- As the G7 gathers in Japan this weekend, the US is championing outbound investment curbs on potentially sensitive technologies or the outsourcing of critical production as the next step to de-risk supply chains and reduce dependence on China. Presently, China itself, Japan and South Korea are the only economies with some restrictions in place, but they are very limited in reach and scope.

- The US is likely to go ahead first through the passage of a bill in Congress, potentially as early as September or October; other countries will likely follow suit. However, full implementation of outbound investment restrictions will take time given potential loopholes.

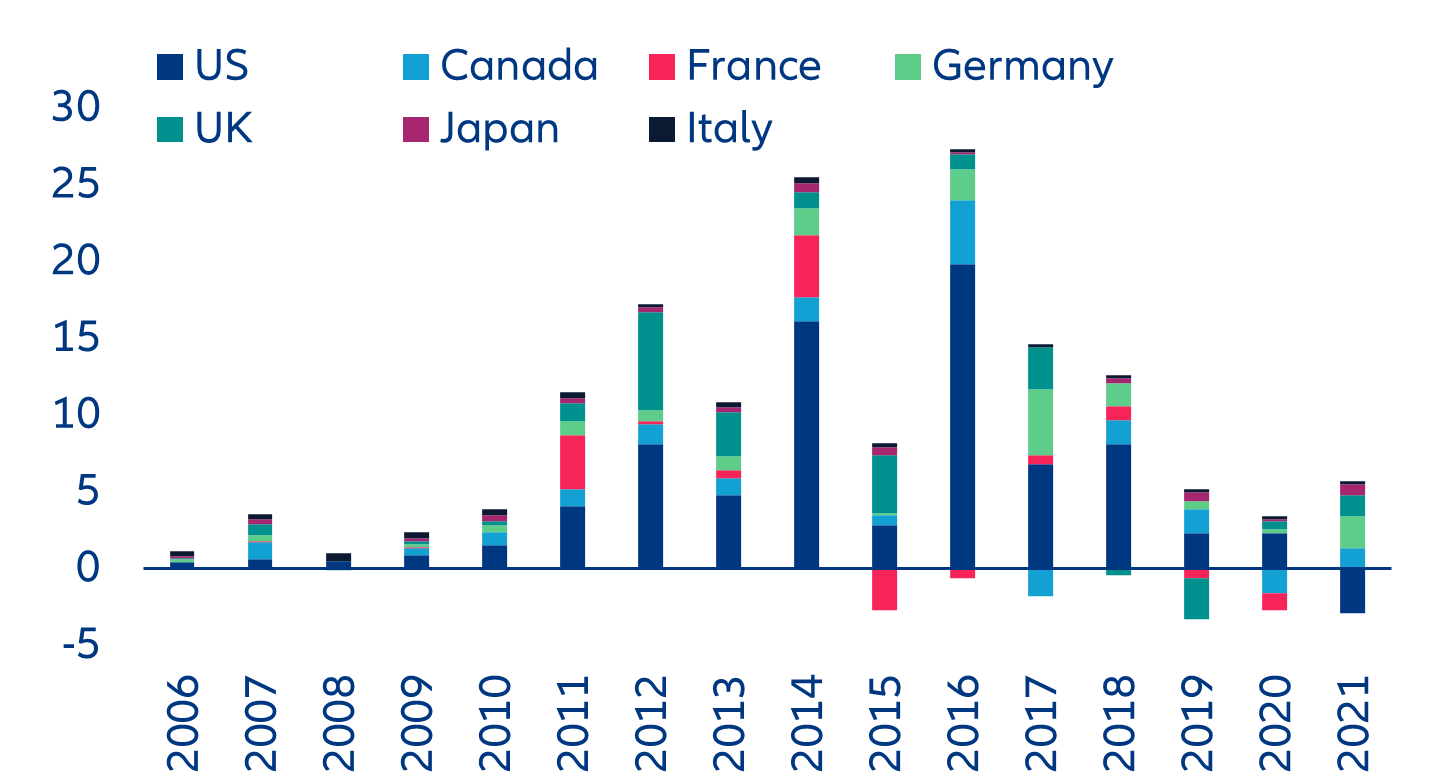

- Two-way investment flows between China and the West are relatively moderate in size and have been declining over the past few years as the private sector has been keen to reduce its involvement amid growing geopolitical tensions. Total FDI flows to China peaked in 2016 at USD27bn for the G7 economies and have since fallen to close to USD3bn, largely led by the US, whose net flows to China turned negative in 2021.

- However, the economic implications of a further decoupling between the West and China could be far-reaching. The long-term damage to the Chinese economy could be far from negligible, even if the restrictions apply to only a handful of sectors. Though Chinese industry has increased its self-reliance, the ecosystem is still benefiting from Western-brought technology and know-how, especially in ICT, pharmaceuticals and biotechnology. China could retaliate by curtailing the supply of critical raw materials in which it has a dominant position, which could severely disrupt global supply chains. But this is unlikely as it already applies some forms of outbound investment restrictions and is still looking towards economic pragmatism (e.g. China has eased some import restrictions on some Australian imports following a multi-year bilateral dispute).

