- The outlook for Central and Eastern Europe (CEE) has slightly improved in recent weeks due to diminishing headwinds from lower-than-expected energy prices.

- Nonetheless, growth in the CEE-4 (Poland, Czechia, Romania, Hungary) remains subdued overall as the impact of continued high inflation, increased interest rates, weaker external demand and lower business confidence will take full effect this year.

- Inflation has peaked in most CEE economies and the disinflation process may be happening slightly quicker than previously expected. However, inflation will remain above central banks’ targets over the next two years.

- Central banks in the CEE-4 were the first to halt their interest rate hiking cycles and, barring any new shocks, we expect some of them to also be ahead of the curve when it comes to the pivot. We expect Czechia to start easing in June 2023, followed by Poland in Q3 and Romania and Hungary at the end of the year.

In Focus

Monetary policy in Central and Eastern Europe ahead of the curve?

Market Movers

- German stagnation—rising insolvencies? German business insolvencies are rebounding albeit from a low level.

- US real estate—trouble (still) ahead? Some housing market indicators have stabilized, but downside risks continue due to weaker domestic activity. The outlook for commercial real estate remains negative, especially for the office sector.

- Making up for inflation—how Jane and Maxi can get their groove back. Investors holding a 60/40 portfolio of equities/bonds lost about ~20% on average last year; it will take them more than three years to fully recover their losses.

- Corporate performance—will inflation continue muting spending in 2023? Earnings have been weak for discretionary sectors, with EPS growth averaging -1.6% globally, though distributors and specialty retail performed significantly worse.

German stagnation—rising insolvencies?

The outlook for Germany’s economy remains bleak despite improving business expectations. The slightly more upbeat message from recent survey data (ifo and ZEW sentiment indicators) was solely driven by better expectations, which still stand at historically low levels. Firms in the services and manufacturing sectors still report weaker current activity (amid declining orders), and uncertainty in the energy-intensive sectors has increased further. Industrial production, especially in energy-intensive sectors, considerably slowed in December (-3.9% y/y and -3.1% m/m, down from +0.4% m/m in November). Production in the energy-intensive sectors is now down by almost -20% compared with December last year. We continue to project a moderate recession in Germany (with negative growth also in Q1 2023 after a contraction of -0.2% q/q in Q4 2022), followed by a subdued recovery after mid-2023 and weak growth in 2024 as financing conditions are likely to remain tighter for longer (Figure 1).

Figure 1. Germany: industrial production

Sources: Refinitiv Datastream, Allianz Research

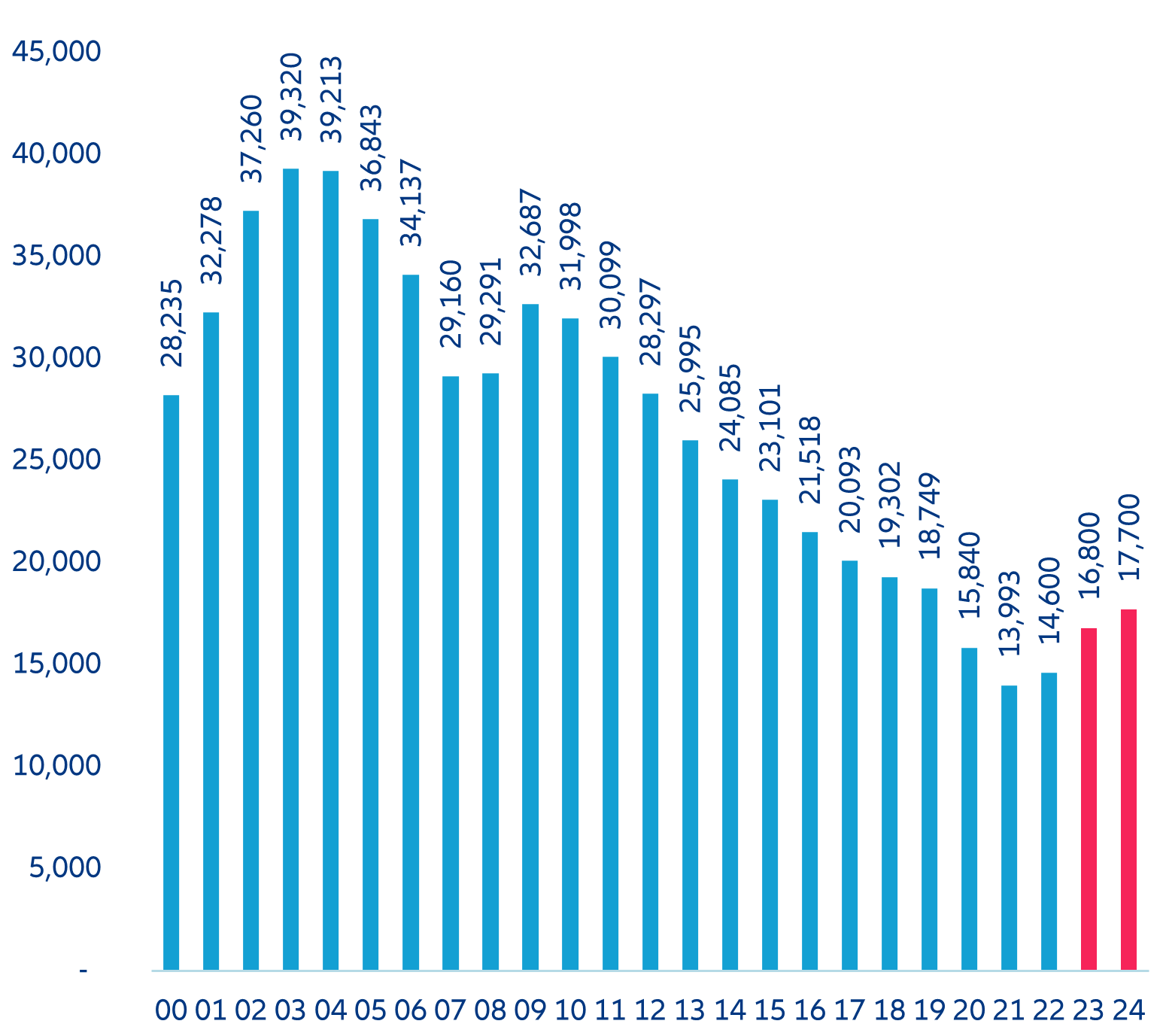

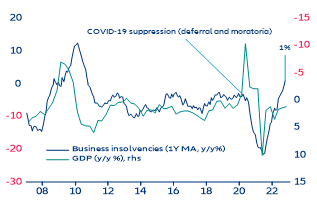

German business insolvencies are rebounding albeit from a low level. The current economic weakness has not left companies unscathed. Despite improving expectations (and scaled-up government support), more and more companies are coming under pressure due to the persistent triple threat of higher input prices, rising labor costs and tighter financing conditions weighing on business prospects. Extrapolating the trend from official data on insolvencies until October, the number of insolvencies is likely to have reached 14,600 cases in 2022, up by +4% over the year after a +19.5% increase in the last quarter. We expect insolvencies to continue increasing to 16,800 cases (+15%) this year (Figure 2). In fact, the one-year moving average of changes in insolvency cases indicates that the pace of new cases brought to German courts has been the highest since the European debt crisis (Figure 3). That said, the number of insolvency cases remains historically low; as a result, the noticeable increase of insolvencies over the last few months implies only a gradual normalization rather than an impending wave of bankruptcies. Germany’s corporate sector still looks comparatively robust compared to other countries. Globally, we expect insolvencies to rise by another +19% this year, reaching pre-pandemic levels (after +10% last year).

