- Over the last four years, Eurozone sovereign exposures to the corporate sector have exceeded 20% of GDP. While support measures have helped keep vulnerable firms afloat, there has been considerable economic scarring – and the risk of higher corporate defaults continues to rise (especially as governments start tightening their belts). Higher public-sector exposures raise the risk of a doom loop as weak growth puts increasing pressure on corporate margins.

- Over the next few years, the Eurozone could become trapped by a combination of weak fundamentals and excessive policy interventions. This exacerbates vulnerabilities from mispriced risk, while underlying fundamentals continue to worsen. But as the credit cycle turns negative (with money supply having turned negative for the first time ever) and fiscal policies become restrictive, the economy must eventually “snap back” to weak fundamentals.

- In an extreme adverse scenario, the complex system of interlinkages between real activity, banks and sovereigns could trigger a fundamental repricing of risk in a new “doom loop”. If we conservatively assume default rates seen in previous crises, a cumulative corporate default rate of 10% over the next two years (up from less than 1% per year) would wipe out about three years of bank profits. Public-sector losses would amount to 5% of GDP on average from direct losses and foregone corporate tax revenues.

- While this scenario remains extreme, it underscores that financial sector policies need to be become more forward-looking, especially in countries where slower insolvencies and lower asset-recovery rates amplify economic scarring, threatening to undermine the financial system and eroding valuable policy space. Pre-emptive policies must also include completing the Banking Union.

In focus – A new Eurozone doom loop?

Eurozone housing market and home affordability – still too expensive

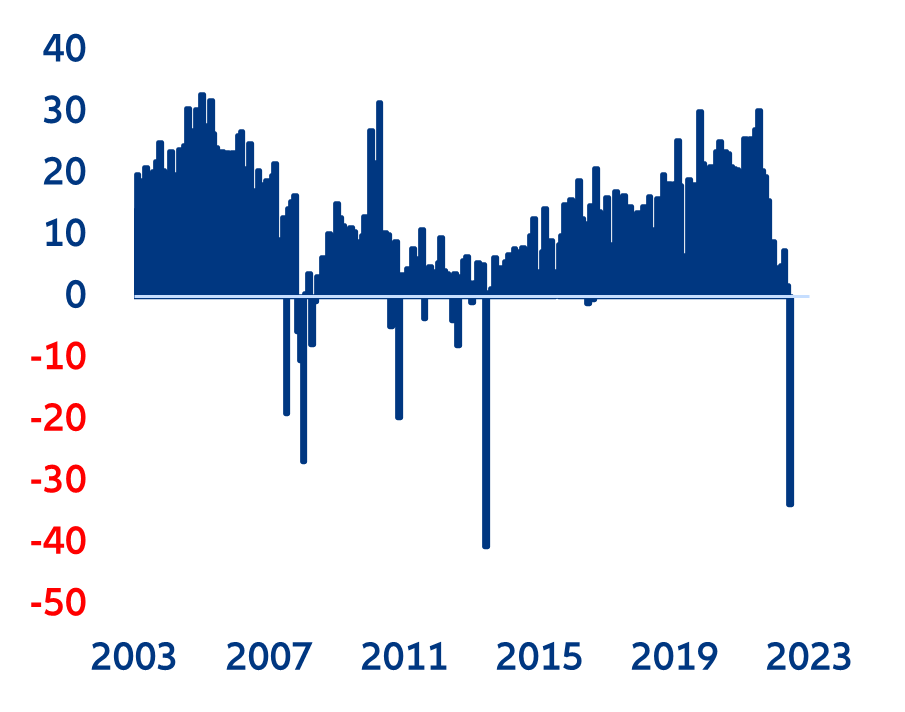

The Eurozone housing market is feeling the pinch as demand for housing loans plunges and the ECB keeps hiking interest rates. Credit conditions keep deteriorating; the ECB is preparing for another 25bps-rate hike (to bring the deposit rate to 3.75%) and the six-month Euro Interbank Offered Rate (Euribor) is about to surpass 4%. While annual loan growth suggests a modest decline (1.8% y/y in May from 3.0% in April), looking at monthly dynamics of household credit for mortgage purposes points to a more alarming picture (-EUR34bn m/m, Figure 1). Demand for loans has plunged as households cannot bear escalating mortgage costs; gross non-financial investment (which refers mainly to housing) decelerated by 5.5% q/q in Q1, down from 6.4% in the previous quarter. We expect this to start to show up in the next European Banking Authority data release later this month.

Figure 1: Loans to households for house purchases (monthly flows) [top] and overall trend [bottom]

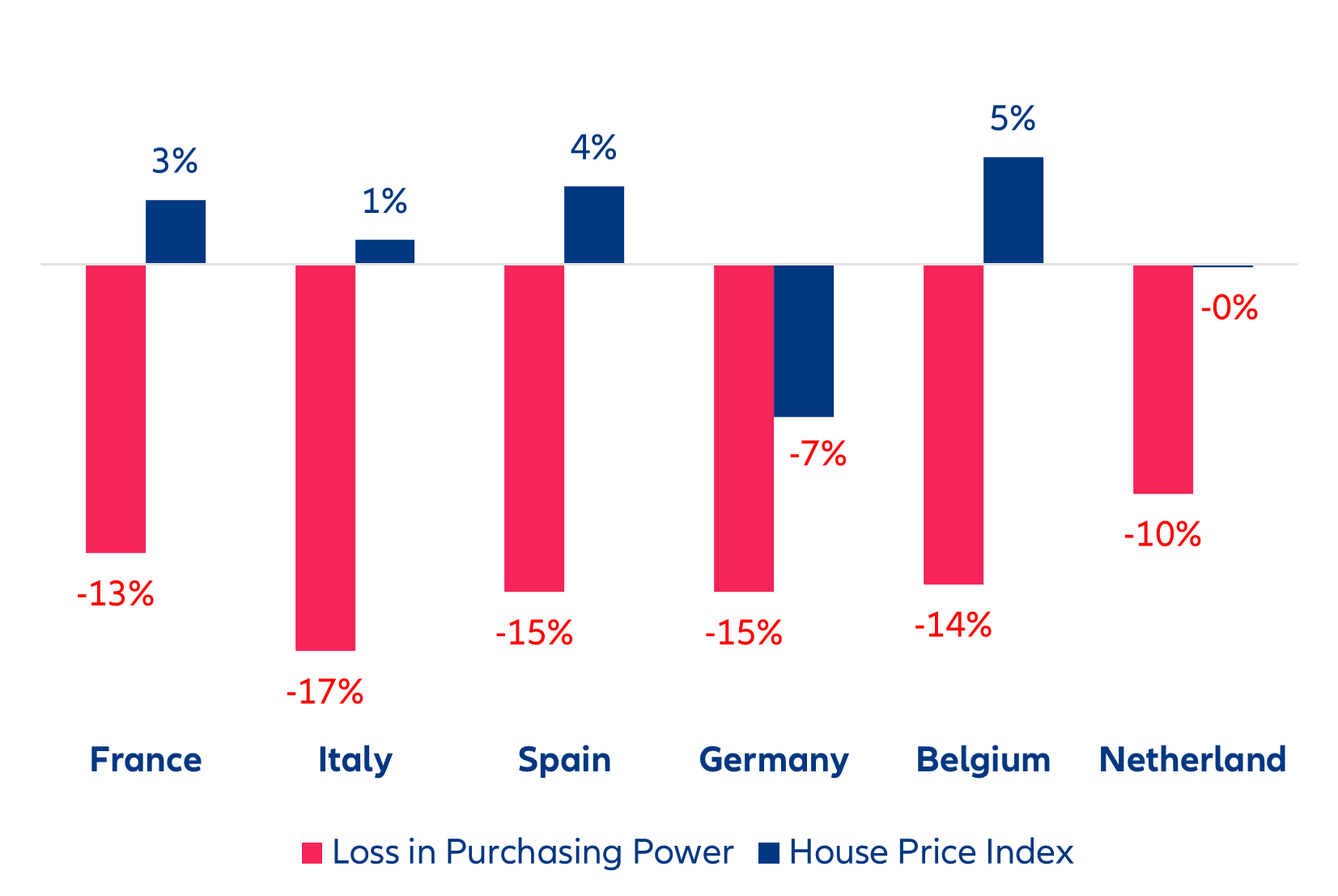

However, despite the shift in market dynamics, the total cost of purchasing a house is still significantly higher than it was before Covid-19. Real house prices in the major Eurozone economies have already contracted between -1.5% (Spain) and -14% (Germany) since March 2022, and we expect further corrections of between 5-10% until end-2024 as financial challenges escalate. But the notable surge in mortgage payments, driven by rising interest rates, has more than offset this decrease and caused a deep housing affordability deterioration across the Eurozone. As a result, the prospect of buying a home is still more expensive than it was a year ago. At the same time, escalating inflation and lagging wage growth are also eating into purchasing power. Looking at a typical 20-year mortgage, we find that the median household lost 13% of purchasing power in France, 10% in the Netherlands, 15% in Spain and Germany, 14% in Belgium and up to 17% in Italy (Figure 2). Considering the change in housing prices, in order to restore the supply-demand balance from 2022, residential house prices need to decline by -16% in France, -18% in Italy, close to -19% in Belgium, -10% in the Netherlands and about -8% in Germany.

Figure 2: Home affordability losses over a year for the median household as of Q1 2023 and change in nominal House Price Index (%).

Sources: ECB, Eurostat, Allianz Research. Note: The loss of purchasing power is computed for a typical 20-year mortgage based on long-term interest rates, national median household income and the maximum repayment set to 35% of income.

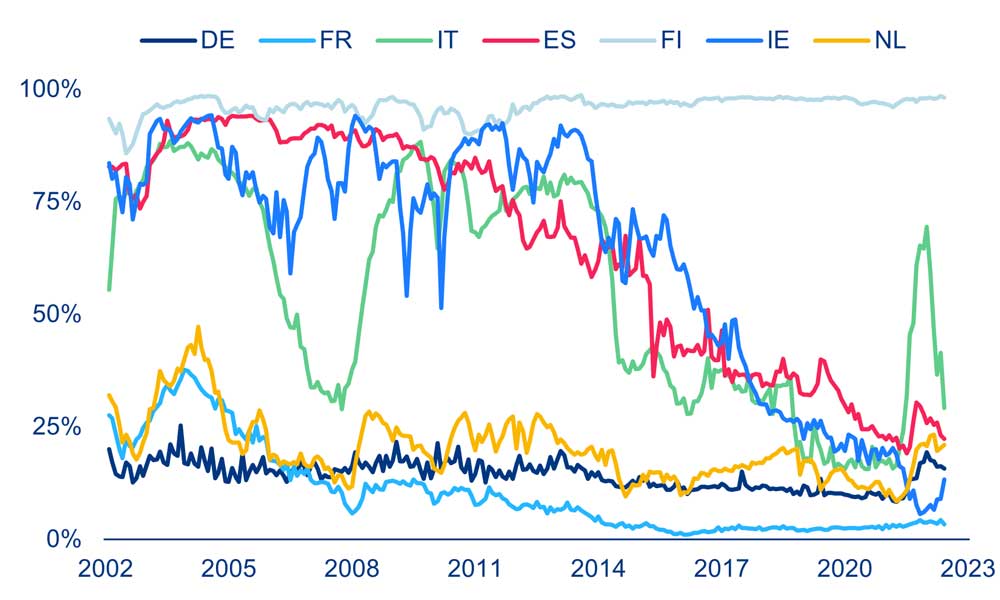

Even as the outlook for Eurozone housing prices is fraught with uncertainty, we do not expect consumers to fully recover purchasing-power losses – and the full transmission from market interest rates to mortgage rates is also still in the making. In 2024, wage-growth expectations (between +4% and +5% in 2023, and +3% and +4% in 2024 for the major economies) will recover only partially in real terms, and the expected home-price correction will fall short from the breakeven figures mentioned above in most countries. Moreover, the fact that fixed-rate mortgages became more popular across almost all the countries has prevented a full pass-through to mortgage rates. But this will come as many mortgage rates are fixed for only a specific period of time. As such, we expect home-affordability losses to range between 5% and 12% by 2024.