In Focus

G7 in Japan: outbound investment protectionism on the menu

Elections in Greece – key for the return to investment grade

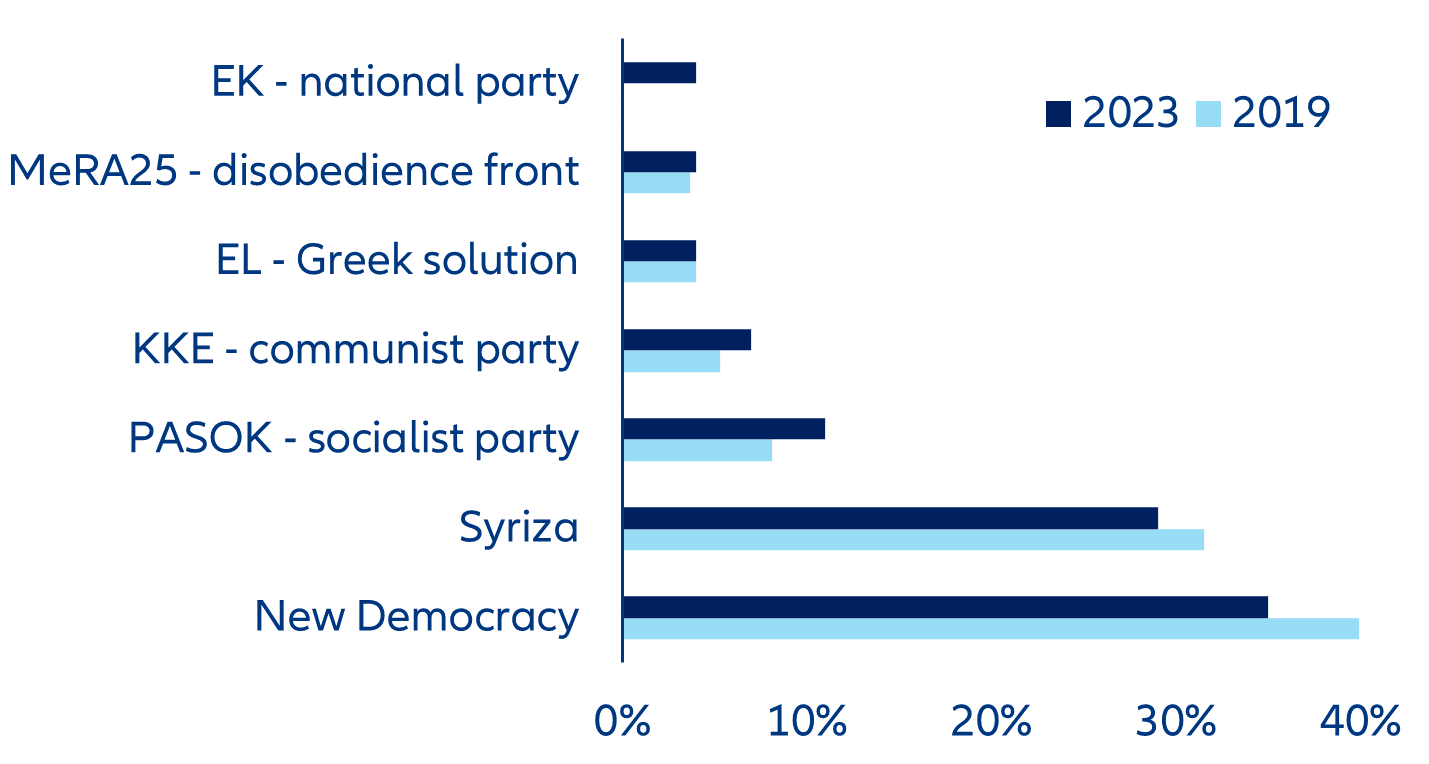

The results of the general elections in Greece this Sunday will be crucial for determining whether the country can maintain debt sustainability and return to investment grade status by the end of the year. The ruling New Democracy (ND) party is leading the polls with 36% (Figure 1) but is unlikely to win an absolute majority as recent changes to the electoral law prevent the winning party from being assigned bonus seats. As a result, new elections are likely to take place at the beginning of July where an ”enhanced” majority will apply, with the first party to get 40 bonus seats named the winner. The most probable outcome will be a coalition between ND and Pasok after the second elections as a coalition between the Siryza (29%) and Pasok parties would probably need more smaller parties to govern. If ND manages to hold on to power, we expect a continuation of current “prudent” and economy-driven policy, with some compromises with Pasok.