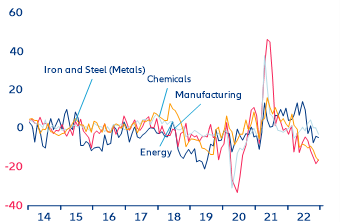

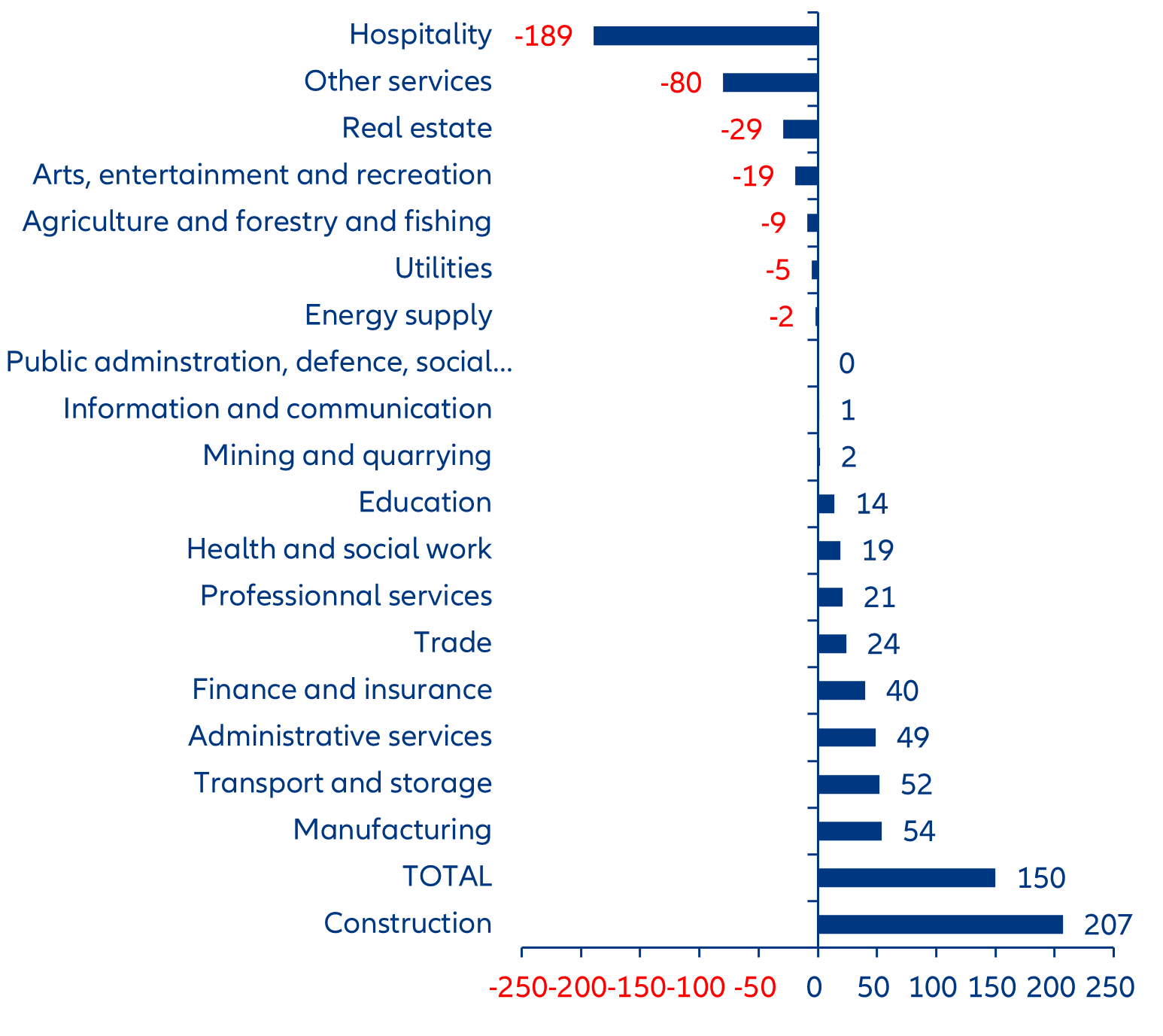

Sectors most exposed to energy and input prices are more at risk, with significant variation within sectors, especially in manufacturing. Construction tops the list (+207 cases ytd, +10%), ahead of manufacturing (+54 cases, +7%) and transport/storage (+52, +6%). However, several sectors have been spared so far, such as hospitality and real estate, where insolvencies have declined. Firms in the manufacturing sectors are unevenly exposed to current challenges. We see a faster increase of insolvencies mostly in data-processing equipment and electronics (+16), rubber and plastic goods (+16), furniture (+14), foodstuffs and fodder (+13). Insolvencies increased moderately in the trade sector, which remains the second-largest source of bankruptcies after construction (Figure 4).

Figure 2. Germany—insolvency cases (annual)

Sources: DeStatis, Refinitiv Datastream, Allianz Research

Figure 3. Germany—GDP growth and insolvency cases (one-year moving average)

Sources: Refinitiv Datastream, Allianz Research

Figure 4. Germany—change in insolvency cases (by sector)

Sources: DeStatis, Allianz Research

US real estate—trouble (still) ahead?

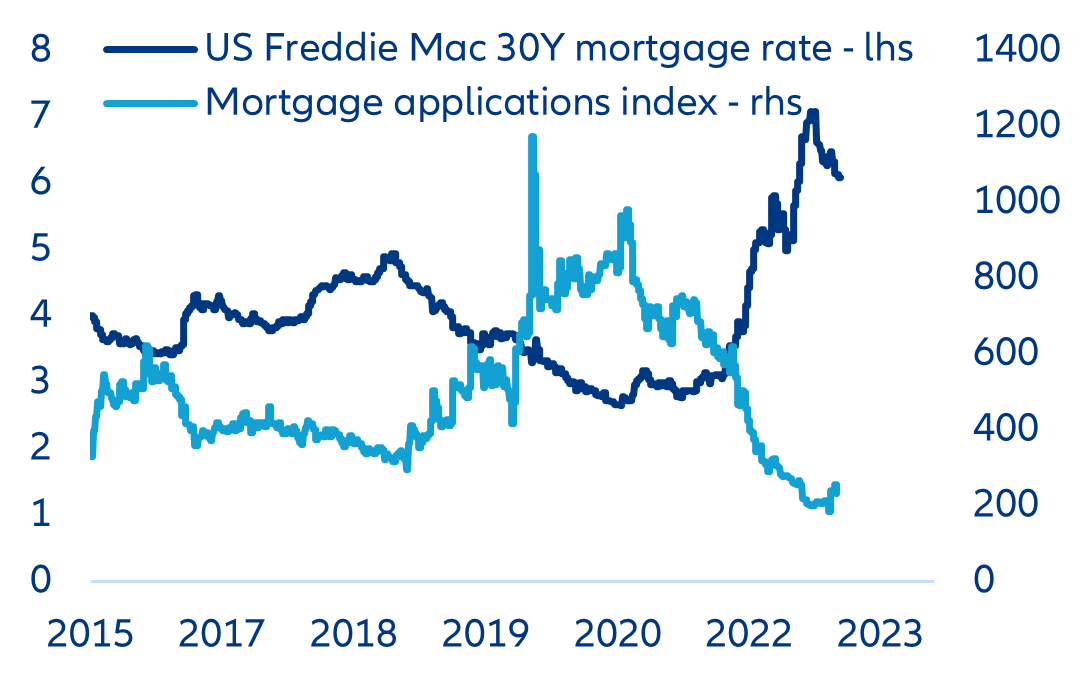

Some US housing market indicators have stabilized but downside risks due to weakening domestic activity prevail. The rapid rise of interest rates and quantitative tightening have resulted in a contraction of money supply, measured by M2, by more than -2% while average mortgage payments have increased by more than +80%. The decline in home affordability has been unprecedented – before the Federal Reserve started hiking rates, about three-quarters of US households could afford to buy a home; this number has declined to about 10% during the last year. However, as the hiking cycle is close to reaching its peak, long-term yields have stabilized and mortgage rates have adjusted lower (Figure 5). Likewise, the sharp decline in home affordability halted during the last quarter of 2022, with slight improvements expected.