Figure 3: Share of new loans at variable rate in total mortgage loans of selected Eurozone economies.

Sources: ECB, Allianz Research

Central and Eastern Europe – Energy crisis unlikely next winter, thanks to declining dependence on Russian oil and gas

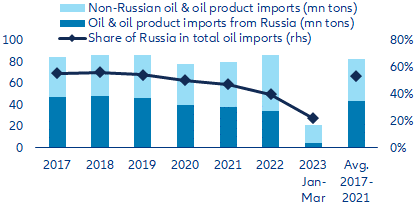

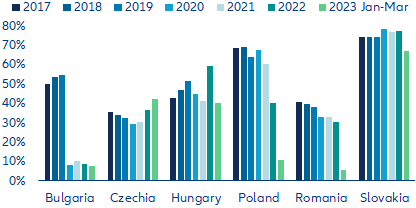

Central and Eastern Europe (CEE) are now much less dependent on Russian oil. While the volume of total imports of oil and oil products in the CEE-6 economies (Bulgaria, Czechia, Hungary, Poland, Romania, Slovakia) increased to a record high 86mn tons in 2022, despite rising global prices, the share of Russia in these imports fell to 40%, down from 47% in 2021 and an average 53% in 2017-2021 (Figure 4). That share fell further to 21% in the first quarter of 2023, following the EU’s embargos on seaborne Russian crude oil imports from early December 2022 as well as on imports of Russian oil products from early February 2023. However, some countries are better equipped than others to turn away from Russian oil: Poland, Romania and Bulgaria – countries with access to the sea – have adapted best, largely eliminating their dependence on Russian oil (which accounted for 11% or less in these countries in Q1 2023). However, landlocked Czechia, Slovakia and Hungary have not yet managed to adapt. The share of oil imports from Russia actually increased in Czechia to around 40% in 2022-2023 and it remained high at 40% in Hungary (in Q1 2023) and at 67% in Slovakia (Figure 5). In order to protect these countries from an energy crisis, the EU did not extend its embargo to Russian crude-oil imports via pipelines.