Figure 1: Greece - voting intentions as of 12 May 2023

Sources: various official polls, Allianz Research

Any political deadlock could threaten a sustained recovery path. While Greece’s economic output remains lower than in 2008 before the sovereign debt crisis hit, it has recovered impressively over the last three years, reaching 6.4% above pre-pandemic levels at the end of 2022. However, government support to households and consumers equivalent to around 5.2% of GDP caused fiscal dynamics to deteriorate temporarily after years of “forced” fiscal discipline and consolidation.

We do not see material risks of deviation from the “post macro surveillance program” agenda but even a modest period of political uncertainty would weigh on Greece’s economic outlook. Greece is one of the main beneficiaries of Next Generation EU funds but crucial reforms (i.e. financial sector reforms to address private indebtedness and strengthen capital markets or reforms to support the private sector to ease the administrative burden and improve the regulatory framework) will need to be implemented over the next few years to receive the resources. In this context, any implementation delay due to a pause in political activity would delay the positive economic impact. Political uncertainty could also delay the promised return to investment grade by the end of 2023, given that the country’s political and fiscal dynamics heavily influence rating decisions.

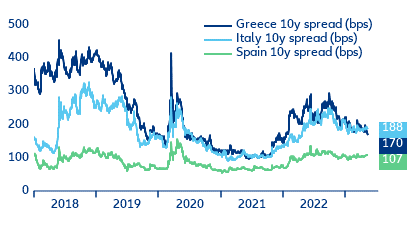

Encouragingly, Greek government bonds are now traded at yields consistent with investment-grade rated countries, and markets do not seem to price in any political turmoil (Figure 2). The largest part of public debt remains in official hands (76% in 2022 from 26% in 2011) and lengthened the average debt maturity to 17.5 years in 2022 (up from 6.3 years in 2011), which mitigates the interest rate burden amid rising policy rates. Still, we expect an increase in the government’s debt burden from the record low levels seen 2022 (2.4% of GDP), albeit not as significant as expected in other periphery countries.

Figure 2: Government debt spreads for Greece, Italy and Spain (at 10-year maturities, bps)

Sources: Refinitiv Datastream, Allianz Research

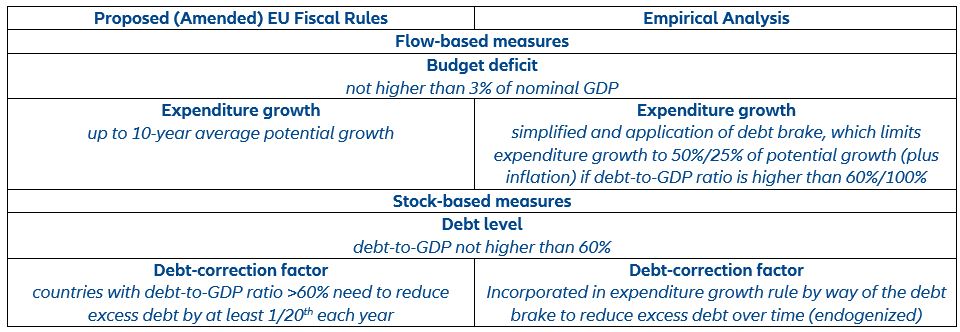

Looking beyond 2023, and in the context of the ambitious overhaul of the EU fiscal rules, the next government will need to prioritize stabilizing its budget balance while making the necessary investments to boost potential growth. Over the last decade, Greece has engineered a remarkable fiscal recovery. However, debt sustainability requires continued fiscal adjustment as the country recovers from both the pandemic and the energy crises. Adherence to the reinstated EU fiscal rules will be critical for Greece to strengthen its fiscal buffers. The new rules offer a country-specific net expenditure path based on simpler rules and with greater flexibility to accommodate necessary spending in priority areas in return for stricter oversight and stronger enforcement (Table 1). For Greece, retaining a focus on growth-enhancing spending will be essential to stabilize debt once current cyclical pressures from the energy crisis abate and give way to structural challenges from the green transition.

Table 1: Overview of amended EU fiscal rules and empirical application for Greece