Figure 5. Mortgage rates vs. mortgage applications

Sources: Refinitiv, Allianz Research

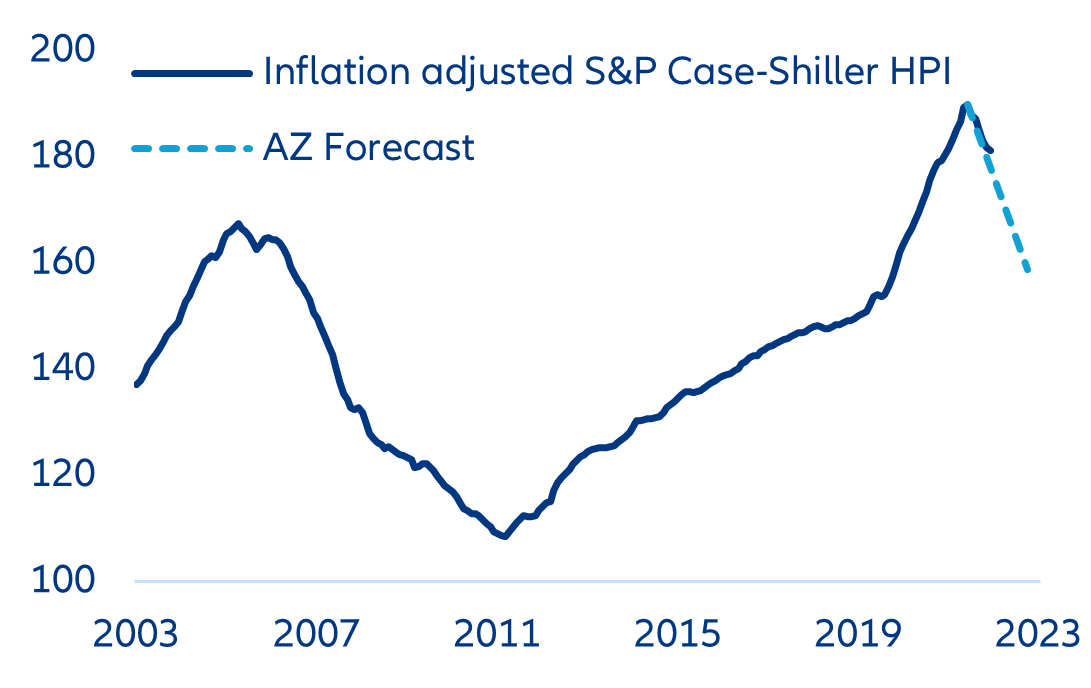

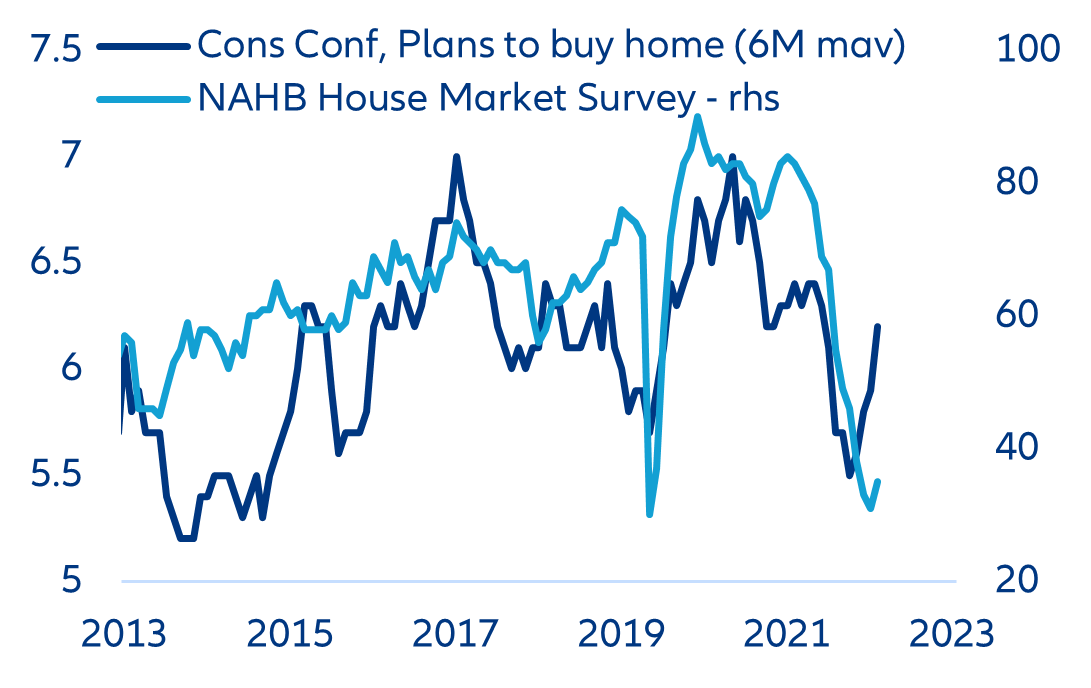

A further price correction in the housing market is likely but will not cause financial stability challenges. So far there has been no uptick in delinquent mortgage loans nor on foreclosures (besides the adjustment after the expiration of Covid-19 measures) and the labor market is proving stronger than anticipated, which could prevent large-scale force-selling. While existing home sales have fallen below Covid-19 lows, the mismatch between the supply and demand of new houses slightly improved in Q4 2022. Plans to buy homes have rebounded, while the supply-side sentiment seems to have bottomed out (Figure 6). In addition, inflation dynamics suggest some stabilization. From the builders’ perspective, and after a tough 2021, construction-materials inflation in 2022 has eased considerably and we have even seen some deflation in Q4. In September, we forecasted a -15% price correction in the US housing market until end-2023. So far, we have seen a decline of slightly more than -4% (Figure 7), which is consistent with our forecast and our outlook for the US economy. Next week, the release of housing starts data will give us a sign of whether the incipient reversal of the downward trend will continue.

Figure 6. Inflation-adjusted House Price Index

Sources: Refinitiv, Allianz Research. 100 = Q1 1980

Figure 7. Supply vs. demand sentiment with regards to the housing market

Sources: NAHB, Refinitiv, Allianz Research

The outlook for US commercial real estate remains negative, especially for the office sector. Recently released data for Q4 2022 confirm price declines for both office and retail. Investment volumes also saw a severe contraction in 2022. The office vacancy rate ticked up last year, which will help push prices further down. Higher market rents (which typically lag) have not matched the rise in inflation and interest rates, which helped push last year’s commercial property returns to the second-lowest level since the Global Financial Crisis (only after 2020). REITs are showing signs of becoming the emerging trouble spot as investors start to withdraw money in large amounts. Besides the good start to the year, most listed REIT indexes in the US are down between -15% and -30% compared to their valuations at the end of 2021. Office REITs are notably the worst performers, while hotels are the only exception due to their lagged post-Covid recovery.