Figure 4: CEE-6 – Russian and non-Russian oil and oil products imports

Sources: Eurostat, ITC Trade Map, Allianz Research

Figure 5: CEE-6 – Share of Russia in oil and oil products imports

Sources: Eurostat, ITC Trade Map, Allianz Research

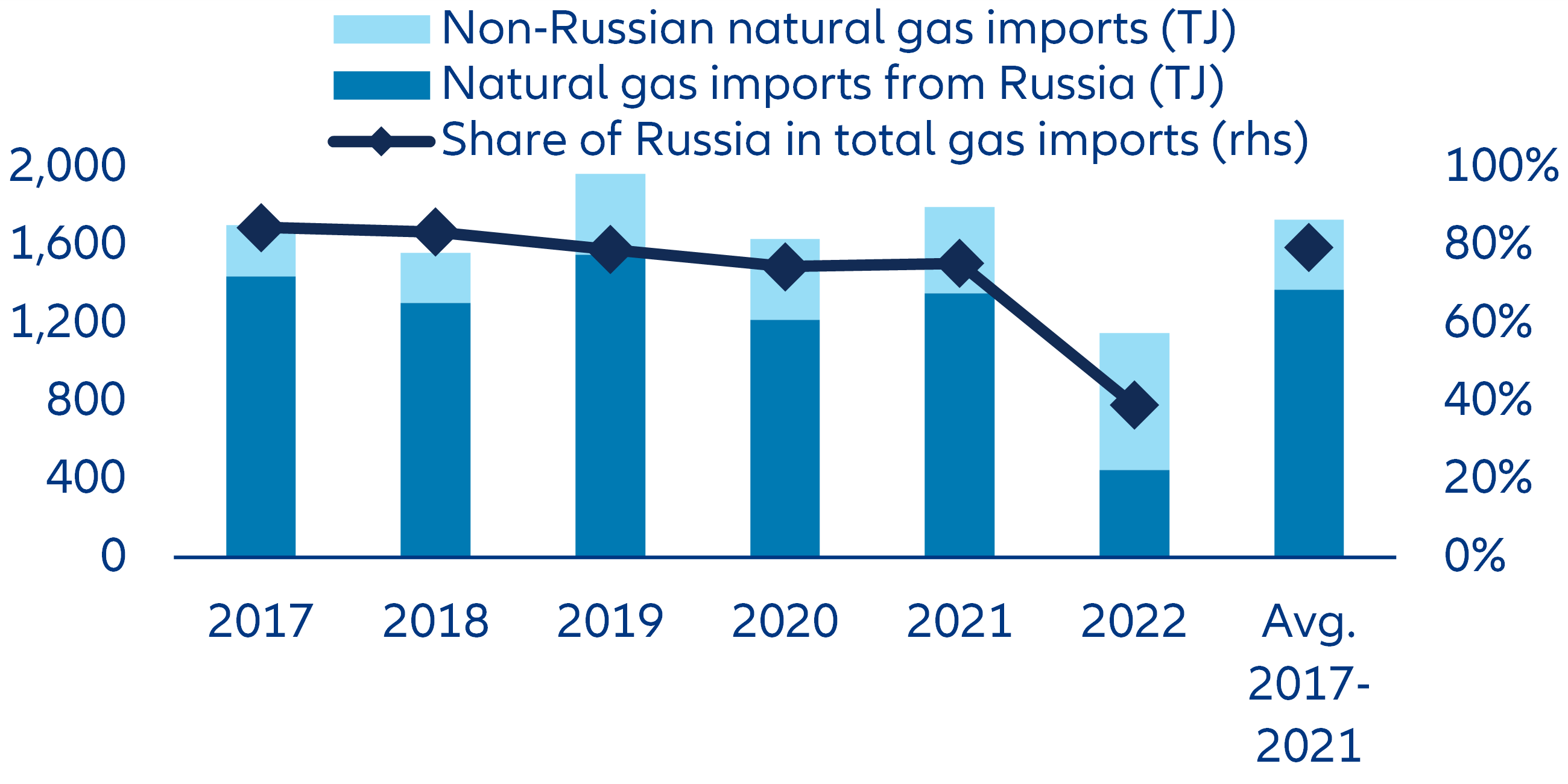

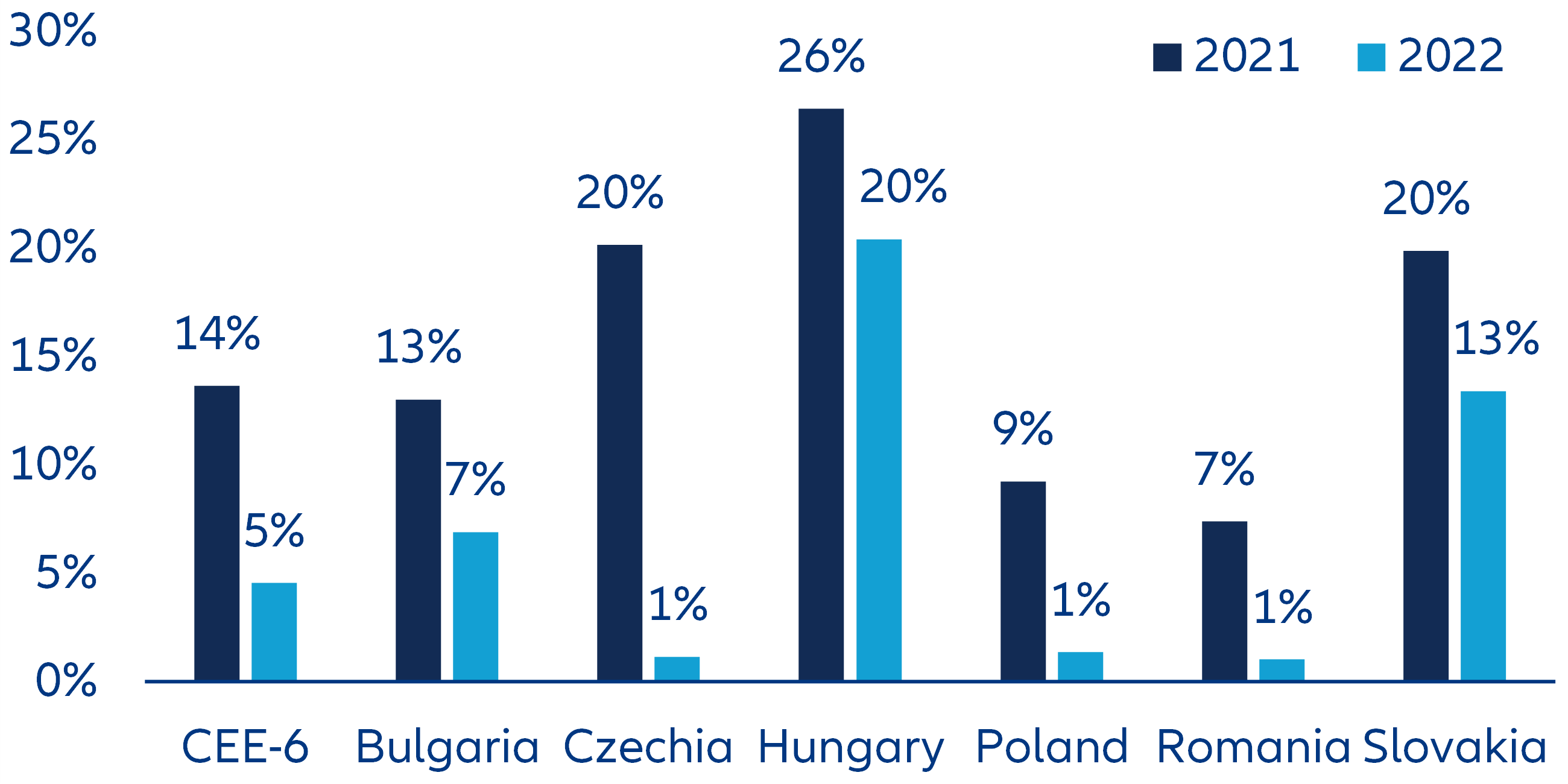

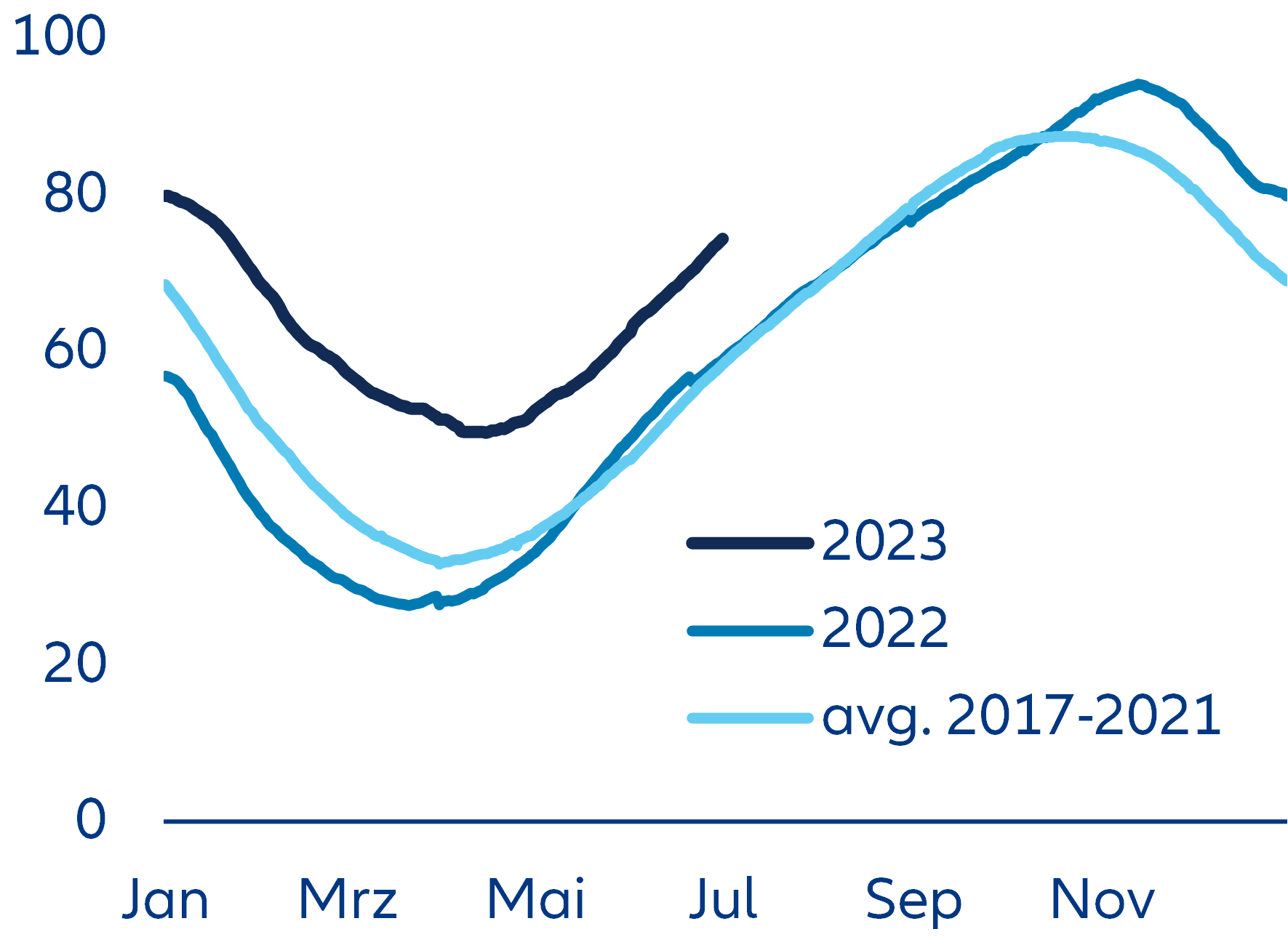

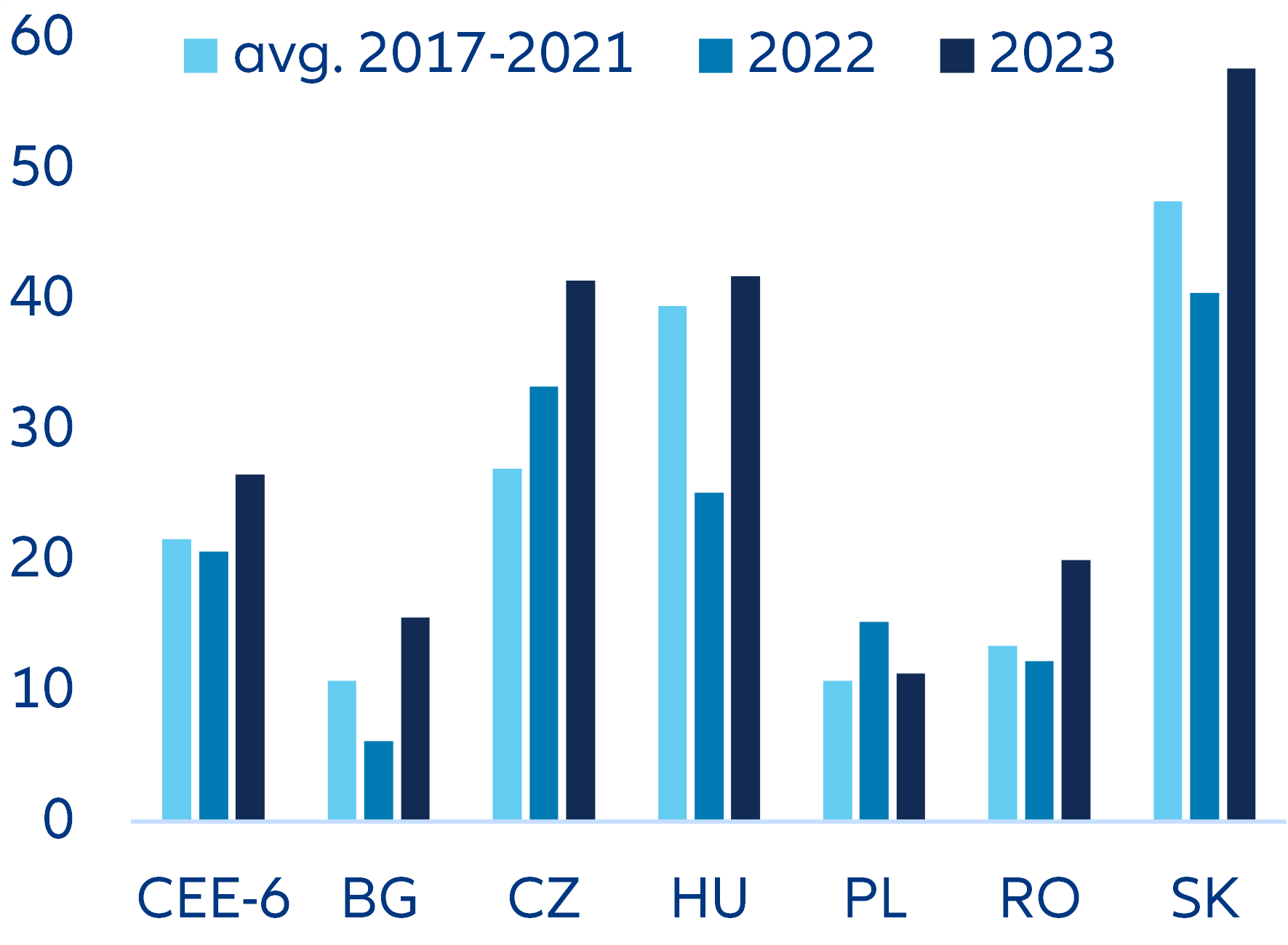

CEE dependence on Russian gas has also declined and the gas-storage position in the region was better as of mid-2023 than at the same time in previous years. The CEE-6 region’s total natural-gas imports decreased by -32% to 31BCM in 2022 from an average 45BCM in 2017-2021. Moreover, the share of gas imports from Russia in total gas imports dropped by -67% to 12BCM in 2022 from 36BCM in 2017-2021. As such, the share of Russia in the region’s gas imports halved to 39% in 2022 from an average 79% in 2017-2021 (Figure 6). As a result, natural-gas imports from Russia accounted only for 1% of total primary energy consumption in Poland, Czechia and Romania, and for 7% in Bulgaria in 2022 (Figure 7). In fact, the shares have gone to zero in Poland and Bulgaria after Russia halted gas deliveries to these two countries in April 2022. Poland has substituted gas largely with locally mined coal while Bulgaria has secured new gas deliveries via a pipeline from Greece. However, the shares of gas imports from Russia in total primary energy consumption were still significant in Hungary (20%) and Slovakia (13%), putting these countries at somewhat higher risk of energy shortages should supplies from Russia dry up. That said, the gas-storage facilities in the CEE-6 have been much better filled in the first half of 2023 than in previous years. As of mid-year, they were 74% full in 2023, compared to 59% in 2022 and 58% on average in 2017-2021 (Figure 8). Looking at the stocks of gas in storage as of end-June in relation to the previous year’s gas consumption, we see that the CEE-6, with the exception of Poland, is better positioned this year than in previous years. And this share was the highest in Slovakia (58%), Hungary (42%) and Czechia (41%), mitigating somewhat these landlocked countries’ otherwise larger dependence on Russian energy.

Figure 6: CEE-6 – Russian and non-Russian natural gas imports”

Sources: Eurostat, ITC Trade Map, Allianz Research

Sources: Eurostat, ITC Trade Map, Allianz Research

Sources: GIE – AGSI, Allianz Research

All in all, we expect the CEE-6 economies to make it through the winter 2023/2024, even if it turns out harsher than the last one. There is a tail risk of energy shortages in Hungary, Slovakia and to a lesser extent Czechia in the event that the coming winter is very cold and a full-scale embargo on Russian oil and gas exports to the region is implemented. If this materializes, we would expect the EU community to be ready to support. That said, this tail-risk scenario should be the incentive for governments in CEE to continue vigorously with their energy-transition plans.

Simultaneous currency depreciation and subsidy cuts – igniting social unrest in Africa?

40% of the African economy faced a local currency devaluation of at least 30% in the past 12 months. It means that at best the cost of imported goods (in terms of units of local currency equivalent to the same amount of USD) has increased by 40%. The fact that inflation has not risen as much (we forecast an average inflation rate of 15.9% on the continent for 2023) tells how much of these costs have not been passed on to the population yet as well as the magnitude of government subsidies, such as those on fuels, which historically are imported even by major hydrocarbon exporters, like Nigeria and Angola.

Along with devaluation, the removal of fuel subsidies adds up to the loss of purchasing power and to enterprise costs. Two months ago, the IMF published an analysis on currency depreciation across Sub-Saharan Africa, pointing to the vulnerability of economies to the international economic situation as the main cause and suggesting tighter monetary policy, fiscal consolidation (e.g., eliminating fuel subsidies) and strengthened social safety nets as countermeasures in light of historically low government revenues (see Figure 9).