Sources: European Commission, Allianz Research

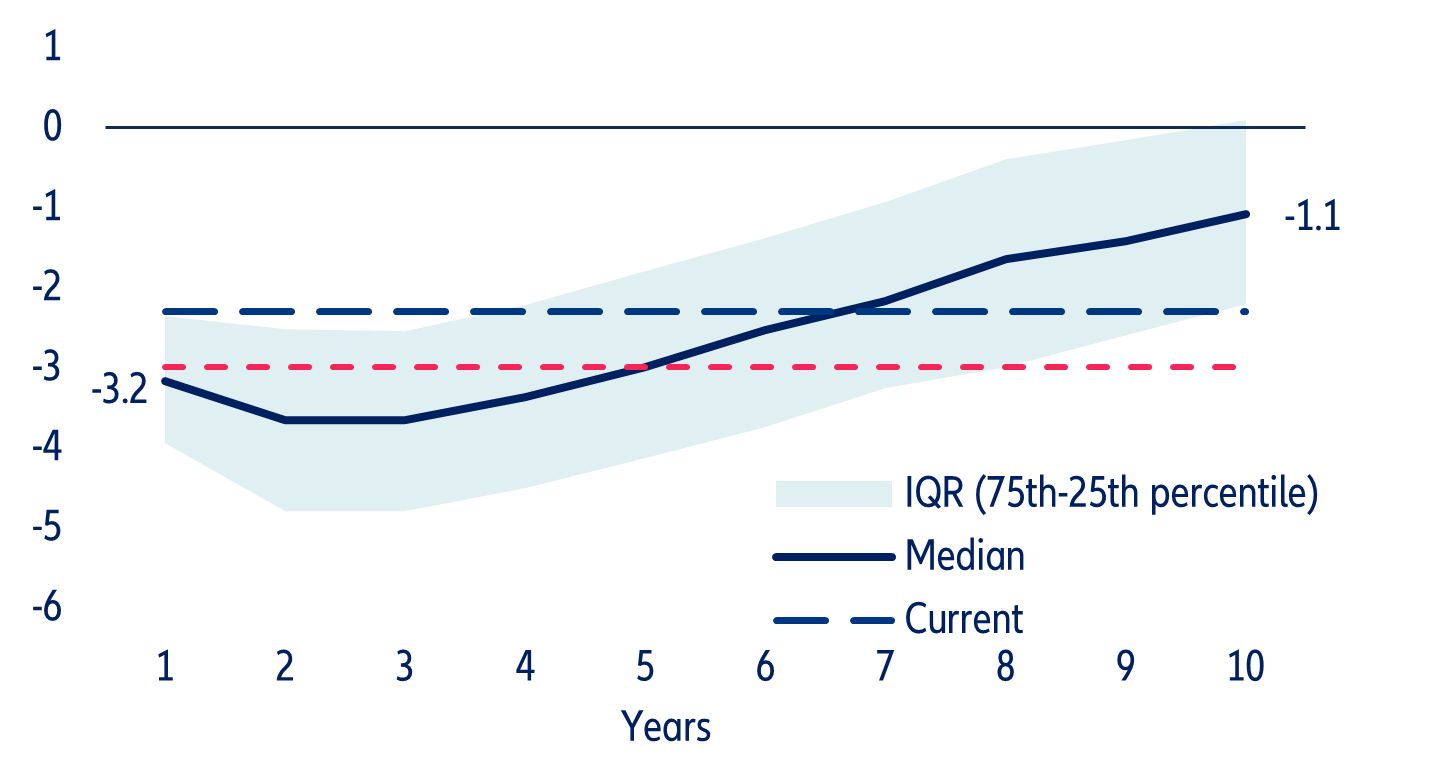

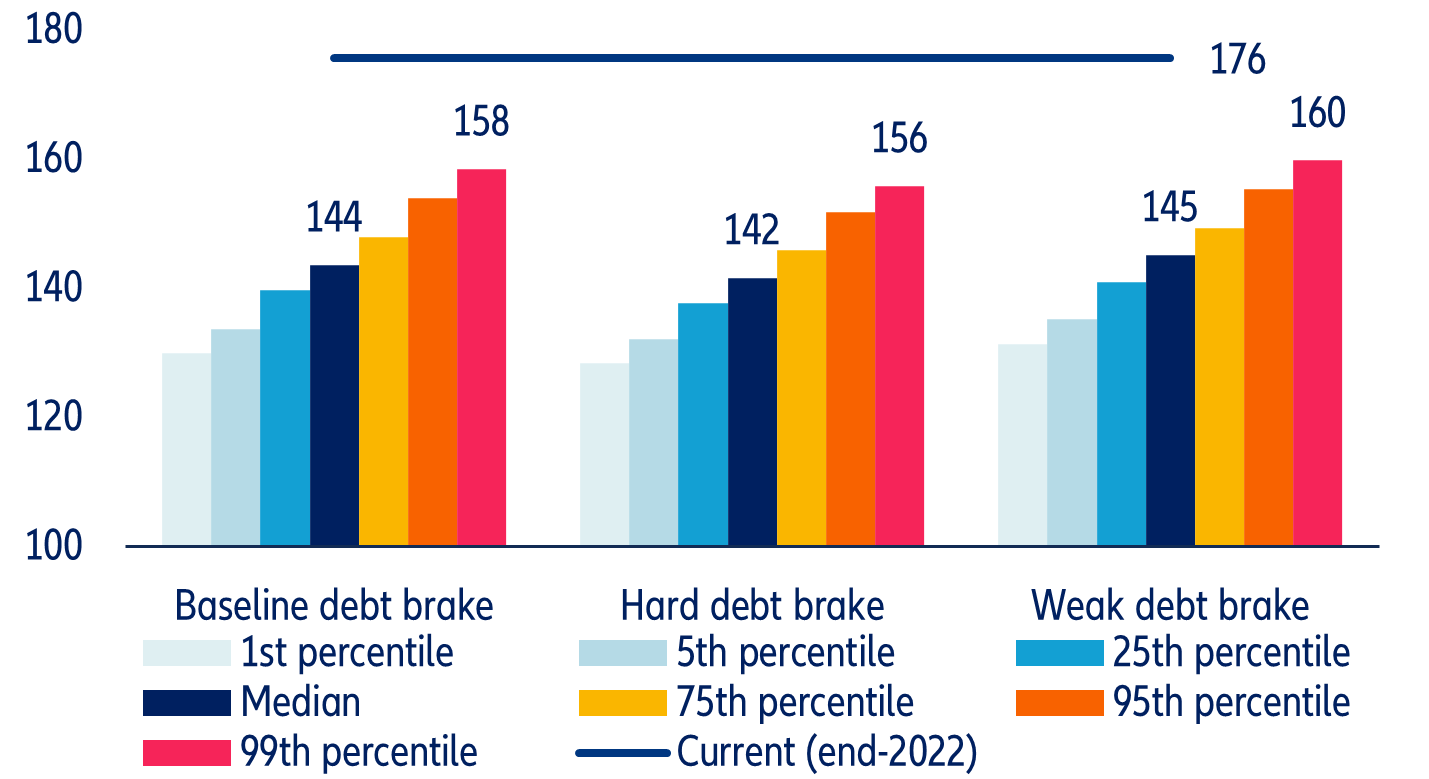

Our simulation results suggest that the EU’s simplified expenditure rule as a single operating target would work well for Greece, implying average real GDP growth of +1.3% per year, in line with potential growth (Figures 3 and 4). This rule significantly reduces the pro-cyclicality and complexity of the current fiscal framework while still guiding the government towards credible debt consolidation. Combining it with a debt-brake mechanism can also provide more flexibility to Greece’s specific circumstances by allowing it a longer adjustment period to reduce excessive debt. Even under an adverse debt scenario (which is modeled based on the 99th percentile density forecast using a Monte Carlo simulation), Greece will be able to further reduce its debt burden by more than 30pps to less than 150% of GDP over the long term. The average real growth under the expenditure rule would also average about 1.3% per year, which is close the country’s potential output.

Figure 3: Greece – Projected budget balance under expenditure growth rule with debt brake (%)*

Sources: Refinitiv Datastream, Allianz Research. Note: */ assumes baseline debt brake, which caps expenditure growth to 50% and 25% of nominal GDP growth if the debt-to-GDP ratio exceeds 60% and 100%, respectively.

Figure 4: Greece – Government debt-to-GDP ratio (10-year average, %)*

Sources: Refinitiv Datastream, Allianz Research. Note: data show the average values under a simplified expenditure growth rule with a debt brake, which caps new spending for the next budget cycle at 50% and 25% of potential growth (plus inflation) for countries with a debt-to-GDP ratio of more than 100% and 60% of GDP, respectively.