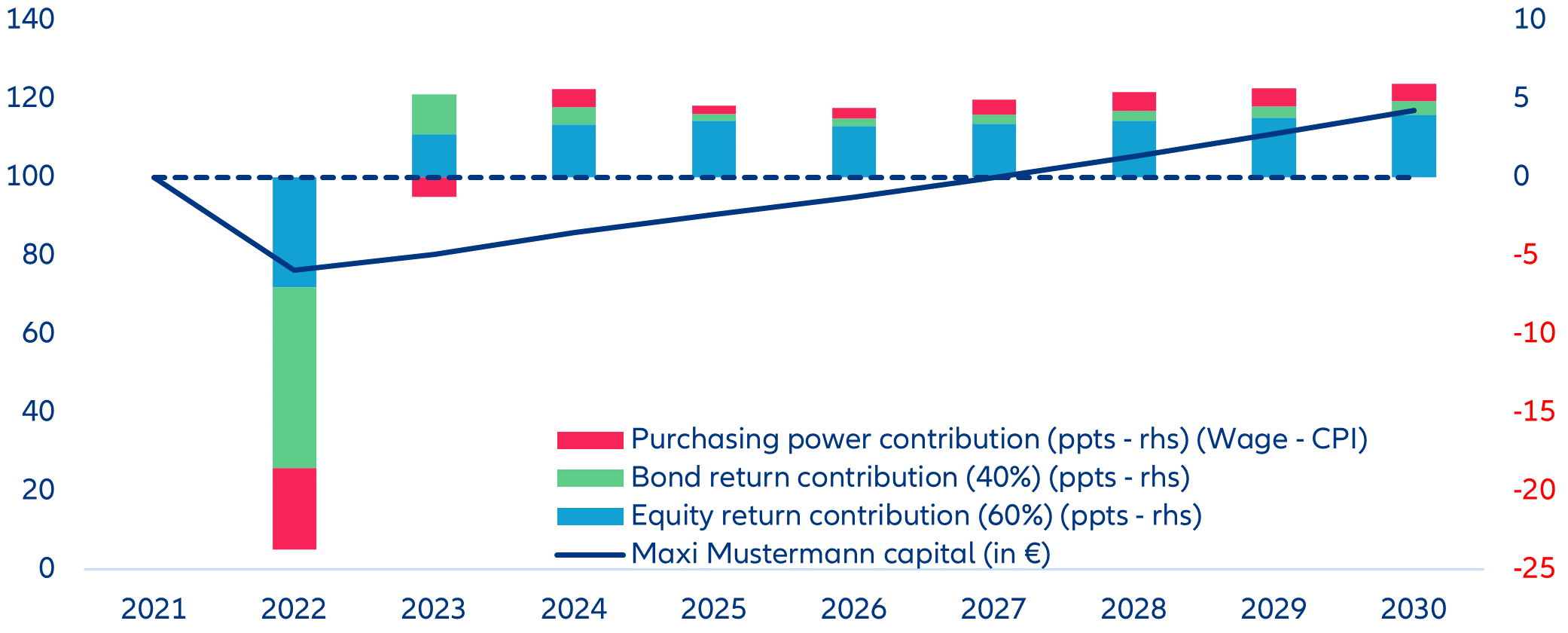

Making up for inflation—how Jane and Maxi can get their groove back

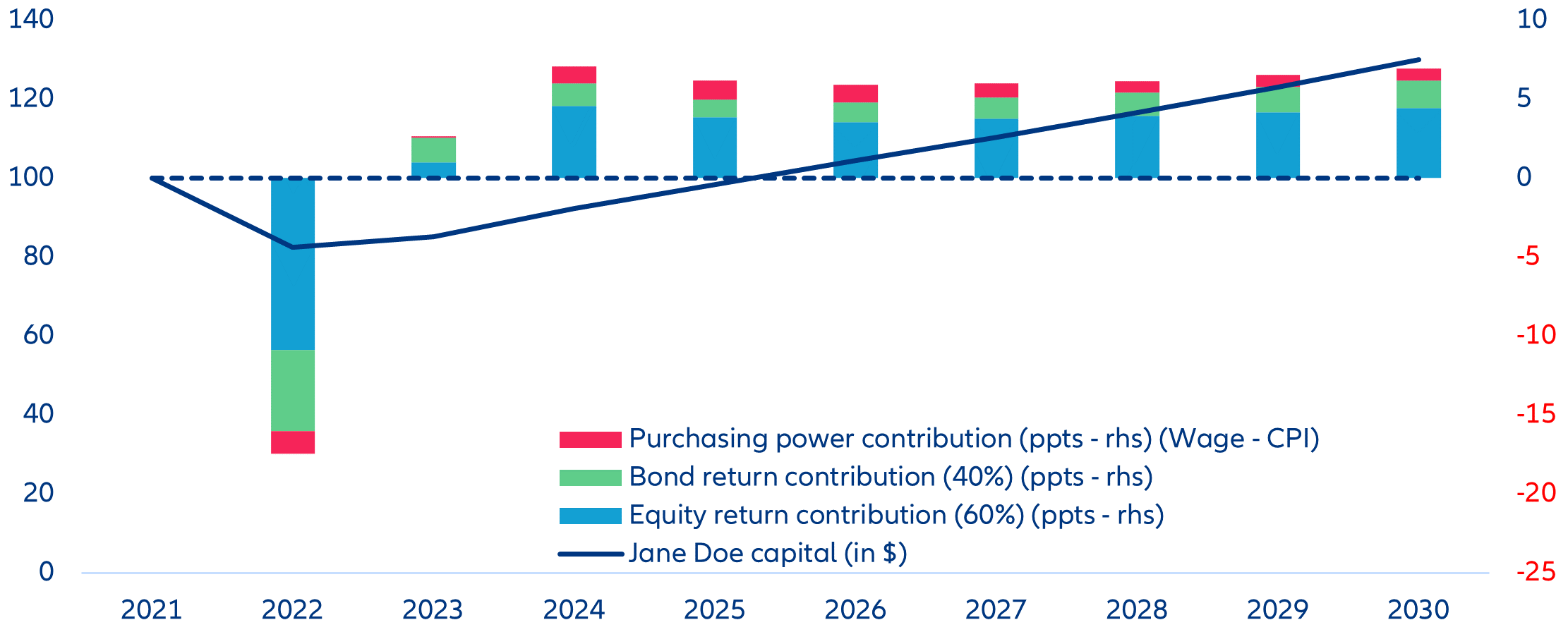

Investors holding a 60/40 portfolio of equities/bonds lost about ~20% on average last year; it will take them more than 3 years to fully recover their losses. In recent years, and especially since Covid-19, retail investors have become more engaged in capital markets. As fascinating as it has been to observe the erratic behavior of “meme” stocks and cryptocurrencies, 2022 ended with a market implosion, leaving new retail investors exposed to sizeable losses. So how long will it take for average investors to recoup their losses? To find out, we recreate a probable path for an average 60/40 portfolio of equities/bonds for both US and Eurozone investors: Jane Doe and Maxi Müller, respectively. In this hypothetical scenario, we assume a USD/EUR100 investment in the local stock market and local government bonds at the end of 2021, adjusting for the loss of purchasing power due to the high inflation regime. Our results suggest that 2022 left US investors with an average loss of -17 % while their European peers suffered an even greater blow of -24%. Based on our current macroeconomic and capital market forecasts [1], it would take up to four years for investors to make their money back (assuming no changes to the portfolio structure intact), Figures 8 and 9).

[1] See Allianz Research quarterly economic and capital markets publication (link)

Figure 8. Jane’s portfolio (in USD and yearly %)

Sources: Refinitiv, Allianz Research

Figure 9. Maxi’s portfolio (in EUR and yearly %)

Sources: Refinitiv, Allianz Research

As more retail investors participate in capital markets, it is increasingly important to provide the right tools to boost financial and risk literacy. Tech advancements for trading, excess savings during the pandemic and yield-seeking at a time of low interest rates and rising inflation are all driving more investors into capital markets. But in our 2020 [1]survey, we found that only 32.4% of Americans and 42.2% of Germans had basic financial literacy competencies. Financial skills can aid households to make the best of their financial decisions – from budgeting to saving and investments. Equipped with the necessary tools, households will be able to weather economic storms, or cushion the blows that our brave new world may throw their way.