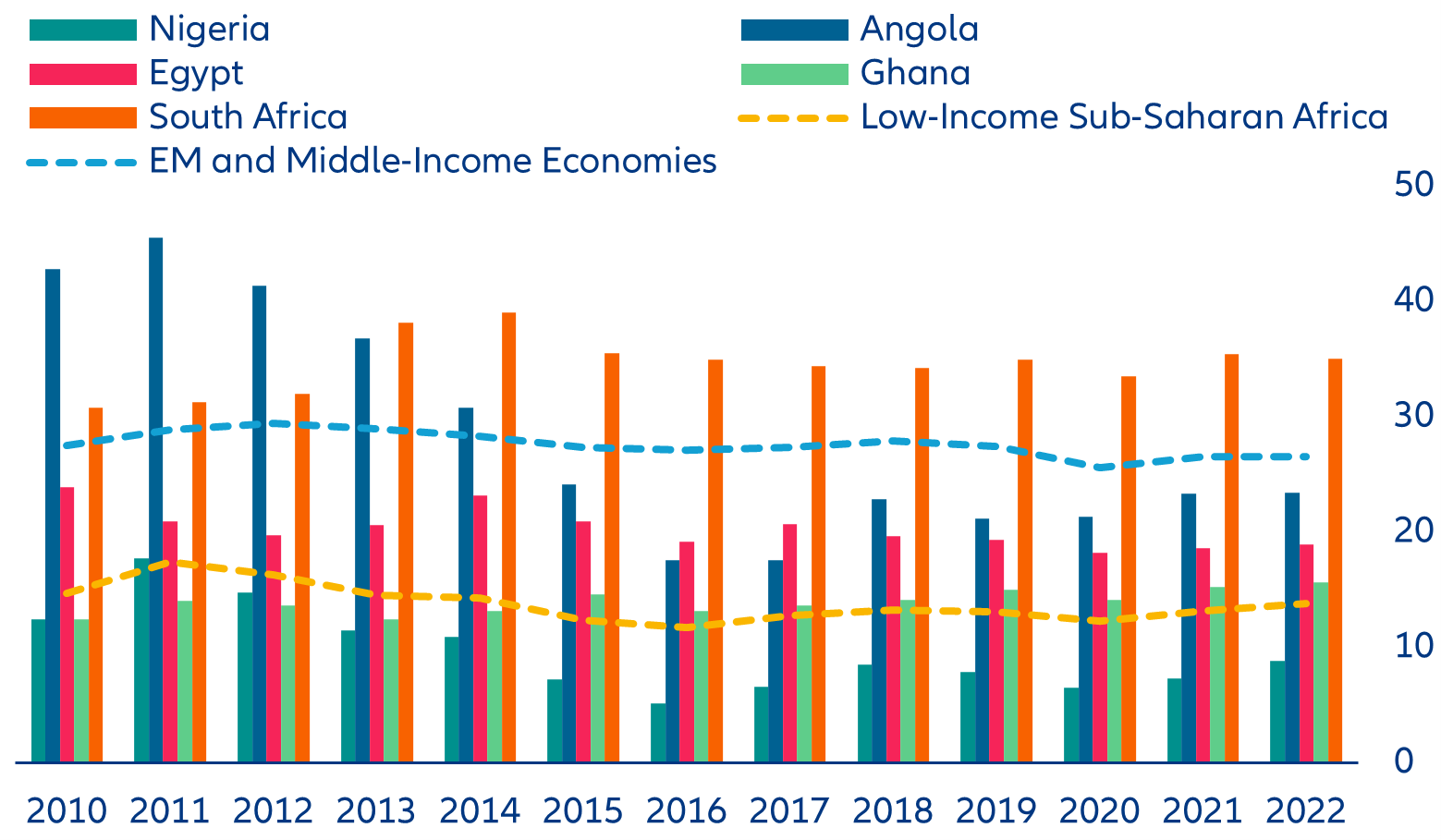

Figure 9: General government revenues, selected African countries (% of GDP)

Sources: IMF, Allianz Research

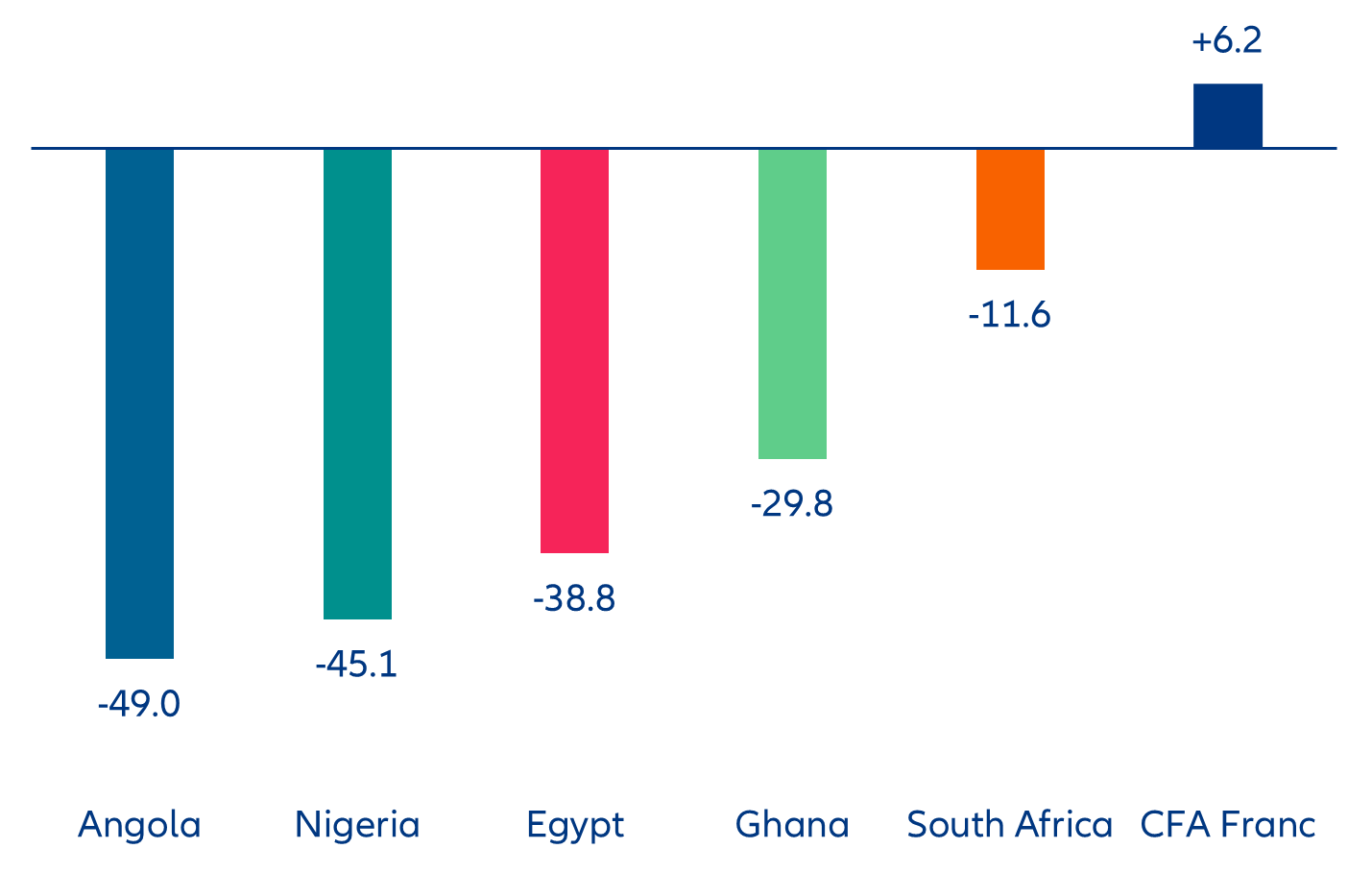

Several countries have devalued their currencies since May, leaving behind the peg with the US dollar that they had maintained up to that point, and also acting on fuel subsidies. In Africa this is the case of the Angolan kwanza and the Nigerian naira, following other currencies that have also depreciated significantly over the past twelve months, such as the Ghanaian cedi and the Egyptian pound (see Figure 10). The four countries alone made up 39% of Africa's 2022 GDP. Kenya and Senegal have also slashed subsidies on the price at the pump to comply with IMF requests.

Figure 10: Currency depreciation (-) / appreciation (+) against the USD in the last 12 months (%)

Sources: Refinitiv, Allianz Research

The combination of devaluation and subsidy removal may trigger significant unrest across the region; Nigeria and Egypt, the continent's two largest economies in terms of GDP, have shown similar dynamics in recent weeks despite a different political setting. Nigeria comes from a presidential election in February in which the winner, Bola Tinubu, was voted by 9.4mn people out of a population of around 231mn. In Egypt, a presidential election is due early next year with President Abdel Fattah al-Sisi looking to repeat the success of 2018 when he got 97% of the vote, or 23mn votes out of a population of 97mn at the time. An escalation of social tensions could have a contagion effect on institutional strength and stability in the area also due to uncertainties about Wagner paramilitaries' role and ongoing conflicts.

Nigeria can be seen as a microcosm of Africa with its strong demographic dividend and great political fragility, deep divisions between north and south and along cultural and religious fault lines, a post-colonial legacy still visible in the balance of trade and an increasingly worrying level of public debt. Struggles to convert economic potential into real growth, production limited by instability and insecurity (as in the case of oil output remaining below the OPEC-agreed quota) and economic diversification still in the making suggest that developments of recent weeks may tell us much about what lies in store for the entire region, for better or worse.

Sources: Refinitiv, National agencies, Allianz Research

Nigeria’s new administration delivered a combo of measures in a fortnight, such as the removal of the fuel subsidy that brought gasoline from USD0.55 per liter in April to USD1.1 by end-May, and the devaluation that came in on 14 June. Two weeks after President Tinubu assumed office, the second longest-serving governor of Nigeria’s central bank was put under arrest. Under his tenure, the central bank supplied the government with the equivalent of USD49bn (NGN22.7trn) in the form of advances, de facto increasing domestic public debt and reducing local currency supply, under a clause that can be activated only if the government experiences a temporary revenue shortfall. These claims will also be subject to devaluation, helping the government repay at least partially such exposures through oil revenues in hard currency. The devaluation could thus help rebalance the public debt profile, but it will bring along prolonged inflation, a higher import bill and additional stress on banks. Short-term domestic debt accounts for more than half of the total, with two-year interest rates well in the double-digits. Assuming that the devaluation could help reduce sovereign exposure and make foreign investment more attractive, Nigerian banks may face a marked deterioration in the quality of assets, capital adequacy and the share of non-performing loans.