Economic uncertainty: Europe paying the high price

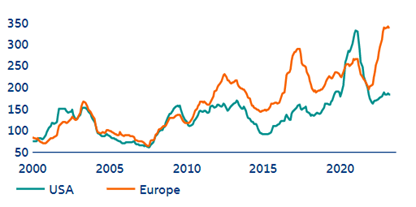

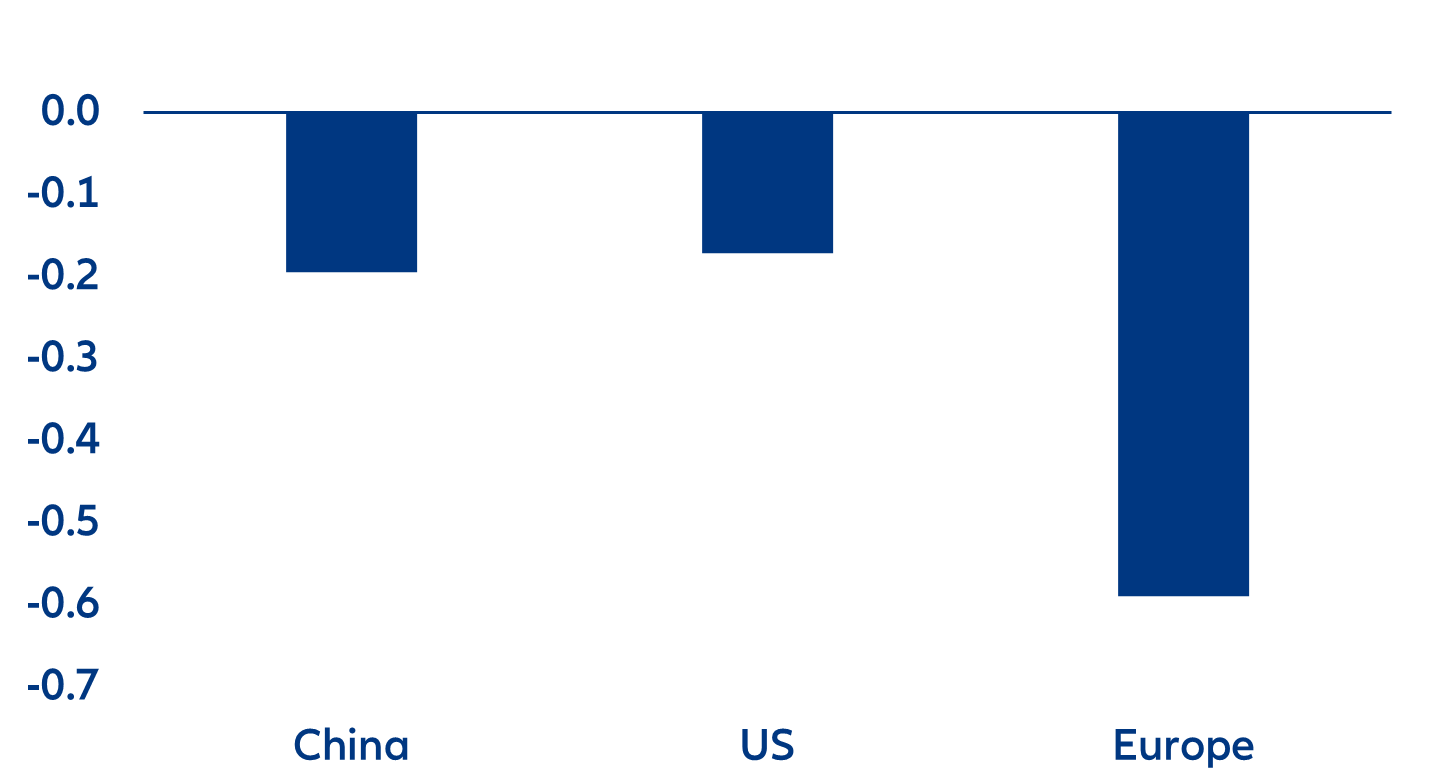

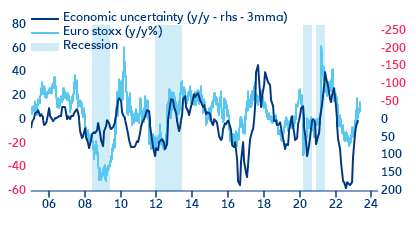

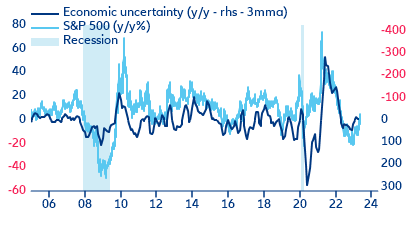

Overlapping crises are keeping economic uncertainty high, with a heavy cost for Europe: At its current levels, we estimate economic uncertainty could cut real GDP growth by -0.6pp by end-2024. Europe is facing a confidence shock twice as big as that in the US, with its economic uncertainty index standing at an all-time high above three standard deviations of its historical values (see Figure 5). With delays in investment plans, higher saving rates and higher inventories, we estimate this economic uncertainty could drag real GDP growth down by -0.6pp by end-2024 (see Figure 6).

Figure 5: Economic policy uncertainty index

Sources: Refinitiv, Allianz Research

Figure 6: Estimated impact of higher uncertainty on real GDP growth, end-2024

Sources: Refinitiv, Allianz Research

Uncertainty: An acquired taste for markets?

Looking at equity indices, we find that investors have been attempting to anticipate a general reduction in broad uncertainty, hoping for a return to a semblance of normalcy. As a result, the stock market has seen surprisingly positive performance, disconnected from traditional measures of value and underlying market fundamentals. Instead, market movements have closely mirrored the cyclical nature of news updates, particularly those related to monetary policy and inflation.

The recent market rally, while beneficial for investors in risky assets, raises concerns about sustainability. Although some justifications can be made, it highlights the potential risks associated with a sudden shift in events or the emergence of an unforeseen "black swan" event, which could swiftly overturn investor sentiment and trigger a significant market correction. Taking into consideration the aforementioned factors and the belief that equity markets will eventually realign with fundamentals and valuations, we see limited room for further upward movement. Instead, it is likely that equity markets will record a stagnant or mildly negative performance from their current levels. In terms of regional vulnerability, European markets appear more susceptible to abrupt shifts in uncertainty levels compared to their counterparts across the Atlantic, mainly due to the relative performance of European equities resulting in a stronger deviation from fundamentals vis -a -vis their American counterparts (Figures 7 and 8).