[1] Financial and Risk literacy: Resilience in Times of Covid-19.

Corporate performance—will inflation continue muting spending in 2023?

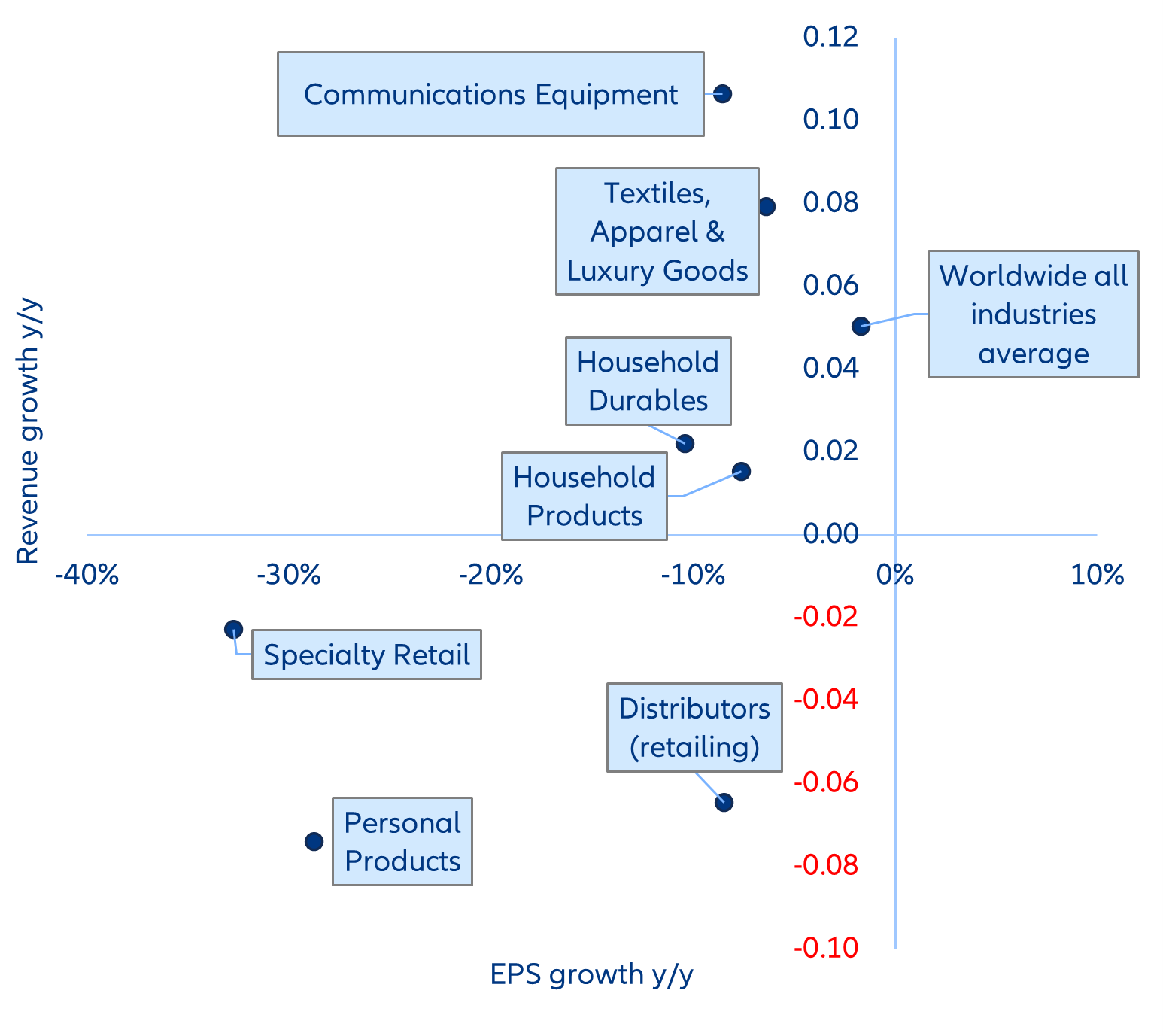

With a quarter of all listed companies having posted their Q4 2022 financial results, discretionary sectors appear to be the worst hit. Although it is still early to draw firm conclusions, it is fair to say that inflation has clearly hit household consumption over the past few months and therefore impacted the earnings of firms in the discretionary sector. Despite the discounts offered by distribution stores, aiming to reduce the inventories glut, retail sales fell by -1.1% in the US in December, and -2.7% in the Eurozone. Margin pressure has been particularly high for apparel retailers and department stores due to their higher bills for textiles, energy and transportation. While the overall industry EPS growth rate was -1.6% on average in Q4, the EPS of distributors and specialty retail companies fell by -8.5% and -32.7%, respectively. As per 2023 guidance, big players in the sector have cut their profit forecasts for the year, hoping for improving sentiments within a few quarters (Figure 10).

Figure 10. Q4 2022 revenue and EPS growth rates

Sources: Refinitiv Eikon (as of 07/Feb/2023), Allianz Research

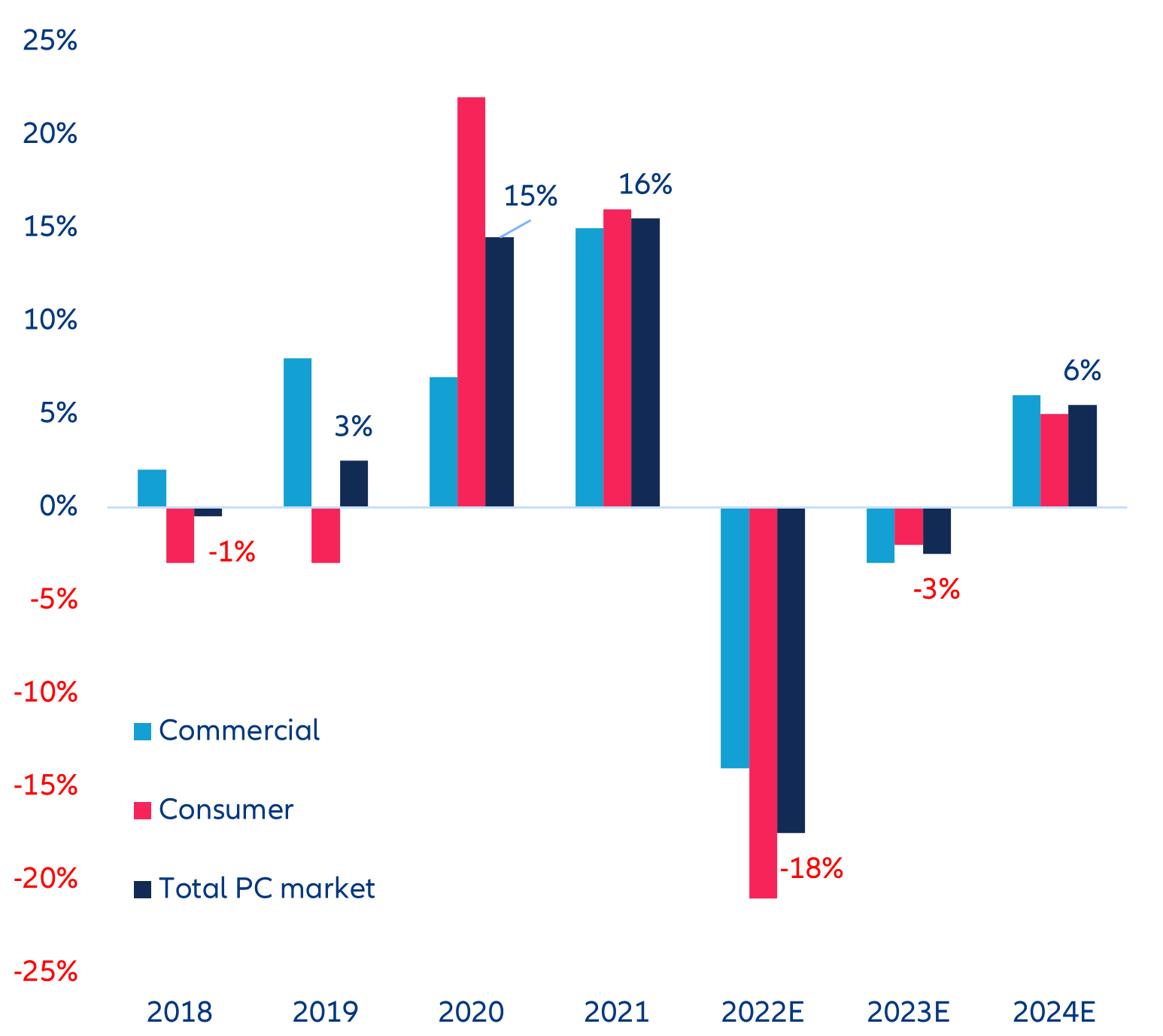

Consumer electronics is also feeling the pinch. After two years of a lockdown-linked sales boom (PC units sold globally climbed +14% in 2020 and +15% in 2021), sales of PCs and tablets fell by -17% and -3.3%, respectively, in 2022 (preliminary data). Consumers who bought new PCs during the pandemic still do not need to renew their current models, and companies are now more cautious with their budgets, given the macroeconomic headwinds. Although big players have announced that they expect pressures to ease in the second half of the year, 2023 is set to be another weak year for hardware sellers. This has been echoed by chipmakers that have been suffering from elevated inventory levels due to waning demand from the tech sector. As a result, they have been shifting their production into other fast-growing segments such as automotive (Figure 11). Global smartphone shipments hit 1.28bn units in 2022 (-11% y/y), the lowest level since 2013. Smartphone sales in China dropped by -13% y/y in 2022 to 286mn shipments (vs. 329mn in 2021), the first time in a decade that sales fell below 300mn, as strict Covid-19 restrictions further curbed demand. Though the worst might be over, global smartphone shipments are expected to decline -4.1% y/y this year to 1.23bn units.

Figure 11: Annual PC shipments growth worldwide

Sources: IDC, Bloomberg, Allianz Research

In Europe, despite the sizable excess savings that remain, we do not expect a consumption boost this year, given the uneven distribution among households. We estimate that the bulk of excess savings are in the pockets of higher income households (Figure 10). For instance, in the UK, we find that the 20% of households with the highest income hold GBP250bn of excess savings compared to a meagre GBP1.5bn for the households with the lowest incomes. The average high-income household has excess savings ranging from EUR13,650 in Germany to GBP41,600 in the UK. At the opposite end of the spectrum, the bottom 20% of households have essentially no more excess savings left.

In focus—monetary policy in Central and Eastern Europe ahead of the curve?

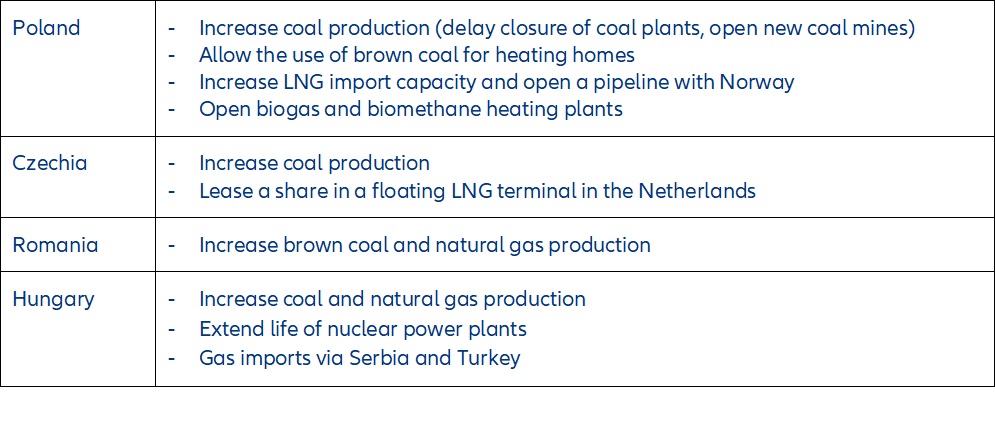

As in the rest of the EU, the energy crisis in Central and Eastern Europe (CEE) has tapered in recent weeks, and lower-than-expected energy prices pose less headwinds to economic growth. The EU’s gas-storage capacity was over 70% full in early February, well above the average 45% usually seen around this time of the year. As a result, the threat of gas rationing this winter has now largely vanished. Natural gas prices have dropped to levels last seen before the war in Ukraine began. A lot of this is due to luck: a comparatively mild winter (so far) has reduced heating demand. But the policy response in CEE was also crucial, especially efforts to reduce energy consumption and improve energy efficiency, as well as shoring up alternative energy supplies and sources to substitute gas imports from Russia (see Figure 12 for the measures taken in the CEE-4, the four largest CEE economies).

Figure 12: Policy measures introduced in the CEE-4 to substitute for natural gas imports from Russia

