- Over the last decade, zero interest rates in Europe did not hold back growth in private households’ financial assets, particularly in Germany (+5.2%). However, the growth drivers were quite different between countries: Whereas German households relied on fresh savings (mainly out of earned income), most other countries benefited from value gains (i.e. the rising prices of securities).

- We find huge differences between the implicit returns on households’ financial assets, which range from 2.5% in Austria to 6.0% in Finland. Implicit returns refer to the total sum of gains in value and investment income in relation to portfolios. As such, they are an intriguing gauge to visualize the differences in investment strategies. Germany performs rather poorly (3.1%), while France (4.1%) ranks in midfield. In the last two years, however, German savers have started to embrace capital markets, pushing their returns above the average of the group of countries under consideration, resulting in additional savings of around EUR1,000 per capita.

- Returns can act as an amplifier of inequality. In most countries, there is a significant spread between the lowest and highest income groups in terms of returns: they increase – more or less – in tandem with income as higher income groups invest more in higher-yielding (i.e. riskier) assets such as equities. But there is one notable exception: the Netherlands, where returns are very similar for all income groups. This is testament to the role of a strong, capital-funded pension system that can work as a wealth equalizer.

- Looking ahead, savers will need to adapt to a world with higher-for-longer inflation – but the old rules still apply. Rising inflation already ate into returns dramatically in 2021, with the average total return falling by more than -60% in real terms. 2022 will be worse: With an average inflation rate of over 8% in the Eurozone, the real return will be pushed deep into negative territory. In 2023, as inflation is expected to fall from its recent peaks, the situation should improve. Nonetheless, with annual inflation at around 5%, real returns are very likely to remain in the red. Furthermore, as inflation is expected to remain elevated for the time being, it is all the more urgent for households to adapt their savings behavior, focusing on long-term value creation rather than short-term liquidity holding.

Returns on private financial assets in selected EMU countries

Different strokes: asset growth and wealth in the Eurozone

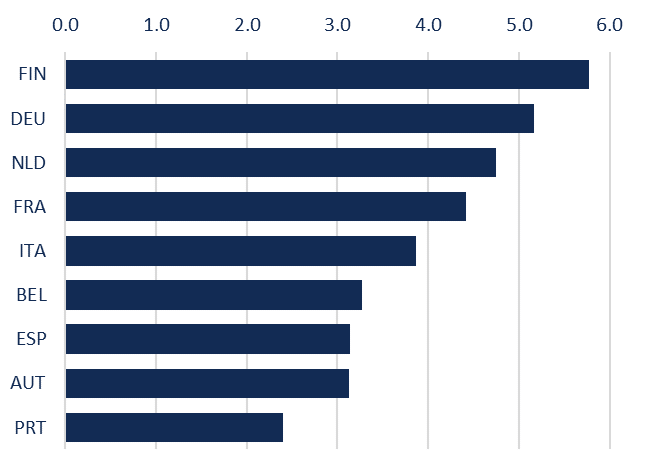

Over the last decade, despite the euro and Covid-19 crises, household financial assets increased in all the seven biggest Eurozone countries we study in this report. In fact, households in Finland and Germany even recorded quite substantial average annual growth rates of more than +5%. At the bottom end of the scale is Portugal, where there, average asset growth was well below the +3% mark, while Austria (+3.1%), Spain (+3.1%) and Belgium (+3.3%) managed to be just above it.

Financial assets per capita*, CAGR 2012-21 in %

*without other equity

Sources: Eurostat, Allianz Research

Sources: Eurostat, Allianz Research