Figure 7: Europe economic uncertainty vs equity performance

Source: Refinitiv Datastream, Allianz Research

Figure 8: US economic uncertainty vs equity performance

Source: Refinitiv Datastream, Allianz Research

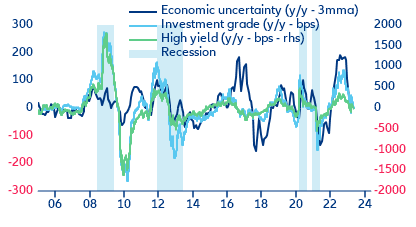

We find a similar story in corporate credit markets, particularly within the high- yield bucket. When considering both equity and corporate credit as two sides of the same risky assets coin, it becomes evident that corporate credit spreads have been and continue to anticipate a return to a more normalized level of economic uncertainty. Notably, US corporate credit appears to be in a more favorable position compared to its European counterpart as European credit spreads appear slightly tighter than what the shifts in uncertainty levels would suggest. However, irrespective of the regional split, and considering our assessment of fundamentals and valuations, we find corporate spreads, especially within the high- yield bucket, to be excessively tight and misaligned with overall economic and fundamental valuations. Consequently, and more abruptly than for equity markets, we anticipate a reversal in spreads towards the end of the year. This reversal is expected to align with the onset of the recessionary environment that will put corporate balance sheets to the test in terms of both income generation and debt- servicing capacity (Figures 9 and 10).

We expect both US and European equities to conclude the year with mid-single-digit positive total returns (around 5%), while investment-grade corporate credit spreads remain range-trading around 150bps for USD bonds and around 170bps for EUR bonds. However, for high-yield corporate credit, we anticipate a widening of approximately 40-50bps from their current levels until year-end.

Figure 9: Europe economic uncertainty vs corporate credit spreads

Source: Refinitiv Datastream, Allianz Research

Figure 10: US economic uncertainty vs corporate credit spreads

Source: Refinitiv Datastream, Allianz Research

In focus – G7 in Japan: outbound investment protectionism on the menu

After reinforcing export restrictions, the US is championing outbound investment curbs on potentially sensitive technologies or the outsourcing of critical production as the next step to de-risk supply chains and reduce dependence on China. As leaders of the G7 countries gather this weekend in Japan, the US is pushing for a G7-coordinated screening of outbound investments to China in specific high-tech technologies. In a speech on EU-China relations on 30 March 2023[1], European Commission President Ursula von der Leyen also declared that the EU is preparing to screen outbound investments related to “a small number of sensitive technologies where investment can lead to the development of military capabilities that pose risks to national security."

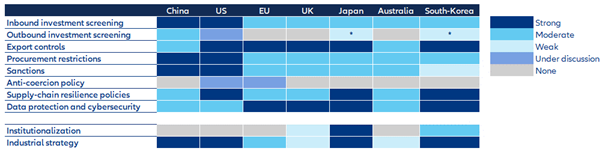

At present, such screening is only implemented by China itself, Japan and South Korea (Figure 11), though on a moderate scale in China and a weak scale in Japan and South Korea. In Japan, the Economic Security Promotion Act aims at securing supply chains and safeguarding home-grown innovation, going as far as subsidizing the return home from China for Japanese companies, the first G7 country to do so. In South Korea, outbound investment is subject to the Act on Protection of Industrial Technology and the screening is done by the Ministry of Trade, Industry and Energy (MOTIE). The aim is to “prevent undue divulgence of, and protect, industrial technology in order to strengthen the competitiveness of Korean industries and contribute to national security and development of the national economy” focusing on sectors such as biotechnology and battery technology (see full list here).

The US, the EU and the UK are, in parallel, said to be discussing a reinforcement of export controls on semiconductors and other critical technology to China. The US tightened export controls to China in 2022 and other countries such as the Netherlands, the UK[2] and Japan have followed suit. Export controls are now being strongly enforced by all major economies (Figure 11 again) and are likely to be extended in the coming years. At the global level, export restrictions reached a record high number of 2,500 in 2022, with more than two-thirds being implemented on goods and the rest as investment and services restrictions.

The restrictions on high-end chips and chip-making equipment exports to China have already led to a dramatic fall in Chinese integrated-circuit import volumes since 2021. US total export volumes of chips and chip-making equipment to China plummeted by -33% between Q4 2022 and Q4 2021. Following last year’s export controls, UK machinery and transport equipment exports to China dropped from 43% of the total to 27% in March 2023 on an annualized basis.

As geopolitical rivalry between the US and China remains high, it is likely the US will impose export controls on new sectors and industries (through the issuance of the so-called ‘Foreign Direct Product Rules’). These could include biopharmaceuticals (where China is highly dependent on US intellectual property), biotechnological materials, technical information and lab equipment (which US firms supply significantly to Chinese facilities) or even agricultural products (eg. seeds).

Figure 11: Economic security measures currently in place and under discussion

Sources: Merics, Allianz Research. NB: * Minor restrictions are in place for foreign banks, weapons manufacturing and narcotics, but they are residuals of processes of economic opening and not full-fledged policies to screen outbound investments

Full implementation will take time given potential loopholes, but the private sector is already reducing its exposure. As pointed out by the PIIE[1], outbound investment restrictions would be tricky to implement and probably create many loopholes. For instance, Western firms could still invest in prohibited critical sectors in China through their foreign-based subsidiaries, or through Hong Kong.