Sources: National governments, Capital Economics, Allianz Research

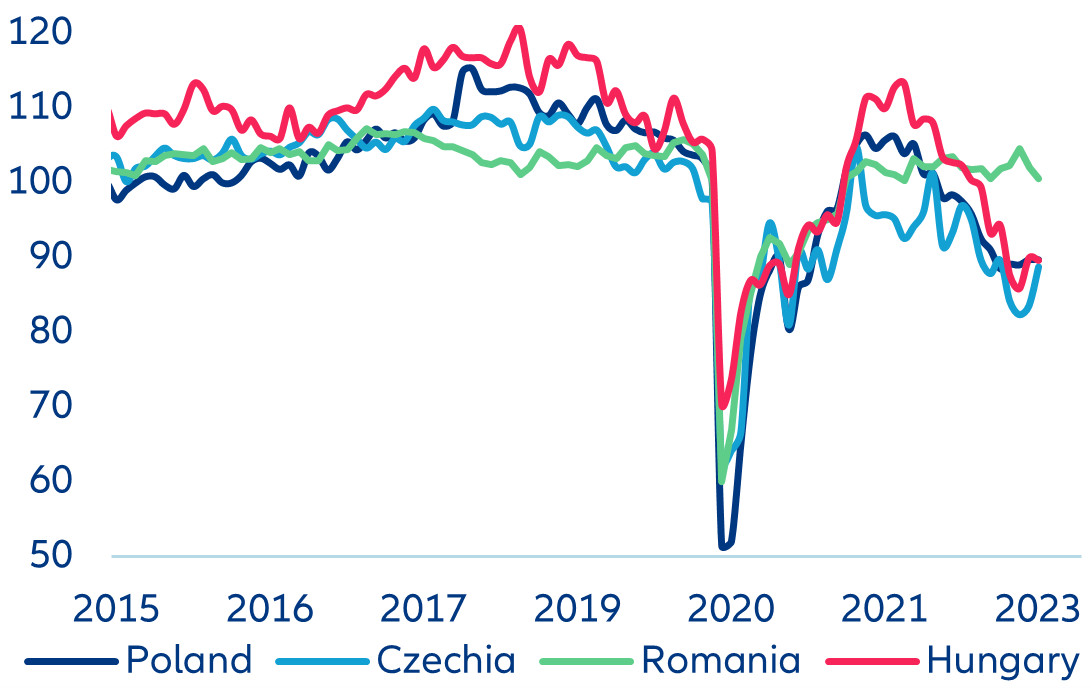

That said, the growth outlook in the CEE-4 for 2023 remains subdued. The impact of continued high inflation, increased interest rates (the lagged impact of aggressive monetary tightening in 2022), weaker external demand and deteriorated business confidence (Figure 13) will take full effect this year. Data released last week confirm that the Czech economy slipped into recession in the second half of 2022, and we expect another decline in output this quarter. We assume that Hungary was also already in recession in H2 as GDP contracted in Q3 and the substantial withdrawal of government support (including abandoning a cap on petrol and diesel prices) in recent months, owing to lack of fiscal capacity, is likely to have triggered a painful adjustment over the following quarters. Poland’s release of full-year 2022 GDP figures suggests that its economy likely contracted in Q4 as well. In Romania, industrial production has been in recession since the second half of 2022, but strong retail trade has so far prevented the overall economy from slipping into recession. We forecast full-year 2023 GDP growth to come in more or less flat in Czechia, around +0.7% in Hungary and Poland and +1.3% in Romania.

Figure 13: Economic Sentiment Indicator

Sources: European Commission, Allianz Research

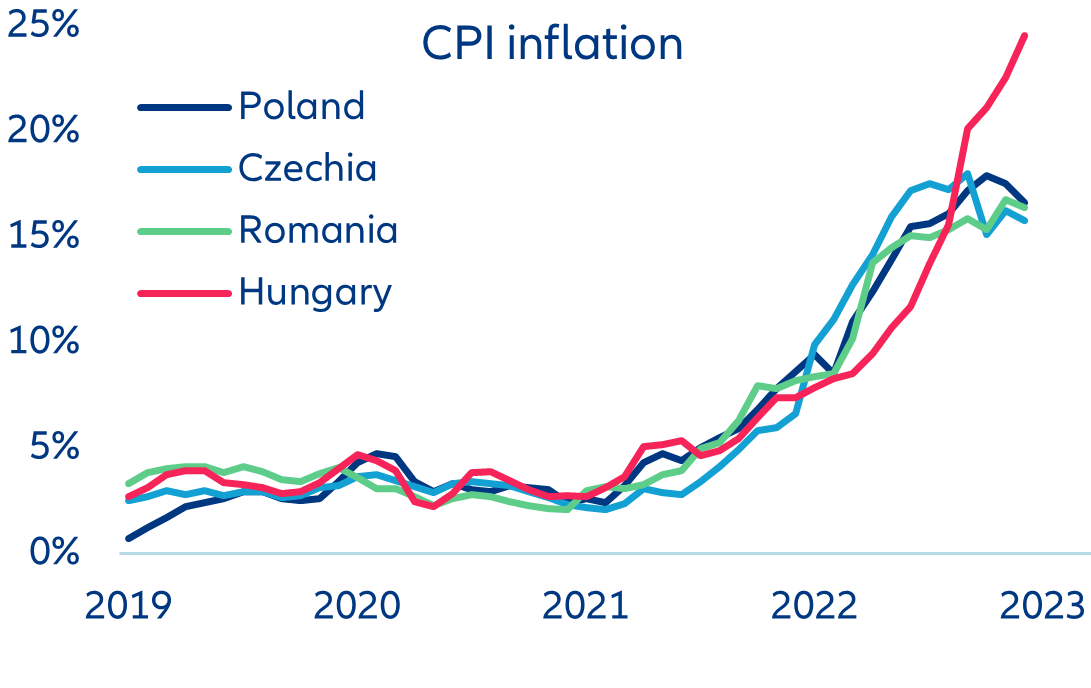

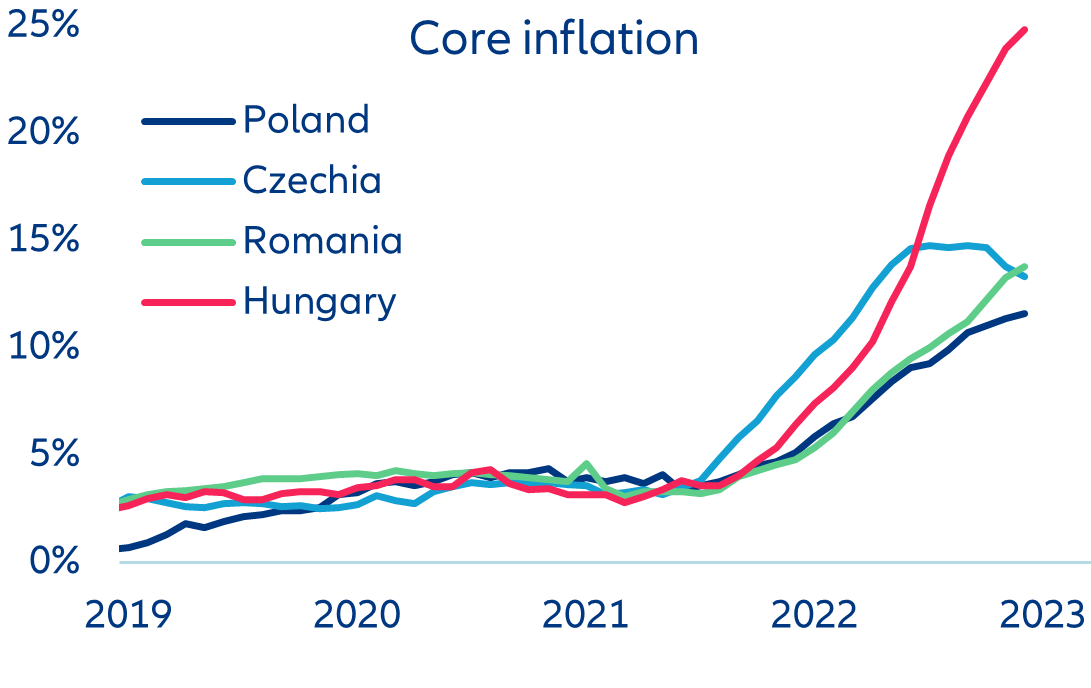

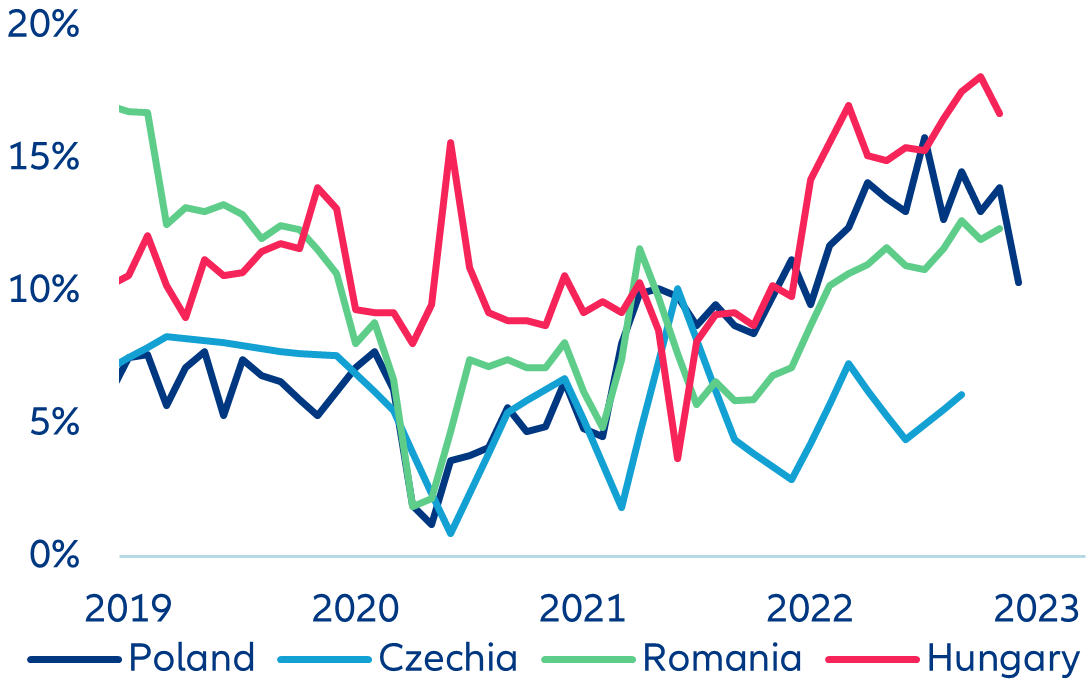

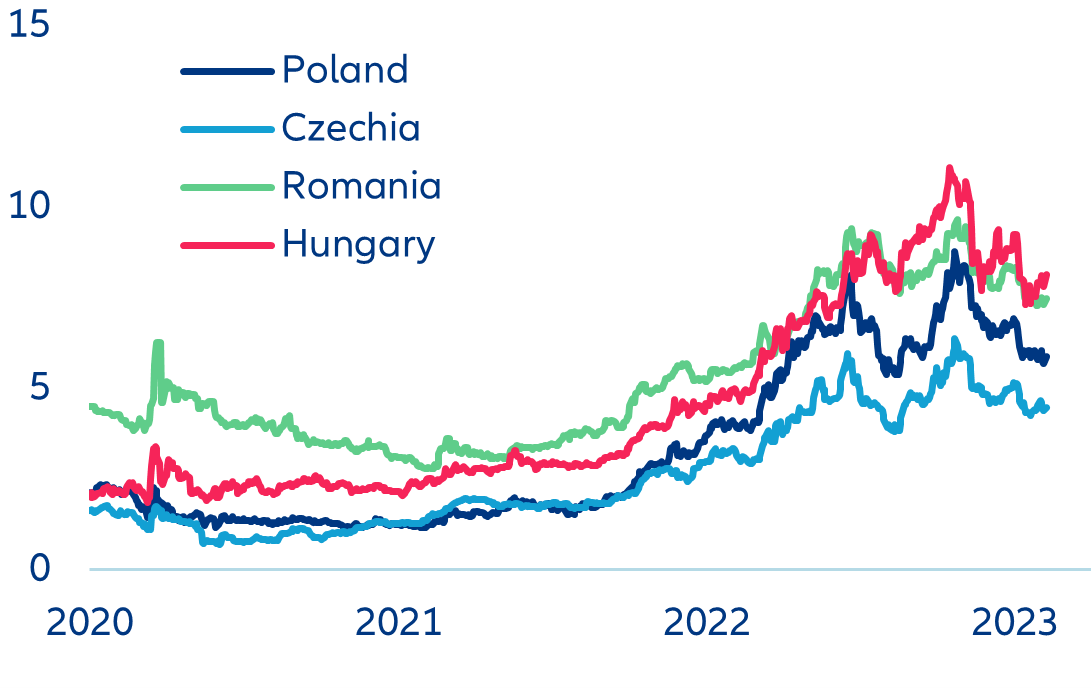

Inflation has peaked in most CEE economies and could decline more quickly than had been expected this year. However, price increases will remain elevated and above targets in the next two years. For the CEE-4, Figure 14 (left panel) suggests that consumer price inflation has passed a cyclical peak in Czechia (18% y/y in September 2022), Poland (17.9% in October) and Romania (16.8% in November). The much-stronger-than-expected drop in natural gas prices since December should ensure that the disinflation trend continues, even though changes in energy-support measures in 2023 may cause temporary (small) increases in inflation in January or February in some countries. However, inflation is likely to remain sticky in 2023 because it was not driven solely by surging energy prices in 2021-2022 but also by rising food prices and higher core inflation. The latter has so far only peaked in Czechia (see Figure 14, right panel) which has seen much lower wage growth in 2022 than its peers (Figure 15). Hungary is an outlier among the CEE-4 in this context. Inflation was initially lower there than elsewhere, thanks to considerable government support. However, it has soared since September 2022 and reached nearly 25% y/y in December (for both consumer price and core inflation) after the government scrapped support amid rapidly widening fiscal and current account deficits. Other major inflation drivers in Hungary have been nominal wage growth (the highest in the region at 16% in 2022, see Figure 15) and currency depreciation. Going forward, we forecast headline inflation to fall faster in Czechia, towards approximately 5% at end-2023 (averaging around 9.5%), followed by Romania (end-year 6.5%, average 10.5%), Poland (end-year 7.5%, average 11.5%) and Hungary (end-year 9%, average 15.5%). Without any new shocks, disinflation should continue in 2024 but we project inflation to fall back to the central bank’s target range only in Czechia (2% ± 1pp) by the end of 2024.

Figure 14: Consumer price (above) and core (below) inflation in the CEE-4

Sources: Refinitiv, Allianz Research

Figure 15: Nominal wage growth

Sources: Refinitiv, Allianz Research

Central banks in the CEE-4 have been the first major ones to halt their interest rate hiking cycles and we expect some of them to also be ahead of the curve when it comes to the pivot. The Czech National Bank (CNB) was the first major emerging market central bank to end its tightening cycle (after a last hike in June 2022), followed by the National Bank of Poland (NBP) in September and Hungary’s central bank (MNB) in October. The National Bank of Romania (NBR) was initially a laggard in monetary tightening and thus has continued hiking until January 2023. That was perhaps the end of its hiking cycle though there is a chance it will opt for one more rate increase on 9 February. The central banks in the CEE-4 have recently been very cautious in their monetary policy communication, avoiding any talk about potential rate cuts later in 2023. But this may reflect the fact that policy communication mistakes by the MNB and the NBP about the ending of the tightening cycles caused some market turbulences (rapidly rising bond yields; see Figure 16) in September-October 2022; the MNB even had to tighten one more time then. Central banks will want to avoid a repeat of that turmoil.

Nonetheless, barring any new shocks, we expect that the central banks in the CEE-4 will begin monetary easing in 2023, given the somewhat improved disinflation outlook and ongoing headwinds to economic growth in the region. The CNB is likely to be one of the first EM central banks to cut interest rates this year, most likely in June when annual inflation in Czechia is forecast to have fallen back to single digits. The recent appreciation of the Czech koruna (Figure 17) may also support an early rate hike as the CNB wants to avoid the koruna being too strong and jeopardizing the economy’s competitiveness. Further rate cuts by the CNB are projected in H2, bringing the Czech policy rate to 6.00% at end-2023 (from currently 7.00%). In Poland, we expect a first lowering of the policy rate around September, when inflation should have declined to below 10% as well, followed by another cut at the end of this year, taking the NBP’s policy rate to 6.25% (from currently 6.75%). The central banks of Romania and Hungary are likely to wait until Q4 2023 for the pivot to monetary easing. Both countries are forecast to experience large double deficits on the fiscal and current accounts and government bond yields are higher than that of Czechia and Poland, requiring more caution by policymakers. We forecast end-2023 policy rates of 6.75% in Romania and 12.00% in Hungary (currently 7.00% and 13.00%, respectively). See Figure 18 for an overview of our policy rate forecasts for the CEE-4 in 2023. These forecasts also suggest that we expect all CEE-4 central banks to pivot ahead of the ECB, and the CNB and the NBP to pivot ahead of the Fed.

Figure 16: 10-year government bond yields (%)

Sources: Refinitiv, Allianz Research