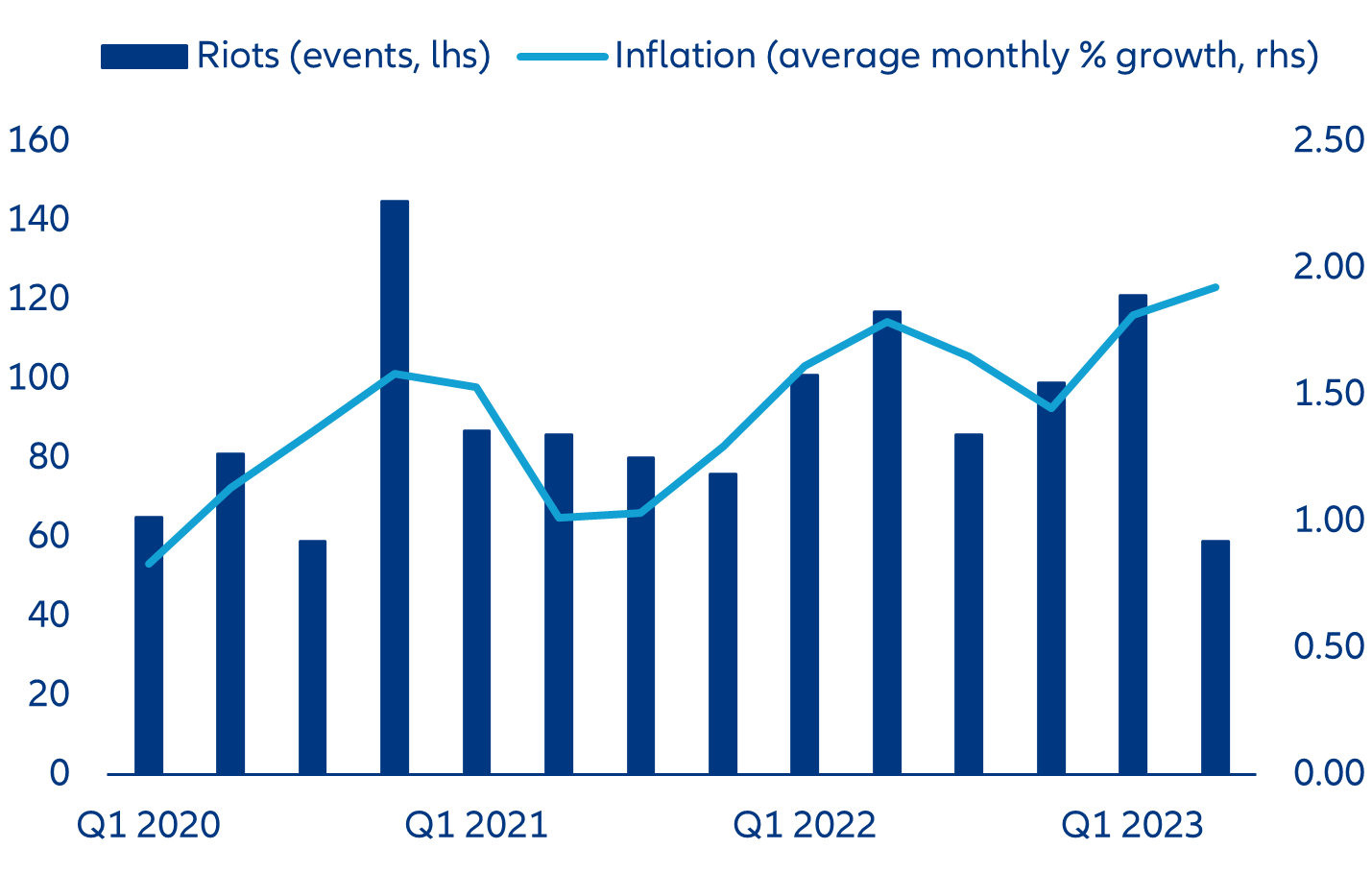

The shock therapy is aimed at redressing structural imbalances but may come with an elevated social cost as four out of 10 Nigerians live below the national poverty line and the minimum wage is still at USD65 per month, equivalent to around one tank of gasoline after the removal of the subsidy. In this context, social calm has been surprising over the past quarter given that unrest is significantly correlated to inflation (Figure 12).

Figure 12: Number of reported social unrest events and monthly inflation in Nigeria, 2020 - Q2 2023

Sources: Central bank, ACLED, Allianz Research

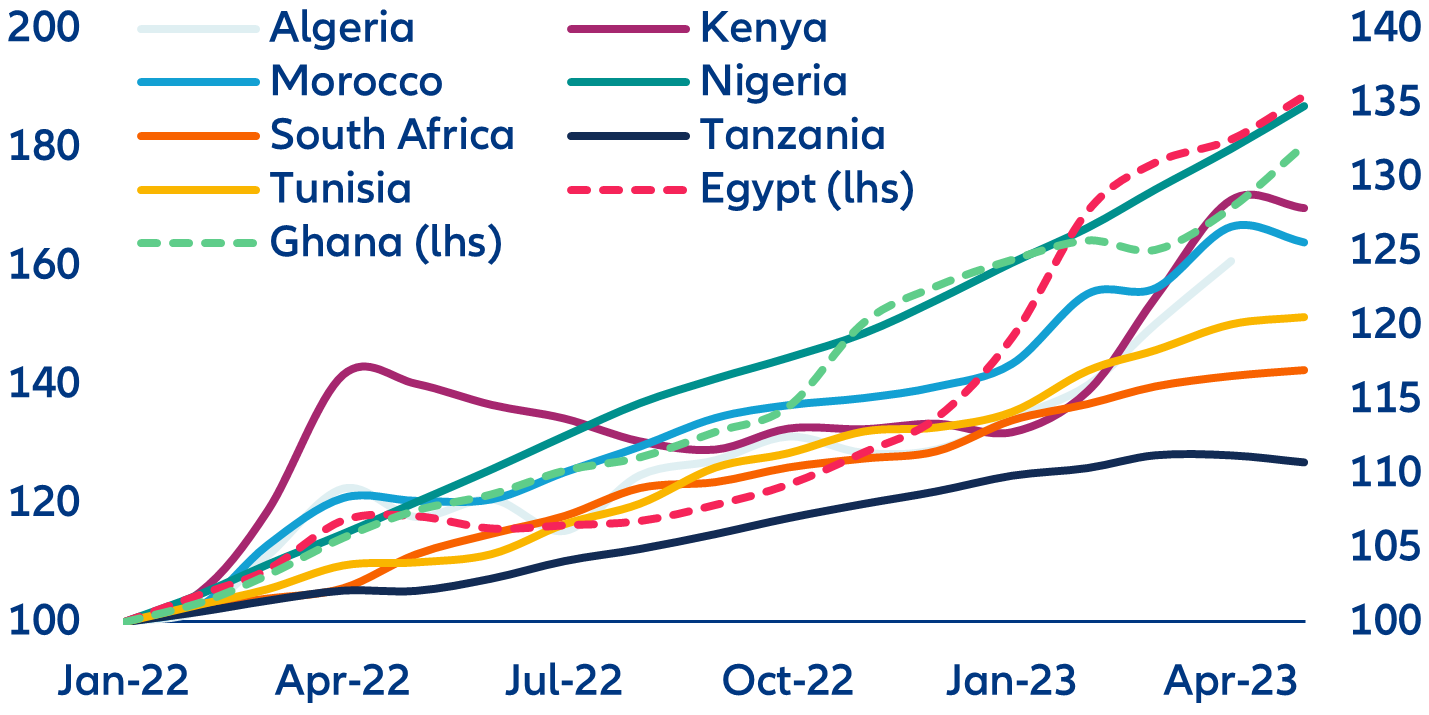

In Egypt, social stability is also surprising on the upside despite dire economic conditions, but some indicators signal that this may be a false sense of calm, while the peak-tourism season may play a role. Food prices rose by +62% in the year following Russia’s invasion of Ukraine, which was Egypt’s main supplier of grains, and have continued to increase (+27% between January and May 2023) despite a substantial moderation in global food prices. Half of Egypt’s population may have fallen below the poverty line.

Figure 13:. Food inflation, selected countries (food and beverages, index: Jan 2022 = 100)

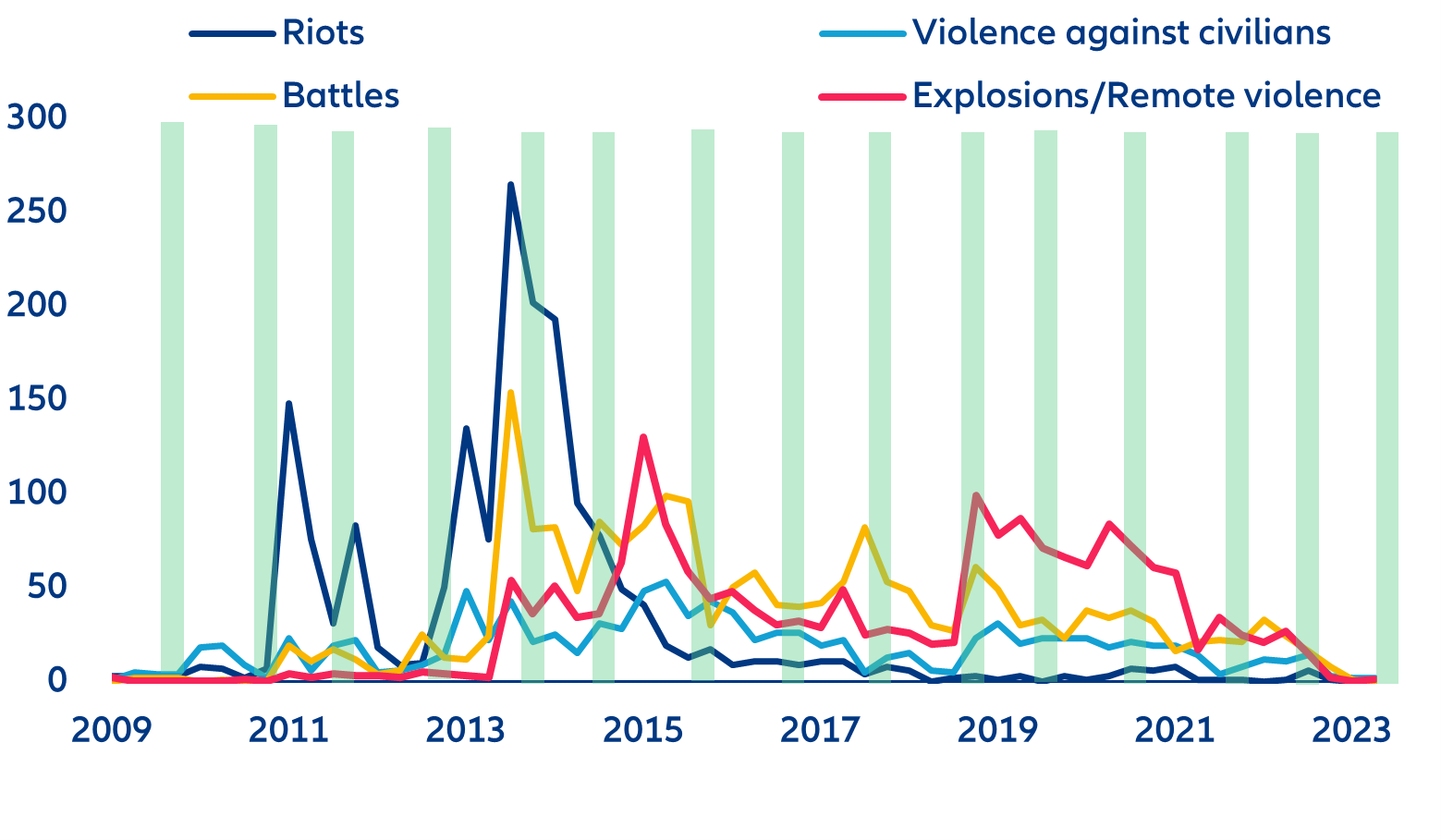

The frequency of political-related events in the last quarters suggests that restrictions on public space have been extended beyond Ramadan, when confrontations historically tend to calm down (Figure 14). Since mid-2018, Egypt’s civil society has been de facto silenced and it is unclear whether this will lead to any resounding developments in the short term. The last time the calm lasted so long was in 2009-2010, i.e., before the Arab Spring erupted. Riots occurred often between 2011 and June 2014 (when al-Sisi's presidency began). In contrast, in the year before he came to power and ever since, explosive attacks and border and insurgent clashes have been by far the most recurring event, unusual for a country not involved in open conflicts. What is surprising about the past six months is the neutralization of any public action, be it a small sit-in or a militia clash. On the other hand, the escalation of the conflict in Sudan, sporadic Islamic State attacks on the Sinai Peninsula in the first half of 2023 and Israel recently complaining about the porousness of Egypt’s borders all point towards increased instability and limited military capability.

Figure 14. Frequency of political events in Egypt, 2009-2023ytd (green bands indicate Ramadan)

Sources: ACLED, Allianz Research

The distance between the establishment and the rest of the Egyptian population has also increased, although generalized unrest remains unlikely in the short term and progress towards IMF-inspired reforms is faltering. The IMF wants to ensure that conditional funds will effectively redress imbalances. Reforming the economy will require redesigning the role of the military and downsizing megaprojects (e.g. the new administrative capital 30km outside the overcrowded and increasingly impoverished Cairo) that are propping up the construction sector, which employs 13.8% of the labor force – third sector in Egypt behind agriculture and trade, second in terms of male workers. However, there is little incentive to pursue additional reforms with the upcoming presidential election in February 2024 and evolving bilateral relations with the Global South. For example, India is set to acquire a dedicated land area for national industries in the Suez Canal Economic Zone and build a USD12bn green hydrogen plant. Since its completion 154 years ago, the Suez Canal has been used as a strategic trump card by successive governments. Several sources talk openly about the possibility of leasing it. Transit fees were already raised several times in 2022-2023 and shipping brokers agree that there is still room for an increase without significant consequences on traffic volumes, given its competitive advantage over alternative routes.

The combination of silenced dissent and increasing mistrust towards international lenders leaves the door open for different outcomes, while another Egyptian pound (EGP) devaluation appears imminent. The differential between the nominal value of the EGP and its fair value is reaching another peak following those of late 2022 and early 2023. With several other countries on the continent devaluing their national currencies inter alia to attract investors, this could be the Egyptian government's next move, hoping the status quo holds up.

Unlike the sovereign debt crises, an escalation of social tensions could have a contagion effect on several African countries, also given the uncertainties about the role of Wagner paramilitaries in the area and increasing insecurity. While everyone's eyes have been on the state of African governments' accounts and the risk of transmitting sovereign crises for months, the main risk to the continent may instead lie in social risk, not economic or financial risk. No other sovereign defaults have emerged at the time of writing since Ghana's deafening crisis in December 2022, although public finances have been deteriorating in Egypt and Tunisia in particular. Several African governments are looking for their own way out with lenders (concessional lenders, China, former colonial powers, other African governments). Three years after a currency crisis, real GDP is typically between 2 and 6 percentage points lower than where it should be based on long-term growth. In most cases, however, output losses start materializing before the currency collapse takes place. In fact, it turns out that the collapse of the currency itself boosts production. Previous research shows that output growth slows down in the year leading up to currency devaluation and during the same year. However, the likelihood of a positive growth rate in the year of the collapse is over two times more likely than a contraction, positive growth rates in the years that follow currency collapse are likely and the persistence of the crash matters. Instead, it will be the responsiveness of individual economies and the resilience of the social contract that will tell us whether a cost-of-living crisis will also bring social disruption across the region.

In focus – A new Eurozone doom loop?

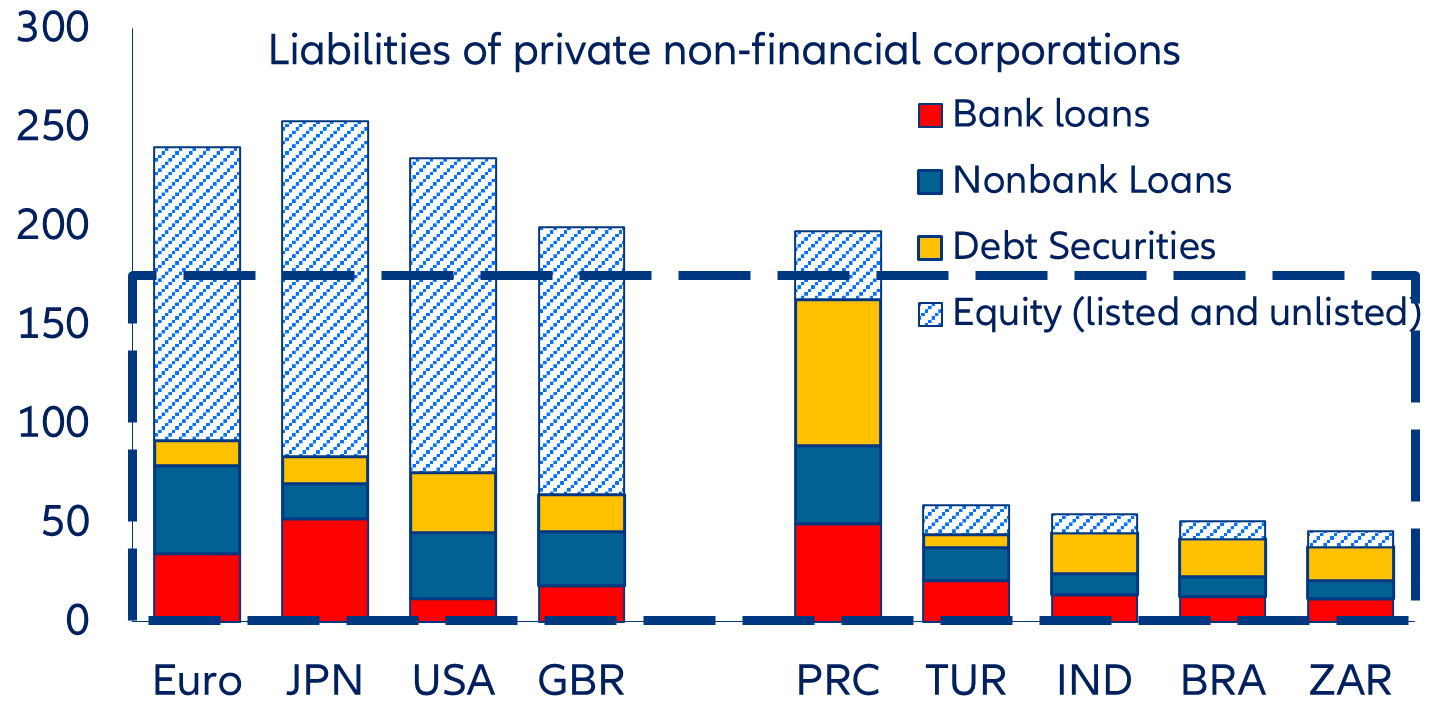

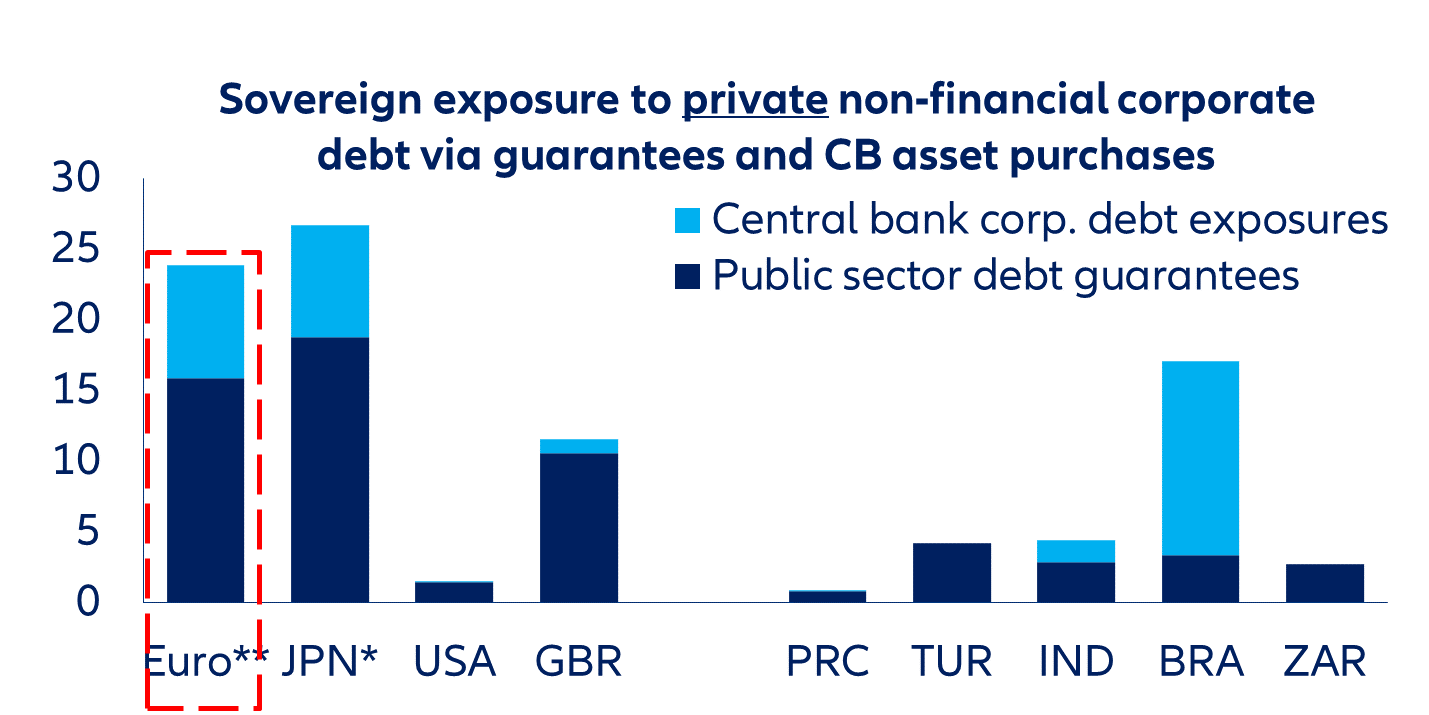

As firms recover from the pandemic and energy crises in Europe, higher public-sector exposures raise the risk of a doom loop as weak growth puts increasing pressure on corporate margins. While support measures, including energy subsidies, liquidity facilities and debt guarantees, have helped keeping vulnerable firms afloat (Figure 15), there has been considerable economic scarring – and the risk of higher corporate defaults over the near term continues to rise (especially as governments start tightening their belts). At its heart, the Eurozone has slipped back into recession and at the end of the year, the bloc’s economy will be barely larger than it was before the pandemic. Some sectors and firms have yet to fully recover (or might slowly disappear), including those more affected by pandemic-related containment measures and related changes in consumer behavior, as well as supply-chain stoppages from critical upstream trading partners. Others are propelled by deeper technological changes and the transition towards a greener economy, which will help them expand more rapidly. This uneven and feeble recovery – combined with the suspension of market signals in sectors with heavy intervention – not only creates a challenging environment for assessing corporate credit risk in banks’ loan books but also contingent liabilities for the public sector as a legacy cost of crisis support.

Figure 15: Eurozone – Changes of key macro-financial conditions (indexed, last pre-recession quarter=100)

Sources: Refinitiv Datastream, IMF Fiscal Monitor (April 2021), Allianz Research. Note: 1/ comprises only public credit guarantees for corporate lending by banks and asset purchases with significant corporate risk (i.e., corporate bonds, private label asset-backed securities, and covered bonds). Guarantees cover mostly new lending and many credit-guarantee programs have not been fully exhausted (assumption: 2/3 usage rate). The actual materialization of guarantees will depend on loan losses in excess of current provisions (net of collateral value) and the loss-sharing by governments (usually about 80%); */ includes stocks and ETFs; **/ weighted average of Germany, France and Italy.

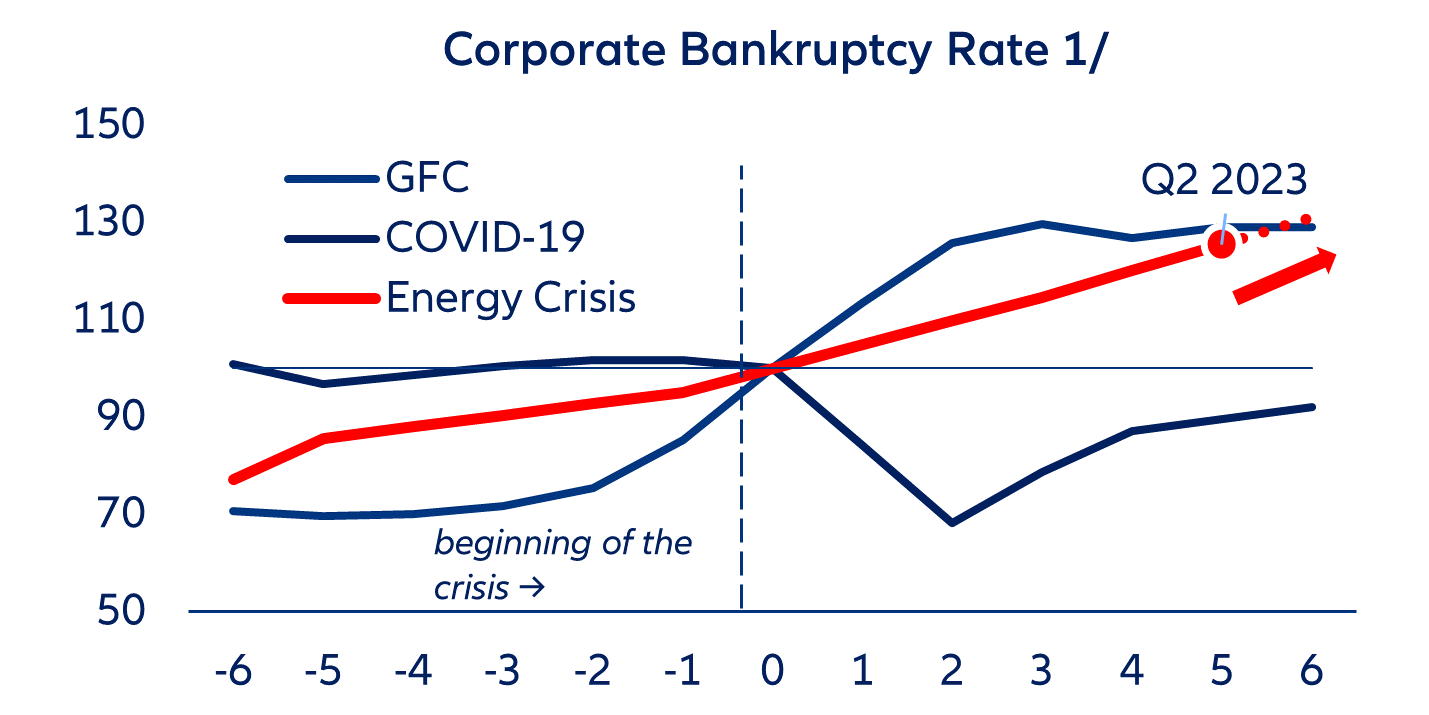

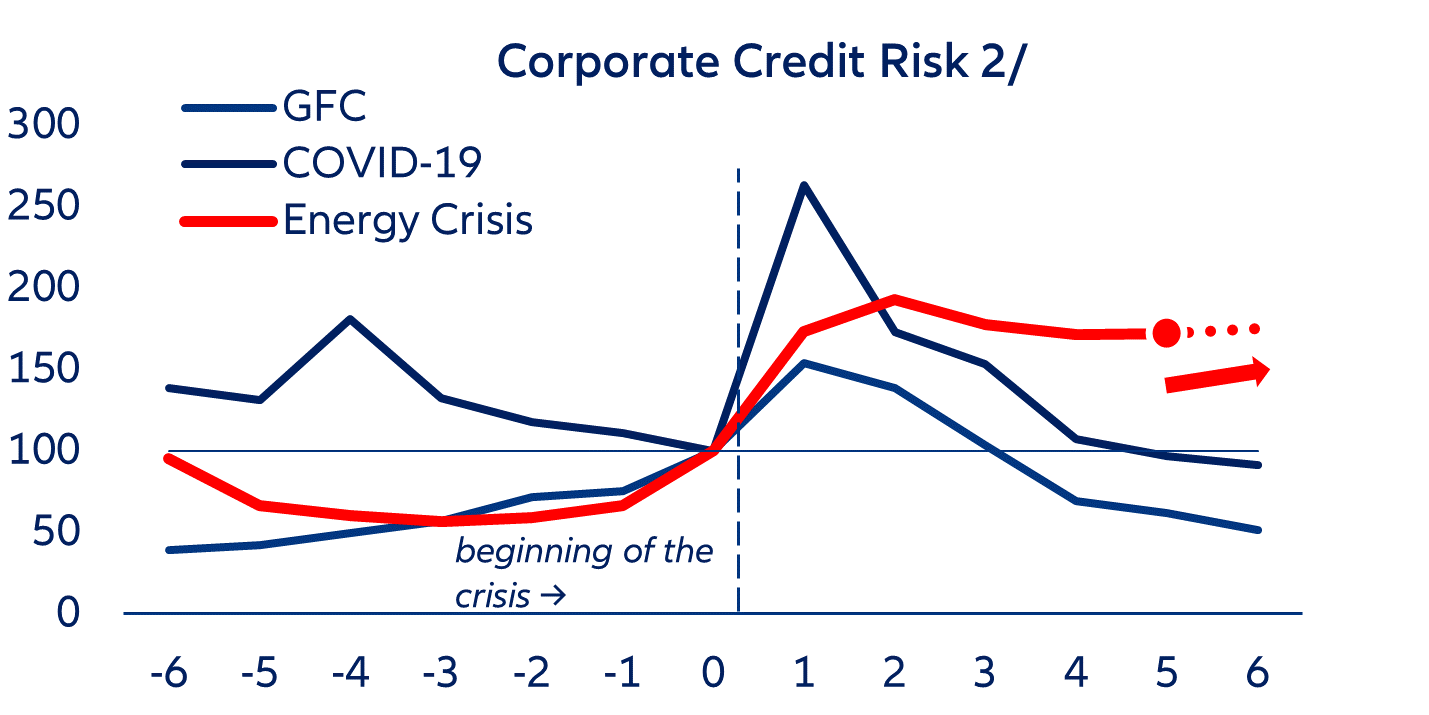

Figure 16: Eurozone – Changes of key macro-financial conditions (indexed, last pre-recession quarter=100)

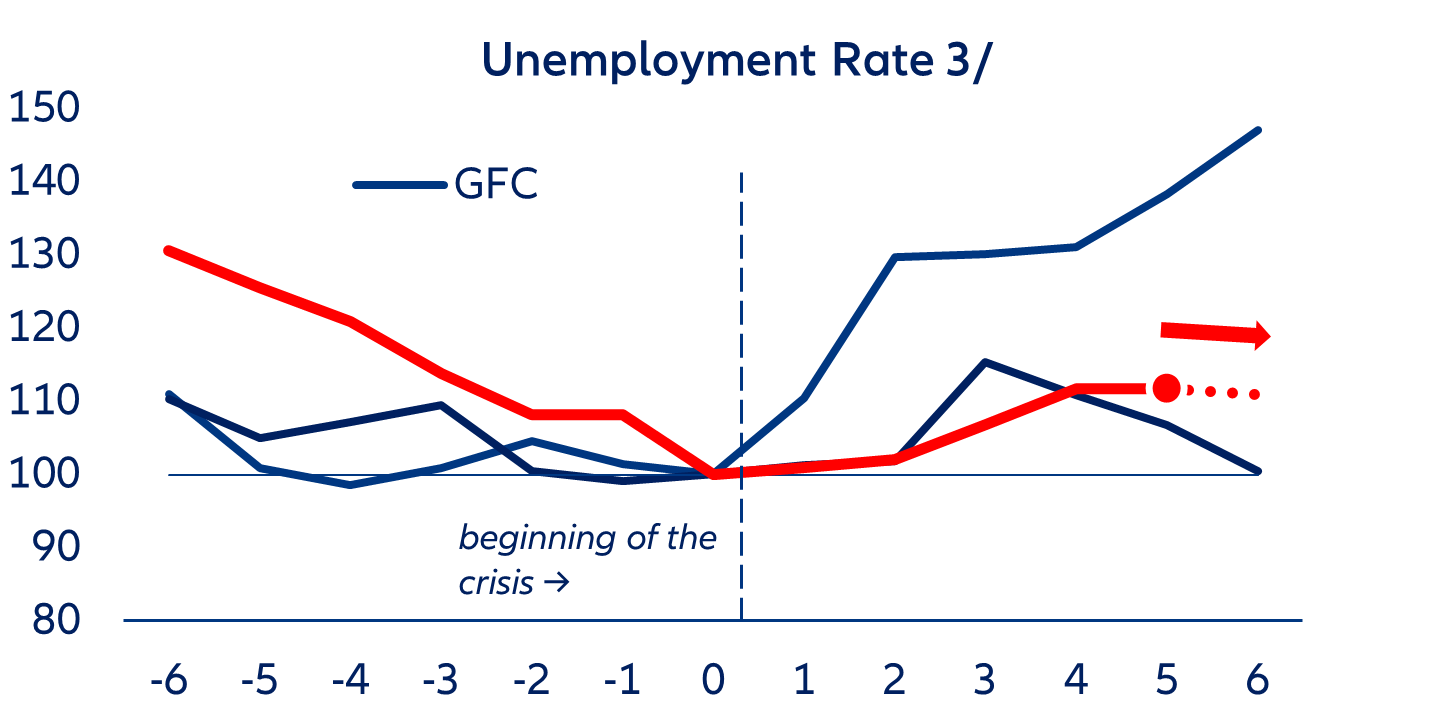

Sources: Eurostat, OECD, St. Louis Federal Reserve, Refinitiv Datastream, Allianz Research. Note: GFC=global financial crisis; the dotted line indicates a forecast value for Q2 2023; 1/ simple average of Belgium, Finland, France, Germany, Italy, Netherlands and Spain; 2/ effective yield (NSA) of euro-denominated high-yield corporate debt securities (ICE Bank of America Euro High Yield Index); 3/ harmonized EA-19 unemployment rate, NSA.

Despite extraordinary crisis support (also compared to other jurisdictions), many heavily indebted firms in the Eurozone will continue to struggle. The Eurozone has slipped back into recession and at the end of the year, the bloc’s economy will be barely larger than it was before the pandemic. Insolvency rates have already started increasing again, but delayed insolvency proceedings and a shallow recession thus far have helped keep corporate defaults low. These suppressed bankruptcies are hiding considerable losses, which could rapidly manifest once the effects of strong policy support have faded, given the buildup of corporate leverage and still weak fundamentals. In fact, many small businesses are still barely afloat and will therefore need to be wound up or restructured. Unless addressed early, worsening corporate profitability could quickly turn into losses – and these liabilities would become real losses for the sovereign.

Over the next few years, the Eurozone could become trapped by a combination of weak fundamentals and excessive policy interventions amid rising geopolitical tensions and secular challenges (e.g. climate, demographics and technological change). This would exacerbate vulnerabilities from mispriced risk, while underlying fundamentals continue to worsen. But as the credit cycle turns negative (with money supply having turned negative for the first time ever) and fiscal policies become restrictive, the economy must eventually “snap back” to weak fundamentals. With new lending depressed, economic activity would stall.

Figure 17: Stylized doom loop of the corporate-financial sector-sovereign nexus

Source: Allianz Research

In an extreme adverse scenario, the complex system of interlinkages between real activity, banks and sovereigns means that an incipient corporate necrosis would spread rapidly, triggering a fundamental repricing of risk in a new “doom loop” (Figure 17). A trickle of defaults in some critical and well-connected sectors could grow rapidly into a torrent, and the sudden realization of losses would jolt capital markets, precipitating a systemic crisis that reverberates through corporate, financial and sovereign feedback loops.

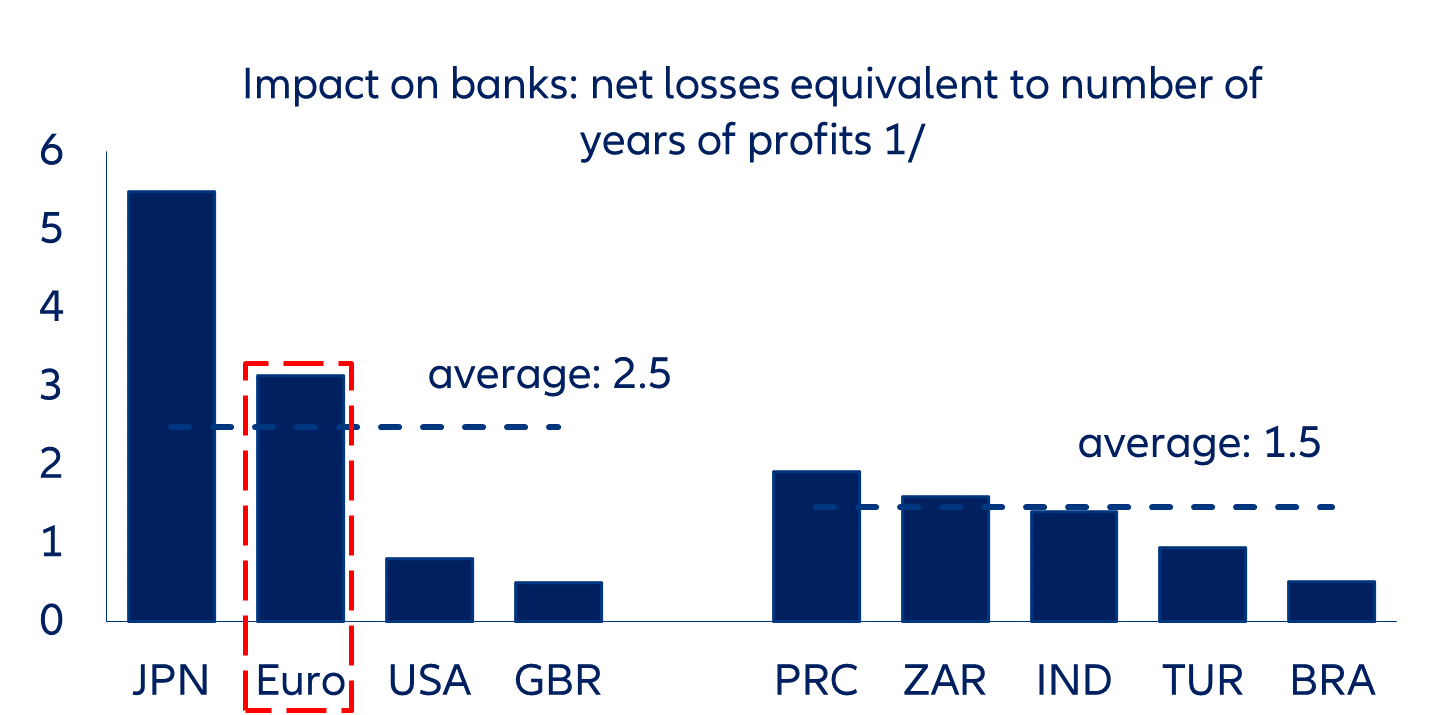

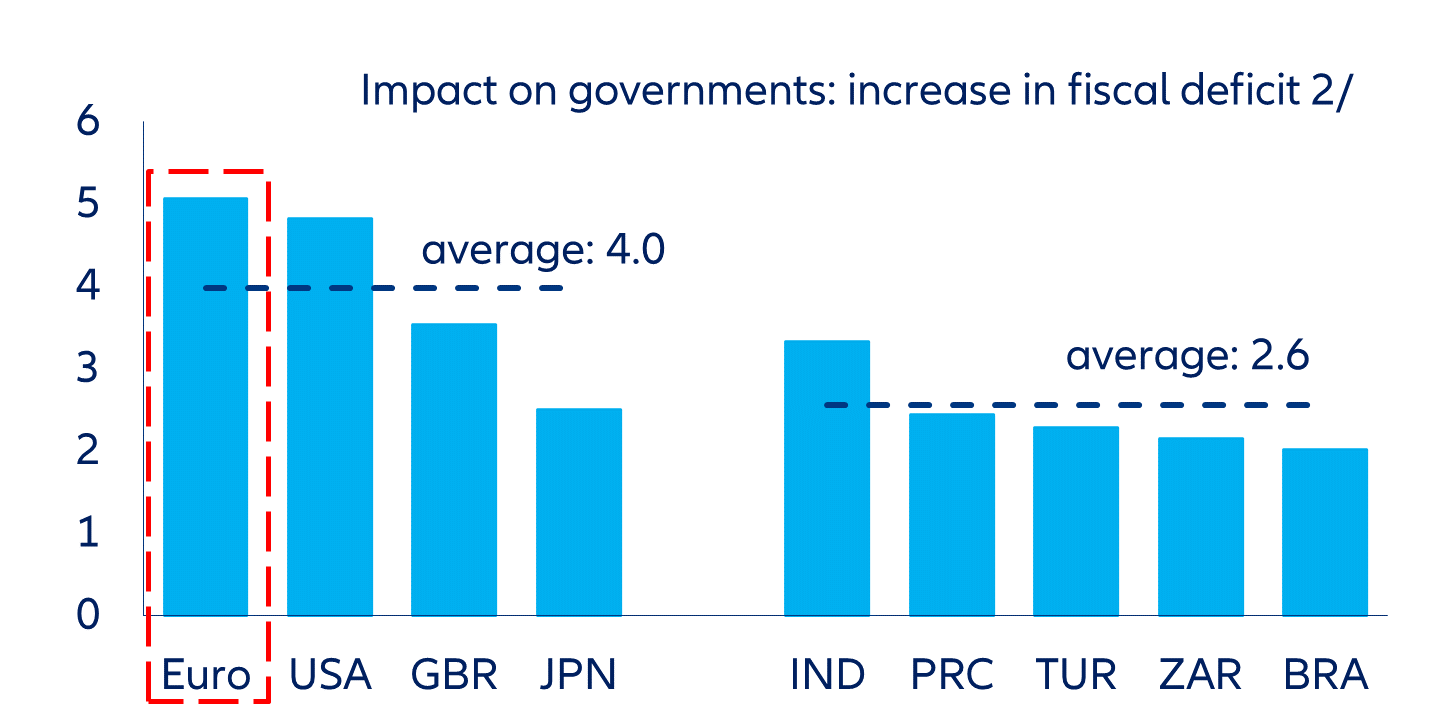

If we conservatively assume default rates seen in previous crises, we can expect a cumulative default rate of 10% over the next two years in this extreme scenario. This would imply a steep increase in insolvencies, based on a current annual default probability of less than 1%. Under these assumptions, losses in the corporate sector would wipe out about three years of bank profits (Figure 18). Banks would respond by cutting back on their riskiest lending to preserve capital – typically to SMEs that need it most. Given sovereign exposures to corporates, the public sector would also bear losses – including up to 5% of GDP on average from direct losses and foregone corporate tax revenues – which would cut deeply into what little policy space is left (Figure 18). In this situation, the Eurozone would find itself in a prolonged recession, but this time with more debt and minimal policy space for yet another fight.

While this scenario remains extreme, it underscores that financial sector policies in the Eurozone need to be become more forward-looking regarding potential corporate sector risks. This is especially the case in some countries where slower insolvencies and lower asset-recovery rates would amplify economic scarring, threatening to undermine the financial system and erode valuable policy space. To reduce the debt overhang ex post, swifter, more efficient and more robust debt-resolution frameworks are needed, including simplified insolvency procedures for SMEs, hybrid restructuring mechanisms and out-of-court workouts.

Pre-emptive policies must include urgently completing the Banking Union. Despite the single supervision and resolution of banks, the Banking Union remains incomplete, with attendant risks of potential fragmentation during times of stress. In recent years, progress to close important gaps, such as the design and implementation of the European Deposit Insurance Scheme (EDIS), has lost momentum and will require a new push to reach consensus and encourage greater cross-border banking. While the European Commission has adopted a proposal to adjust and further strengthen the EU’s existing bank crisis-management and deposit-insurance (CMDI) framework, with a focus on medium-sized and smaller banks, it ignores the role of effective national institutional protection systems and the importance of EDIS (also in resolution) for completing the Banking Union.

Figure 18: Eurozone – first order Impact on banks (net losses equivalent to number of years of profits) [top] and governments (higher fiscal deficit from contingent liabilities, central bank exposures and lost taxes as % of GDP) [bottom]

Sources: Refinitiv Datastream, Allianz Research. Note: we assume a corporate default rate increase of 6.1pps in 2023, with the government absorbing 90% of losses covered by guarantees; 1/ for the analysis of the impact on banks, capital buffers are preserved without considering the additional impact of net change in corporate credit risk weights and lost interest income from corporate lending; 2/ the fiscal analysis does not include impact of deteriorating fiscal deficit and government debt stock on funding costs (and debt sustainability) and comprises only public credit guarantees for corporate lending by banks, which cover mostly new lending. Many credit-guarantee programs have not been fully exhausted (assumption: two-thirds usage rate); governments also incur corporate income tax losses of 30% and 25% of GDP (ex post shock) in advanced and emerging economies, respectively.

At the same time, policymakers should consider new ways to work more with the private sector to restructure public sector exposures to distressed yet viable firms. This will require a new policy mindset, shifting away from thinking like a creditor looking to collect principal or roll over loans to that of an equity investor looking to maximize recovery value, such as by incentivizing debt restructuring through tax credits and injecting new equity.