For now, governments are still balancing their desire to curtail technology transfers to China against the concerns of the private sector, which has a high stake in Chinese investments. The US[2] is likely to go ahead first with its own regime to review outbound investment to China later on this fall (the so called “reverse CFIUS”, referring to the Treasury Department’s Committee on Foreign Investment, which reviews inbound investments) but other G7 countries are likely to follow suit. In the US, a bipartisan bill (China Competition 2.0 Bill) has a good chance of being passed by Congress as soon as September or October (after a few failed attempts in previous years). The major industries considered would be microchips, some type of AI related to military and surveillance and quantum computing, but the biotech and clean energy sectors could also be included. The EU faces some constraints with respect to the existing fragmented FDI screening landscape among its member states and will thus likely move more slowly.

Two-way investment flows between China and the West are already on a downward trend. Despite some acceleration in 2021, inbound FDI from China dropped by -77% vs its 2016 peak to EUR46bn due to the increased investment screening in largest European countries. Up until 2020, close to 60% of inbound investments in Europe from China were made in Germany, the UK and France, with the Netherlands gaining traction since 2021 following a large Chinese acquisition. Central and Eastern Europe accounts for around 10% of total Chinese investments in Europe. Most of the inbound Chinese investments are made in the automotive sector and consumer products, but ITC, biotech, pharmaceuticals and the health sector are also gaining traction.

The trend for inbound investments from China in Europe is likely to remain on the downside, not only because of new European regulations (incl. on procurement and foreign subsidies) but also due to reinforced screening by the individual countries. In 2022, Germany, Italy and the UK already blocked several Chinese investments in the so-called strategic industries.

The majority of EU states have already enacted laws to protect their national security. In Germany, the Foreign Trade and Payments Act (Aussenwirtschaftsgesetz) and the Foreign Trade and Payments Ordinance (Aussenwirtschaftsverordnung (AWV)) are in place and concern sectors such as personal protective equipment (PPE), AI, quantum technology, robotics and autonomous driving. In France, FDI control rules are set out in the Code monétaire et financier, and concern sensitive sectors including energy, critical infrastructure, food security, transport, print press, defense, space, AI, robotics, cybersecurity and public health. In Italy, inbound FDI is controlled by the Golden Power Law. In the Netherlands, the Cross-Sector Foreign Direct Investment Screening Act (Wet veiligheidstoets investeringen, fusies en overnames) was adopted by the Dutch Senate in 2022 and targets investments the field of (very) sensitive technology. The UK amended its foreign investment review regime by passing the National Security and Investment Act (NSI Act) 2021. There are 17 sectors within which foreign investments are controlled, mainly concerning high-tech products.

Similarly, outbound investment to China has been on downward trend since 2016 (Figure 12), led by a sharp pull-back from the US. For instance, the outward stock of FDI from the UK in China stood at close to GBP11bn in 2021 (-15% compared to 2018), or 0.6% of total UK outward FDIs. On the other side, inward FDIs in the UK from China stood at only GBP5bn, or 0.3% of the total UK inward FDI stock.

Figure 12: G7 countries FDI inflows into China (USD bn)

Sources: Refinitiv Datastream, NBS, Allianz Research

The big concern is not total FDI flows at stake but rather the supply of critical materials should China retaliate. Outbound investment restrictions in China are more likely to be narrowly targeted in the short term, but to widen in the medium term. The private sector is thus likely to curtail investments from active channels towards China (FDI and Venture Capital investments) further in the benefit of passive channels (buying of financial securities). If the restrictions are coordinated and implemented by major countries or economic areas, it will reduce loopholes and create important regulatory barriers for investment flows into China.

The long-term damage to the Chinese economy could be far from negligible, even if the restrictions apply to only a handful of sectors. Though Chinese industry has increased its self-reliance, the ecosystem is still benefiting from Western-brought technology and know-how, especially in ICT and pharmaceuticals and biotechnology. Western restrictions could thus exacerbate the slowing of Chinese productivity over the coming years, at a time when increased state intervention and political interference are causing widespread misallocation of resources and weighing on the performances of large firms.

However, retaliation by China would potentially inflict severe harm to Western economies, even if direct retaliation has been limited in size and rather selective in the past. Recently, China has eased some import restrictions on certain Australian imports (cotton, copper and coal) following a multi-year bilateral dispute. The stakes are high for Europe as China is the dominant supplier of critical raw materials necessary for the green transformation. Export curbs on critical raw materials by producing countries have increased dramatically over the past 15 years, not least to mention the Critical Raw Materials Act by the EU. New restrictions could severely disrupt key industries, lead to shortages of key products and massively increase prices.