not changed much or even improved over the past decade, most of them up-and-coming economies and particularly in Latin America.However, in some big countries like India and Russia the opposite development had to be observed – similar to the situation in the developed economies: Here, wealth distribution has deteriorated in most of the countries included in our analysis, i.e. the proportion of wealth in the hands of the richest ten percent has grown again. Nowhere is this development more marked than in the US. Having said that, inequality has also increased considerably in a number of European countries (France, Switzerland, Ireland or Italy). When asset growth slows in the aftermath of a crisis, this would appear to hit the low and middle wealth categories particularly hard. "The political implications are clear: anyone hoping to achieve more even wealth distribution should not aim to limit asset growth by imposing taxes and levies, but rather to do absolutely everything possible to foster asset growth as a whole. Growth is the best way of achieving social justice", said Heise.

An analysis based on global wealth classes corroborates this heterogeneous picture.1 In 2013, a total of around 912 million people with medium net financial assets lived in the countries included in our analysis. The momentum driving the ascent of the global middle class becomes particularly evident if we look at a longer period of time: since the turn of the millennium, the share of the population that falls into the wealth middle class in global terms has doubled in Latin America, has almost trebled in eastern Europe and has increased seven-fold in Asia. But the rapid growth of the middle class is not a success story for everyone. Particularly in those countries that have set the stage for a massive increase in debt in recent years and whose financial assets have been hit hard by the crisis, there are now fewer people of "high wealth" than there were at the start of the millennium. All in all, a good 65 million people have been demoted from the "wealth upper class" over the past few years. The most pronounced absolute shifts in this direction have been witnessed in the US, Japan, France and Italy - all countries in which the distribution of wealth within the country itself has become significantly "less equal", too.

The number of members of the low wealth class (average net per capita financial assets of less than EUR 5,300) has remained relatively constant in recent years, at around 3.5 billion. This is mainly, however, a by-product of strong population growth. If the trend is adjusted to reflect this natural increase, a true story of advancement can be found lurking behind these figures: almost half a billion people have managed to climb into the global wealth middle class over the past 13 years. "This figure, more than any other indicator, highlights the fact that, in a global comparison, more and more people are managing to participate in global prosperity. So from this global angle, inequality certainly cannot be said to be on the increase", said Heise.

1As in previous years, the "Allianz Global Wealth Report" splits asset owners into three global wealth classes. The global wealth middle class encompasses all individuals with assets of between EUR 5,300 and EUR 31,800.

Top 20 2013 according to…

...Net per capita financial assets

| in EUR | y-o-y in % | |

|---|---|---|

| #1 Switzerland | 146,540 | 6.2 |

| #2 USA | 119,570 | 14.2 |

| #3 Belgium | 78,300 | 4.6 |

| #4 Netherlands | 71,430 | 3.8 |

| #5 Japan | 71,190 | 7.6 |

| #6 Sweden | 70,080 | 12.8 |

| #7 Taiwan | 66,010 | 10.6 |

| #8 Canada | 65,900 | 10.4 |

| #9 Singapore | 64,520 | 5.4 |

| #10 UK | 63,490 | 11.7 |

| #11 Israel | 55,840 | 8.8 |

| #12 Australia | 53,960 | 12.1 |

| #13 Denmark | 53,380 | 6.6 |

| #14 Italy | 48,800 | 2.9 |

| #15 France | 46,020 | 6.0 |

| #16 Germany | 44,280 | 5.3 |

| #17 Austria | 43,740 | 1.8 |

| #18 Ireland | 34,300 | 10.8 |

| #19 Portugal | 22,480 | 8.6 |

| #20 Spain | 21,990 | 22.6 |

Top 20 2013 according to…

...Gross per capita financial assets

| in EUR | y-o-y in % | |

|---|---|---|

| #1 Switzerland | 220,030 | 4.2 |

| #2 USA | 150,780 | 11.0 |

| #3 Netherlands | 121,620 | 2.5 |

| #4 Denmark | 118,290 | 2.7 |

| #5 Sweden | 108,780 | 9.5 |

| #6 Australia | 105,280 | 8.6 |

| #7 Canada | 101,470 | 7.9 |

| #8 Belgium | 98,150 | 4.2 |

| #9 Singapore | 94,210 | 5.1 |

| #10 UK | 93,040 | 7.7 |

| #11 Japan | 92,150 | 6.1 |

| #12 Norway | 78,840 | 6.9 |

| #13 Taiwan | 76,350 | 9.8 |

| #14 Ireland | 72,330 | 2.0 |

| #15 France | 68,890 | 4.0 |

| #16 Israel | 66,910 | 8.3 |

| #17 Italy | 63,900 | 1.9 |

| #18 Germany | 63,850 | 3.8 |

| #19 Austria | 63,510 | 1.0 |

| #20 Finland | 46,470 | 6.7 |

Forward Looking Statement disclaimer

As with all content published on this site, these statements are subject to our Forward Looking Statement disclaimer: