- The European Commission’s new Economic Security Strategy could not have come sooner, with its focus on boosting Europe’s competitiveness and deepening the Single Market as essential elements for safeguarding the bloc’s economic security. The pandemic and the energy crises stress-tested the EU’s resolve in forming a strong political consensus. It emerged battle-hardened but severely weakened economically. Now the “European project” finds itself – yet again – at a critical stage of development that requires safeguarding its economic future amid rising geopolitical tensions and domestic pressures.

- While the Economic and Monetary Union has helped increase convergence across countries over the last two decades, the momentum has significantly slowed. In fact, regional disparities are on the rise. In addition, the uneven recovery from the crises is set to increase the income gap as projected growth remains broadly the same across most member countries with still large differences in GDP per capita.

- Clearly this trend warrants asking the critical question as to how the Eurozone can achieve meaningful convergence. Deepening the EMU requires greater financial integration and better coordination of fiscal policies. Completing the banking and capital markets unions, as well as reforming fiscal rules, will ensure a deeper and stronger Eurozone.

In focus – Eurozone convergence: two steps forward, one step back

US labor market – soft landing, but not enough for the Fed

The US labor market seems to be rebalancing painlessly. Labor shortages remain acute, with a vacancy-to-unemployed ratio at 1.8, only a touch below the maximum level reached last December (2.0). However, rebalancing is underway. On the demand side, job vacancies were down to around 10mn in April (JOLT survey), which is -16% from the peak in March 2022 (and around 40% of the pre-pandemic level). On the supply side, the labor force participation rate (labor force over the working-age population aged 15 to 70) stood at 68.6% in Q1 2023, only 0.2pp below the 2019 average. Others measures of labor-market tightness such as the quit rate and the job-search rate are also gradually normalizing.

We expect a soft landing of the labor market despite weakening growth as companies accept lowering their margins. The first signs are already visible with still low unemployment, together with normalizing inflation. The vacancy rate is indeed easing without causing much of a pick-up in the unemployment rate. The fall in job openings so far mostly reflects lower hiring (the layoff rate is remains low). On the other hand, we believe that wage growth and inflation will normalize by the first half of next year (see below).

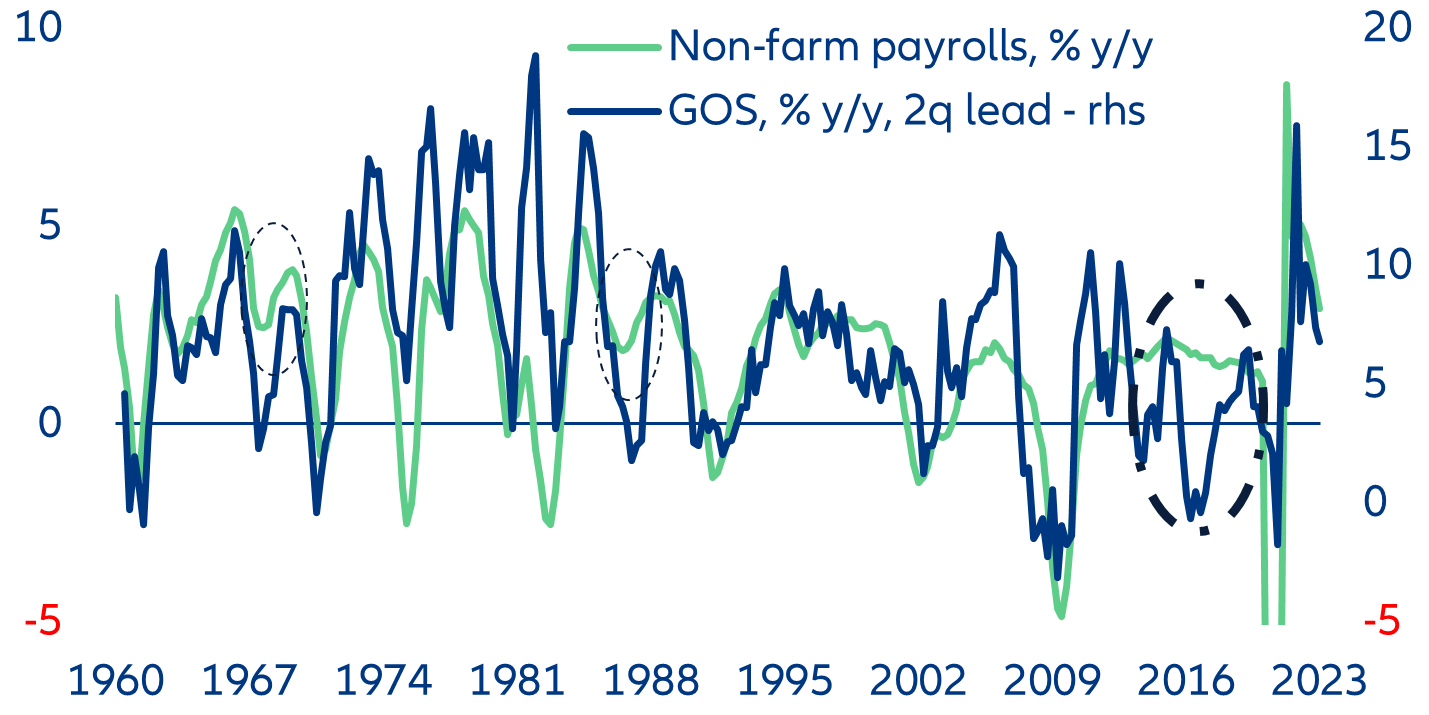

Amid deteriorating demographics and difficulty in hiring after the pandemic, we believe that companies will favor staff-hoarding strategies even as growth slows sharply by the end of the year. Weakening demand induced by rising interest rates is already making a dent on companies’ margins, which have been falling on a q/q sequential basis since Q4 2022. Yet companies continue to hire, an unusual but not unique pattern last seen in the 1960s, during the end of the 1980s and in 2016-17 (Figure 1). Labor costs seem to adjust via lower working hours: Private weekly hours workers per head have dipped to their lower 2011-2019 bound in May. We expect the unemployment rate to peak at 4.2% in Q2 2024, from 3.6% in Q2 2023.

Figure 1: Gross operating surplus (GOS) and non-farm payrolls growth

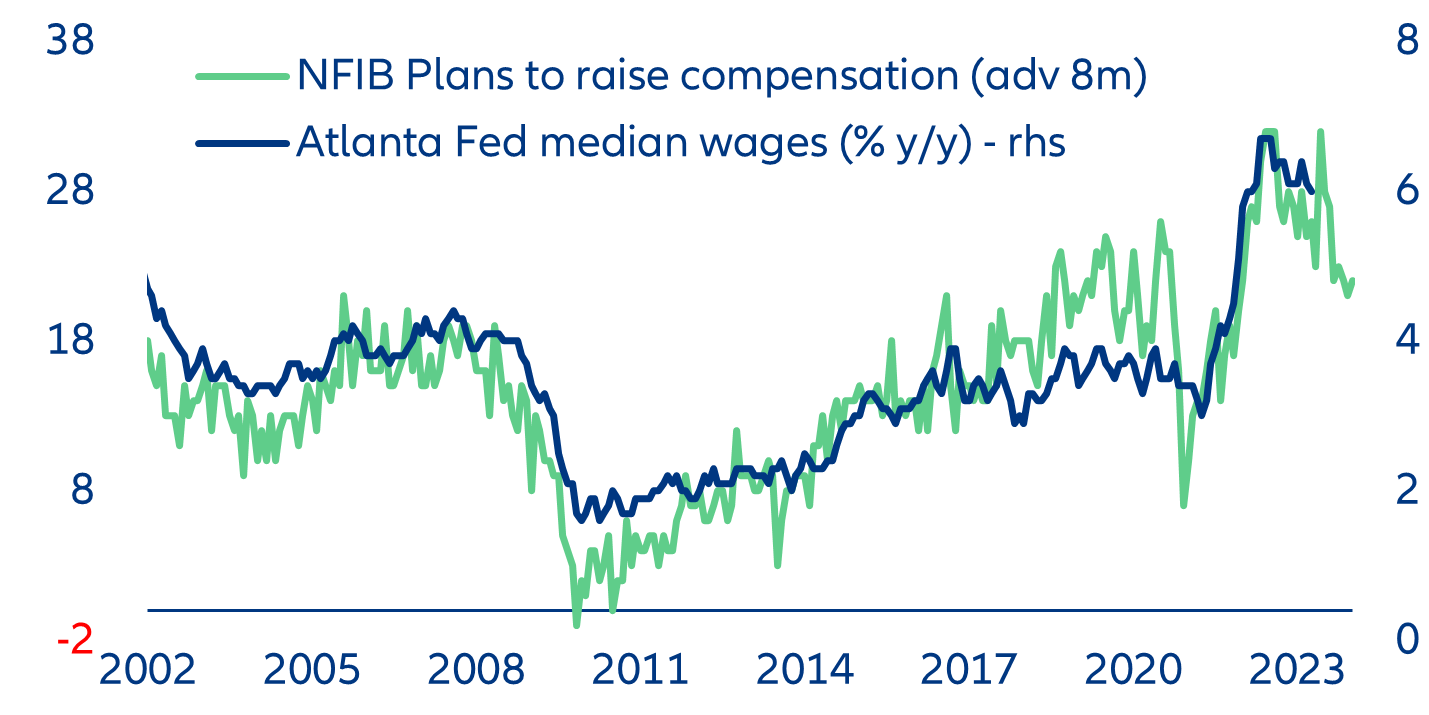

The Federal Reserve is not done with rate hikes. Even though disinflation is strengthening and the labor market is getting less tight, the Fed remains focused on current core services inflation and wage-growth prints (‘data-dependent’), which are still inconsistent with its 2% inflation target. According to the NFIB survey, wage growth as measured by the Atlanta Fed wage tracker (our preferred measure of underlying earnings growth) should pull back to around +4.5% by the end of the year, vs +6% presently (Figure 2). That would still be a little too strong for the Fed’s liking. It (rightly) sees +3-3.5% wage growth as compatible with 2% inflation. Amid economic resilience and elevated core price pressures, we think the Fed will deliver two last rate hikes of 25bps in both the July and September meetings, though the September hike is far from being certain. We expect the squeeze in profit margins and a further easing of wage growth through 2024 (amid entrenched medium-term inflation expectations) to do the trick to push core inflation close to 2% by next summer.

Figure 2: Wage growth and NFIB survey

China’s increasing constraints call for more (policy) action

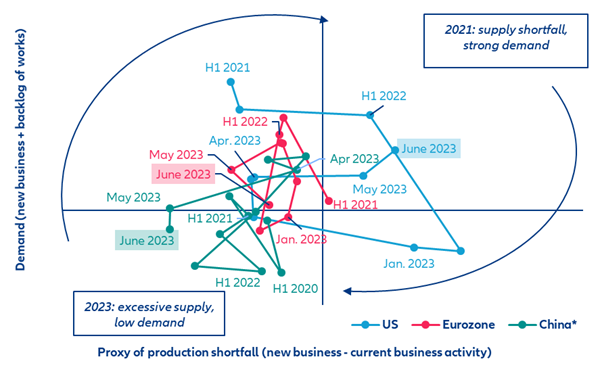

As expected, China’s economic growth continues to lose steam: soft business sentiment data for both manufacturing and services in June support our GDP growth forecast of only +1.3% q/q in Q2, down from +2.2% in Q1. A NBS Manufacturing PMI reading of 49.0 and a decline of the Caixin Manufacturing PMI to 50.5 (down from 50.9 in May) underscore sluggish economic activity in manufacturing. Activity in services is also slowing. The NBS Non-manufacturing PMI declined to 53.2 for June (down from 54.5 in May), and the Caixin Services PMI hit 53.9 (down from 57.1 in May).

Figure 3: Non-manufacturing PMI “Supply – Demand Clock”

Sources: Refinitiv Datastream, Allianz Research

Export demand is slowing, which has increased oversupply. The new export orders sub-index fell across both indices. In the NBS Non-manufacturing PMI, the sub-index remained below the 50 mark at 49.0 in June, down 0.7 points from May when it fell into contractionary territory after having reached 52.1 in April. Overall, prospects are expected to remain depressed as we expect a broad-based trade recession in 2023 (-0.7% in volume and -2.1% in value). Global spare capacity has reached its highest level in three years.

Deflationary pressures are intensifying. The input and output price sub-indices suggest that prices kept falling for both construction and services sectors, although at a slower pace compared to May. In the manufacturing sector, amid easing delivery constraints and falling demand, deflationary pressures have strengthened, which shows in the softening of sub-indices for input prices. PPI prices fell by close to -4.6% y/y in May and inflation should decline to less than 1% by end-2023. This warrants at least one more rate cut (-10bps) by Fall this year (to 3.45% for the one-year Loan Prime Rate and 7% for the Reserve Requirement Ratio, which should boost traditional funding and the limit the rise in shadow banking.

The labor market is under pressure, which does not bode well for consumer confidence. In the manufacturing sector, the employment sub-index remained well below the 50 mark. But it is a mixed picture in services: The equivalent sub-index of the Caixin rose slightly to 51.9 in June from 51.5 in May, suggesting an improving labor market in the services sector while it was deteriorating in the NBS survey. In construction, the NBS survey showed a deteriorating outlook for employment. That does not bode well for consumer confidence. Youth unemployment is over 20%, on the back of skills mismatches, and some migrant workers have taken lower-paid service jobs this year instead of working in export factories, given the weakness of external demand, notably in advanced economies.

In this context, more policy support is needed. In response to the slowdown, policymakers are trying to implement further counter-cyclical measures, including recently approved support for home-related consumption. The recent State Council meeting also deliberated on further measures to boost consumption and increase spending on urban renovation projects. Policymakers are likely to avoid implementing broad-based stimulus (such as large cash handouts to households), focusing rather on targeted fiscal measures going forward, including the increase in local government special-bond quotas. The share of annual quotas stood at 61.7%, much below 2022 levels.

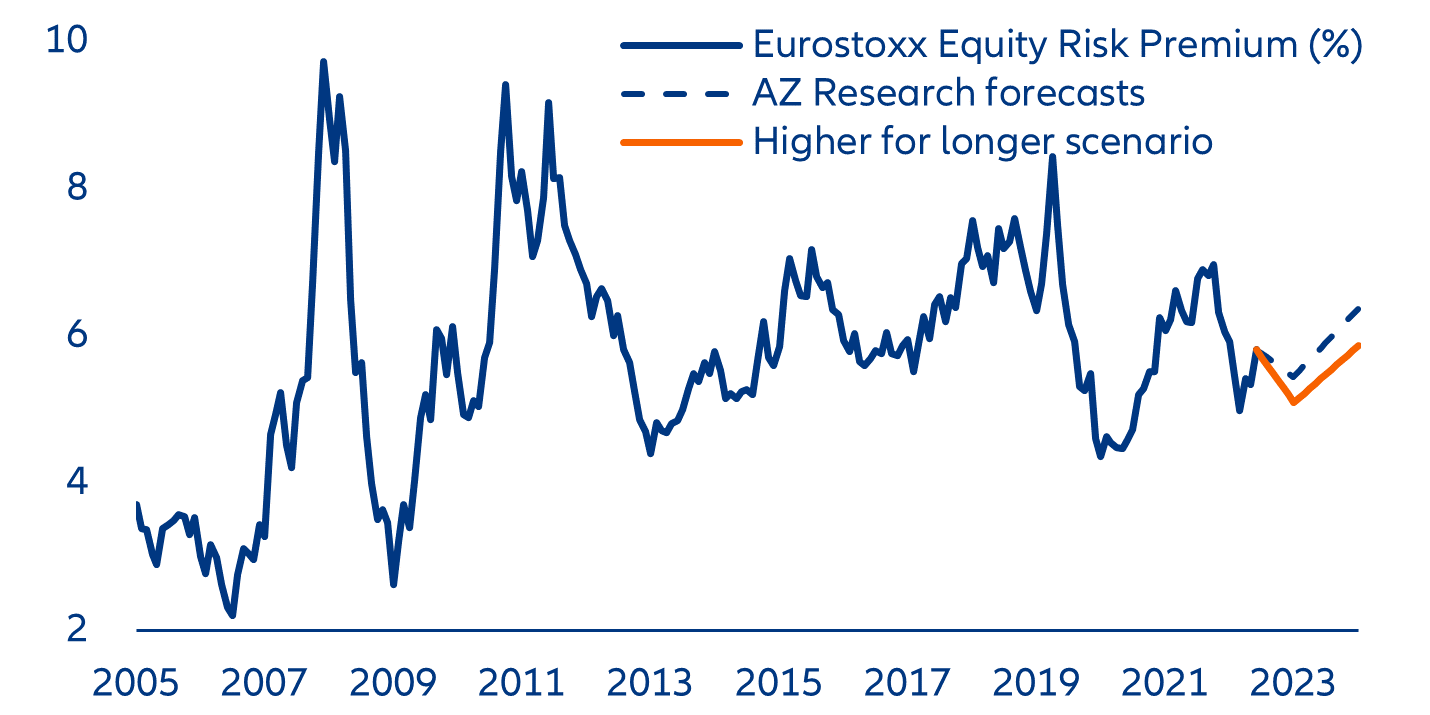

China’s re-opening has not boosted capital markets. Even though opportunities remain compelling given the large size of China’s economy and still strong growth prospects, valuations are far lower relative to other major markets in advanced economies. The equity risk premium is about four times as high as in the US (Figure 5). While low correlation with major markets should be attractive during a time of limited diversification possibilities, capital account restrictions make foreign investment less efficient.

Figure 5: Equity Risk Premium (ERP) in selected equity markets

Sources: Refinitiv Datastream, Allianz Research. Notes: EMU=European Monetary Union; 1/ MSCI benchmark indexes used; 2/ South Korea has been used as the reference among large EMs, since other large markets such Brazil and India have structural negative ERP (based on this methodology, i.e., using IBES 12M forward EPS and 10Y yield).

We expect some improvement during the second part of this year, but this will not be enough to offset year-to-date losses amid persistent headwinds from a weakening currency. China’s flat price performance overall is likely to weigh on emerging markets, which are bound to underperform vis-à-vis the Eurozone and the US in 2023, except for Latin America and the rest of Asia-Pacific. When it comes to corporate credit, policy support has not fully restored confidence and foreign portfolio outflows show no signs of abating, while liquidity in the high-yield spectrum remains very thin.

What if the ECB goes “higher for longer”?

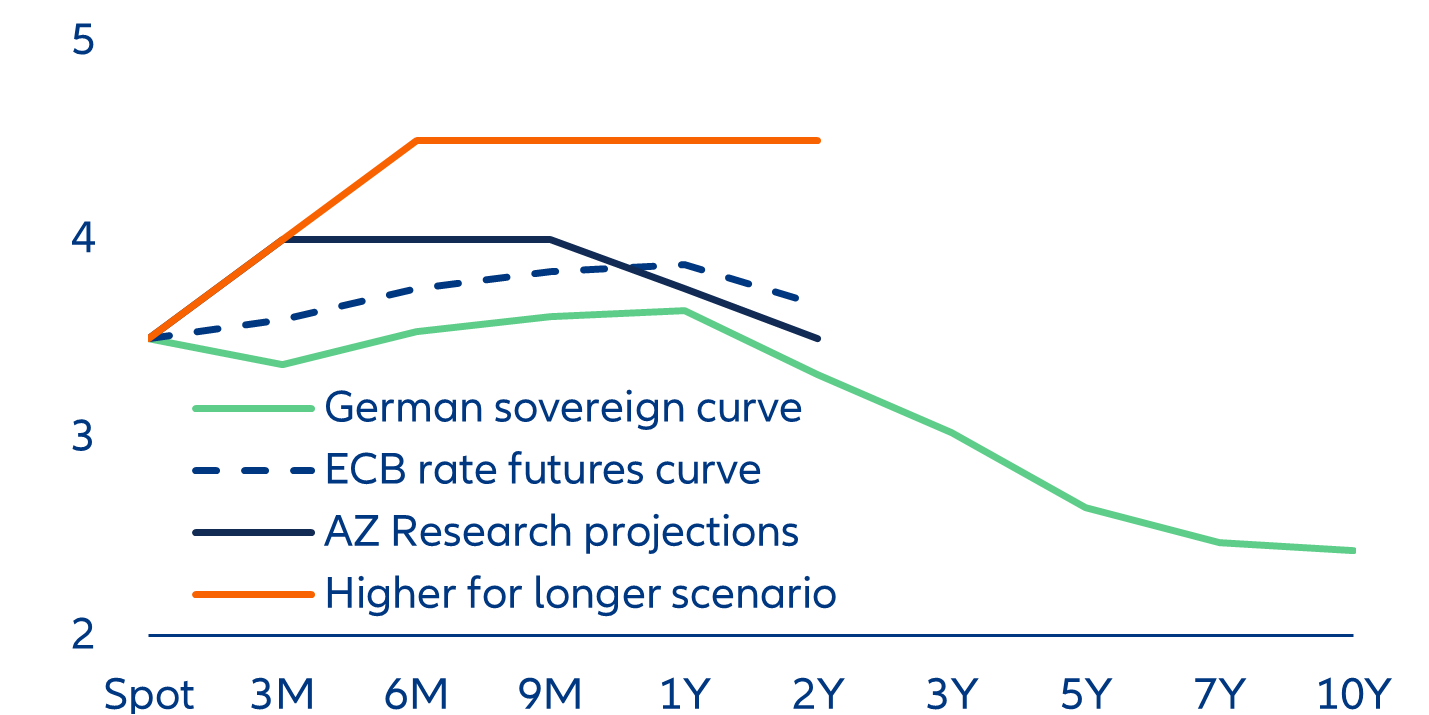

Stronger-than-expected core inflation has lowered the bar for the ECB to keep interest rates higher for longer. While headline inflation for June came in line with expectations at 5.4% y/y (down from 6.1% y/y in May), core inflation increased to 5.4%Y (up from 5.3% y/y in May). Services inflation has risen again to 5.4% y/y (from 5.0% y/y in May) as expected, and with a notable base effect from the EUR9 ticket in Germany. Goods inflation decreased to 5.5% y/y (from 5.8% y/y) but less than expected. On a monthly basis, price changes are now much weaker than they were in early 2023 and disinflationary forces (outside services) are gaining momentum as monetary supply keeps declining. Even before the recent inflation data releases, we had already revised up our terminal expectation for the ECB to 4.0%,[1] assuming that it will continue to hike even after its July meeting by another 25bps in September. However, what is more important is the increasingly hawkish tone from the ECB, which became apparent at last week’s Central Bank Forum in Sintra. The divergence between the forecasts of the national central banks (June and December) and the forecast of the ECB (March and September) on the stickiness of inflation has raised the degree of data dependency in the ECB’s policy-rate path. It seems unlikely that the ECB will forecast meeting its medium-term price stability target of 2% before the end of 2025, which would could postpone potential rate cuts from June 2024 (our current forecast) to 2025.

Figure 6: ECB rates and German sovereign curve projections (in %)

Sources: Refinitiv Datastream, Allianz Research

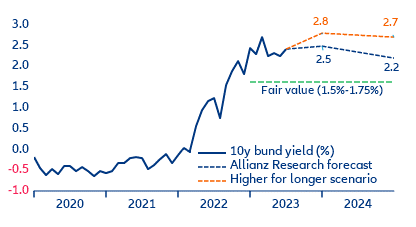

The prospect of a more prolonged period of tighter monetary policy would exert upward pressure on both ends of the yield curve. We examine the impact of a “higher-for-longer” scenario in which the ECB raises the deposit rate to 4.5% without rate cuts until end-2024. This scenario significantly deviates from market consensus (+75-100bps) and would lead to a notable market correction (Figure 6), including on the long end of the yield curve. The current pass-through effect of changes in the one-year-ahead policy-rate expectations to the ten-year German Bund yield is approximately 70%. This implies that for every 100bps change in expectations, around 70bps are absorbed by the longer end of the German yield curve. Thus, the 10-year Bund yield would rise to 2.8% and 2.7% until the end of 2023 and 2024, respectively (up from the current level of 2.4%). Additionally, it would indicate a 30bps and 50bps upward deviation from our baseline forecasts for 2023 and 2024, respectively, and widen the gap to the fair value rate of 1.5% and 1.75%, respectively (Figure 7).

Figure 7: 10-year Bund yield projections (%)

Sources: Refinitiv Datastream, Allianz Research

Higher long-term yields would weigh on equity markets. Extended higher rates would also impact riskier assets, tilting the cross-asset attractiveness in favor of fixed-income investments due to the increasingly attractive yields. This effect would primarily manifest in 2023 as the anticipated resurgence in earnings for 2024 would stimulate equity performance and narrow the gap in relative attractiveness in favor of equity markets. Quantitatively, a higher-for-longer scenario would potentially reduce equity performance by approximately 3 to 4% in 2023, compared to our expected 9% total return for the Eurostoxx (Figure 8).

Figure 8: European equity market performance (%)

Sources: Refinitiv Datastream, Allianz Research

In focus – Eurozone convergence: two steps forward, one step back

The “European project” finds itself – yet again – at a critical stage of development that requires safeguarding its economic future amid rising geopolitical tensions and domestic pressures. The pandemic and the energy crises stress-tested the EU’s resolve in forming a strong political consensus. It emerged battle-hardened but severely weakened economically. At its heart, the Eurozone has slipped back into recession amid still far-too-high inflation. At the end of this year, the bloc’s economy will be barely larger than it was before the pandemic – equivalent to four lost years. However, strong growth and productivity are a necessary, if not sufficient, condition for Europe’s economic self-determination. Rising geopolitical tensions between the US and China (and more broadly the “collective West” vs. the “collective East”) amplify security concerns in national politics and economic policy – and challenge Europe’s mercantilist growth model underpinned by a strong commitment to globalization. At the same time, cracks in the system have become more apparent and require more focus on the domestic agenda, including rising inequality (e.g. inefficient labor markets and lagging regions), political ambiguity (e.g. a sense of loss of control and accountability) and pressing secular challenges (e.g. climate, demographics and technology).

In this context, the European Commission’s new Economic Security Strategy could not have come sooner, with its focus on boosting Europe’s competitiveness and deepening the Single Market as a priority for safeguarding economic security. But it is also complicated by an uneven recovery from the recent crises. Some sectors and firms have yet to fully recover (or might slowly disappear), while others are set to expand more rapidly, including those benefitting from less dependence on fickle trading partners, deeper technological changes and the transition towards a greener economy. This means that there will be some economic scarring, albeit significantly less than in the period following the global financial crisis, which will vary considerably across member states. Restoring trend growth will be challenging, especially in regions of Europe that have been falling behind.

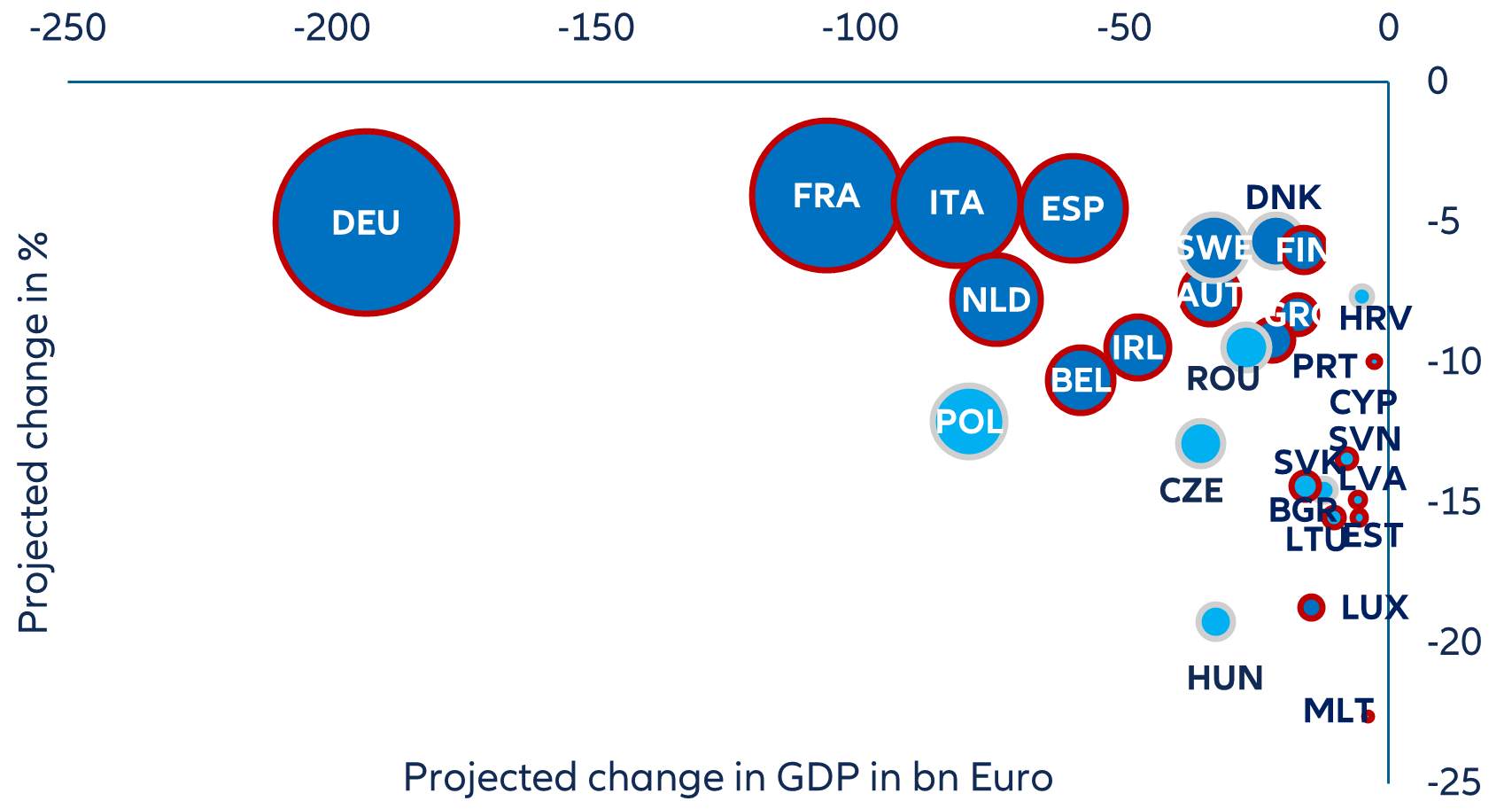

Figure 9: EU – counterfactual change in GDP without European trade and financial integration (2022, % and in EUR bn)

Sources: Eurostat, Felbermayr, Gröschl and Heiland (2022), Allianz Research. Notes: baseline estimates for 2014 GDP levels are applied to GDP in 2022; “new” EU member states (which joined the bloc in 2003, 2006 and 2013) are in light blue; Eurozone member states are marked by a red border.

The Eurozone needs to pivot from crisis-fighting to the future by building strength from within through greater integration and convergence. Going forward, the key policy challenge is to re-energize the recovery, limit the long-term output loss and transform economies, including by fostering a smooth reallocation of resources and investing in climate-friendly and digital infrastructure paired with a security-oriented and strategic (re-)organization of essential trade relationships. However, current policy choices also raise legitimate concerns about whether the pre-crisis differences in views regarding evolving reforms of the Eurozone architecture will resurface once again. And differences in views could grow if the convergence across Eurozone countries keeps stalling, which seems likely.

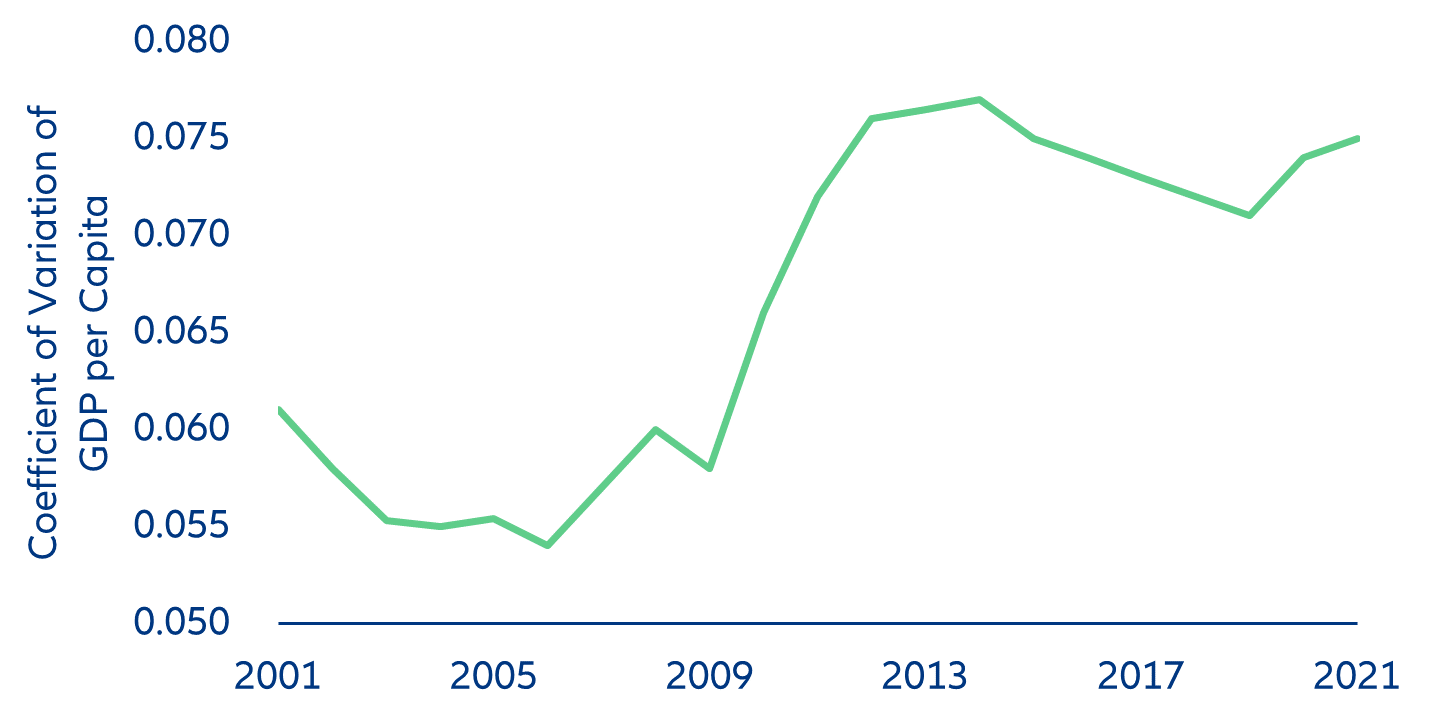

Figure 10: Eurozone – scale of regional disparity*

Sources: Refinitiv, Allianz Research. Note: */ includes Austria, Finland, France, Germany, Greece, Italy, Netherlands, Portugal and Spain (as well as the UK for the years before Brexit).

The Economic and Monetary Union (EMU) has been a clear political and economic success, which has helped increase the convergence across countries. The common market has boosted trade within the bloc and strengthened its resilience during economic downturns. The Eurozone benefits massively from enhanced economic integration and subsequent growth opportunities. In a hypothetical world without EU membership and financial transfers, Eurozone countries would have lost about 10% of GDP on average in 2022 (Figure 9), with smaller, more open economies facing a bigger impact. The German economy would be about 5% smaller (-EUR194bn), followed by France at -4% (-EUR106bn). Malta, the smallest Eurozone member in terms of GDP, would lose nearly a quarter of its economy but the least in absolute terms, with GDP declining by about -EUR4bn.

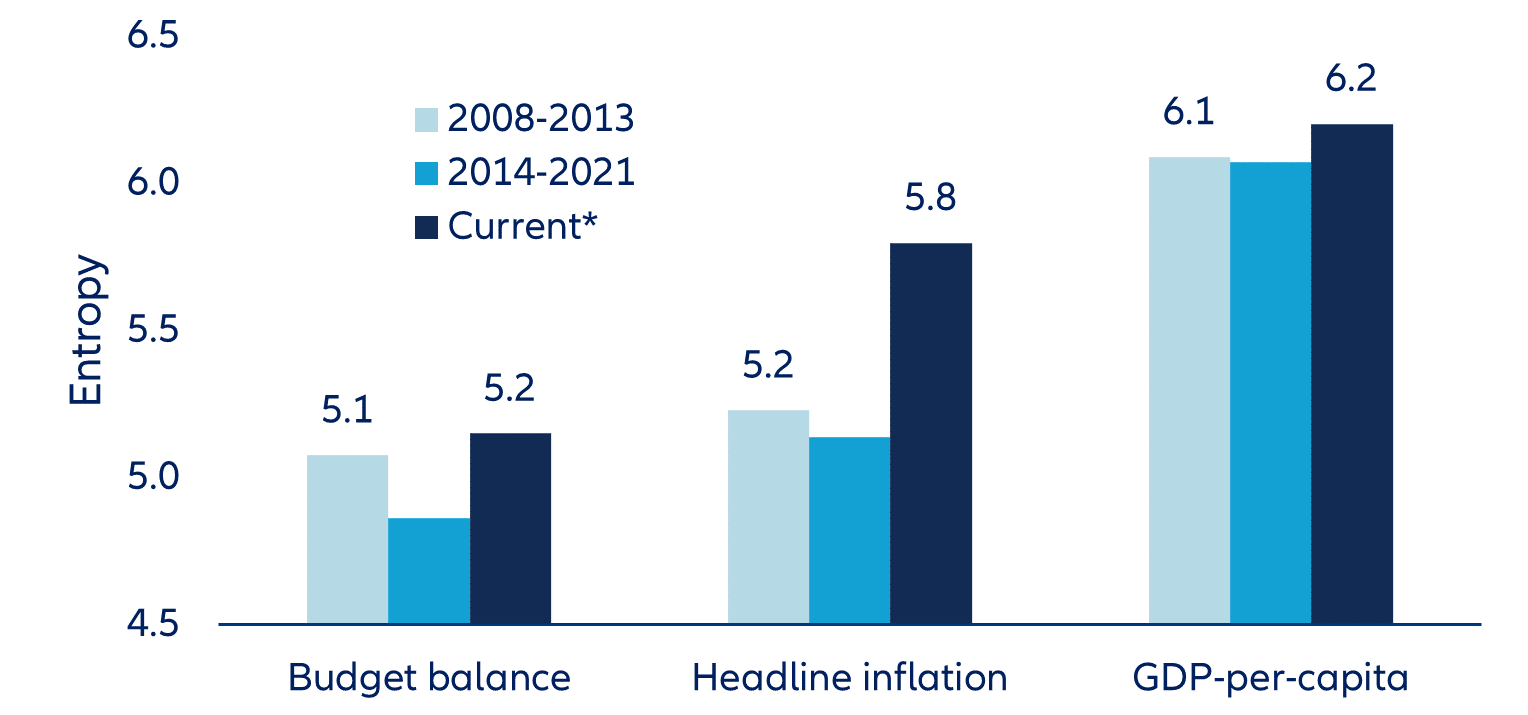

Figure 11: Eurozone – dispersion of key economic variables (average)

Sources: Refinitiv, Allianz Research

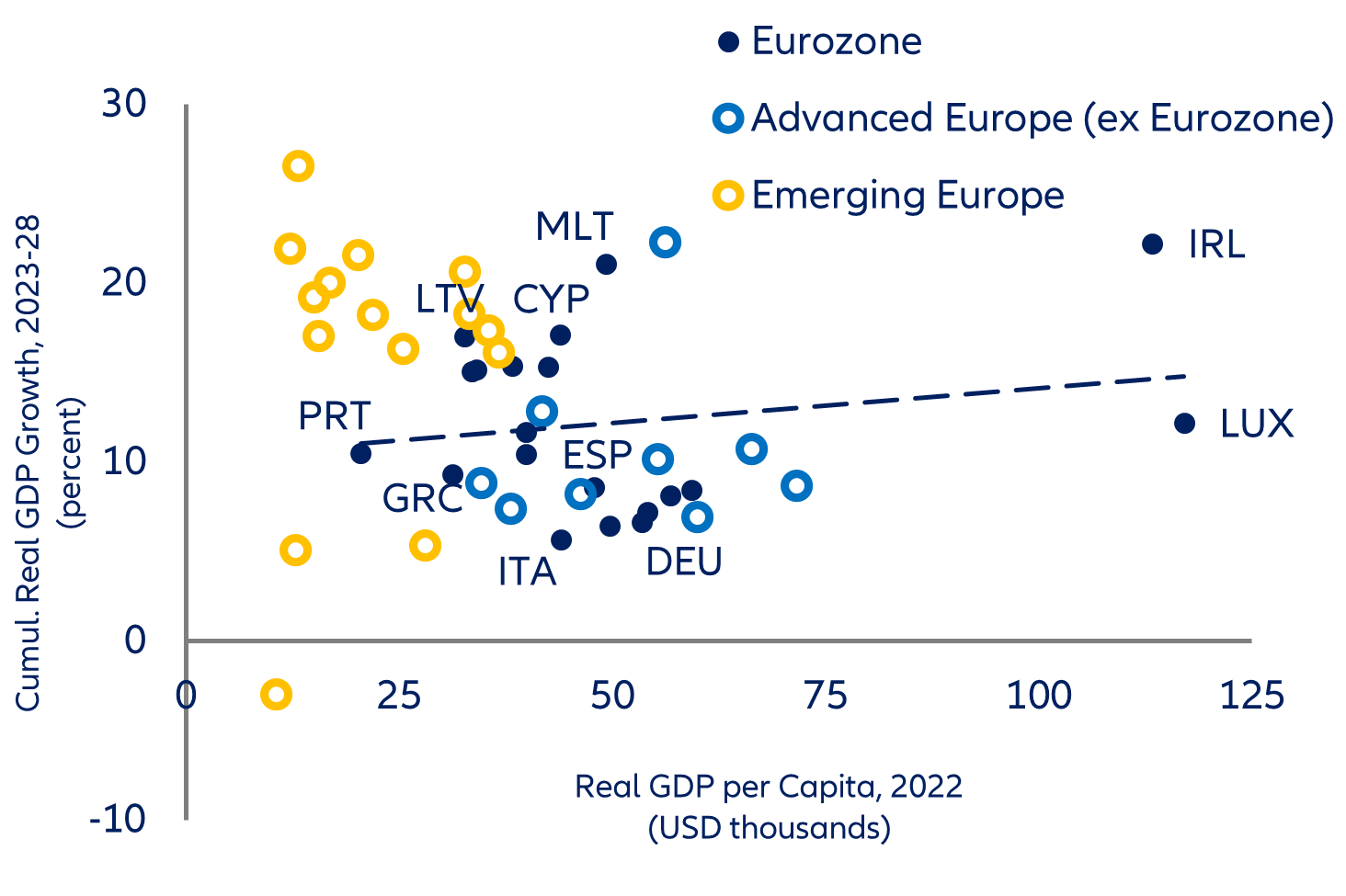

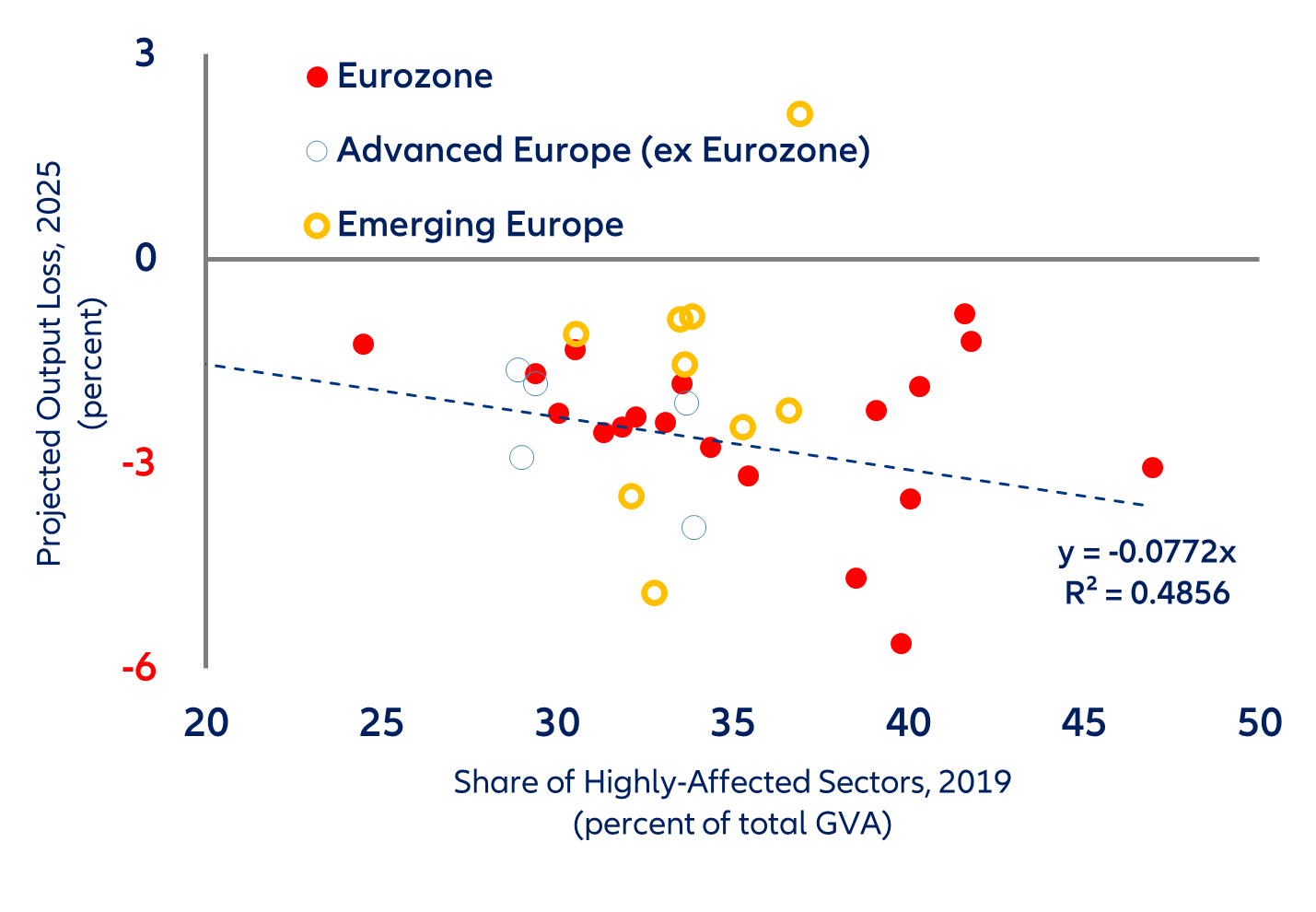

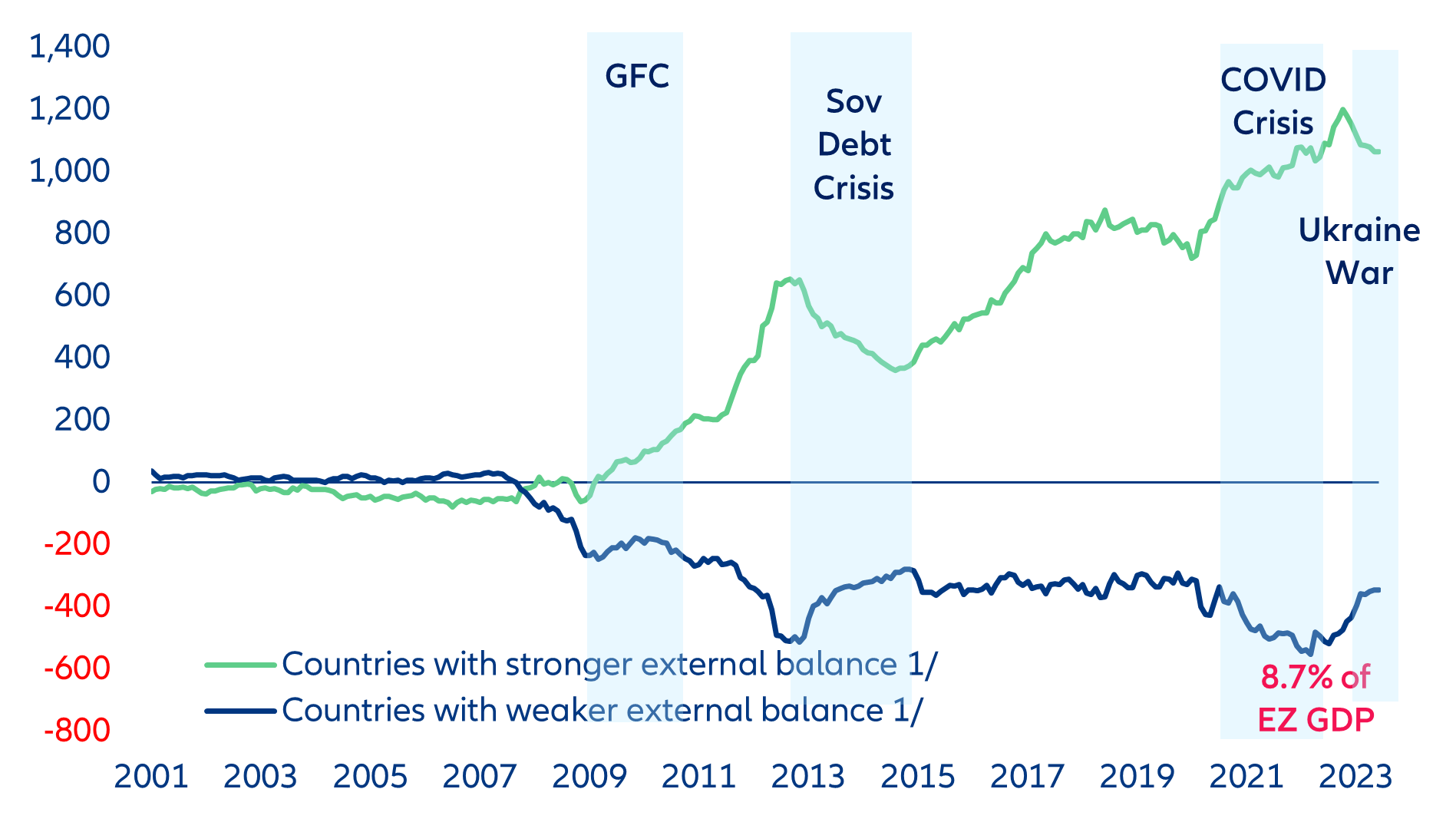

However, divergence has increased again in recent years, and regional disparities in particular are on the rise (Figures 10 and 11). In addition, the uneven recovery from the crises is set to increase the income gap as projected growth remains broadly the same across most member countries with still large differences in GDP per capita (Figure 12). The income divergence reflects various factors, including the varying impact of the pandemic and energy crises, pre-crises vulnerabilities, policy responses and economic structure. Looking only at the scarring effects from the pandemic, Figure 13 illustrates that the output loss in 2025 is projected to be more severe in countries with a higher share of “highly-affected” services. Structural factors, such as differences in labor productivity, labor force participation and demographics, have held back economic convergence prior to the crises and are now likely to exacerbate the adverse effects of the pandemic and the war in Ukraine on economic activity. At the same time, the divergence of TARGET2 balances, the Eurosystem’s large-value payment system, has continuously widened. While the liabilities of national central banks in more vulnerable member countries to their peers in the rest of the Eurozone have declined over the last 1.5 years due to quantitative tightening, they remain at more than 8% of GDP (Figure 14).

Figure 12: Europe – GDP-per-capita and growth (percent, US thousand dollars)

Sources: Refinitiv, Allianz Research

Figure 13: Europe – share of highly-affected sectors vs. output loss (percent, percent of total GVA) 1/

Sources: Eurostat, Refinitiv, Allianz Research. Note: GVA=gross value added; 1/ highly-affected sectors include trade, travel, accommodation and food services, real estate, arts and entertainment; output loss is compared against the pre-Covid trend; excludes Ireland due to scaling.

Figure 14: Eurozone – Target 2 net balances (EUR bn)

Sources: ECB, Allianz Research. Note: GFC=global financial crisis; 1/ countries with a traditionally negative current account balance and/or weaker fiscal position.

Clearly, this trend warrants asking the critical question as to how the Eurozone can achieve meaningful convergence. Deepening the EMU requires greater financial integration and better coordination of fiscal policies.

- Banking Union: The pandemic and the energy crises have not precipitated a banking crisis, in part because banks were much better capitalized and less risky than before the GFC. Despite the single supervision and resolution of banks, the Banking Union remains incomplete, with attendant risks of potential fragmentation during times of stress. In recent years, progress to close important gaps, such as the design and implementation of the European Deposit Insurance Scheme (EDIS), has lost momentum and will require a new push to reach consensus and encourage greater cross-border banking. While the European Commission has adopted a proposal to adjust and further strengthen the EU’s existing bank crisis-management and deposit-insurance (CMDI) framework, with a focus on medium-sized and smaller banks, it ignores the role of effective national institutional protection systems and the importance of EDIS (also in resolution) for completing the Banking Union.

- Capital Markets Union (CMU): Increasing cross-border private risk-sharing and reducing firms’ reliance on bank financing in Europe requires better integrated capital markets. Advancing the capital markets union is critical to EU resilience. Capital markets should also play a key role in financing the transition to a greener, more digital economy. The new 2020 CMU action plan identified several steps needed to “reboot” the EU’s push for greater capital market integration. Fast implementation of these recommendations would make access to market-based finance easier and lessen firms’ reliance on bank borrowing.

- Fiscal framework: Credible EU fiscal rules are essential for an effective monetary union. Earlier this year, the European Commission proposed the most ambitious overhaul of the EU fiscal framework in more than two decades. The focus on a simplified expenditure-growth rule as a single operating target (and removing the structural-balance rule) offers an opportunity for vulnerable Eurozone economies to gradually reduce their budget deficits while making the necessary investments to boost potential growth. Retaining a focus on growth-enhancing spending would be critical for the country to stabilize debt once current cyclical pressures from the energy crisis abate and give way to structural challenges from the green transition. Recognizing that countries have emerged from the crises with elevated debt levels, preserving a deficit rule anchored to nominal growth with a more flexible adjustment period for fiscal consolidation seems to be a reasonable solution. But not excluding public investment from the limits of the fiscal rules should raise concerns; Europe’s central fiscal capacity for more public investment remains too small.