- With the cash cushion that was built during the pandemic losing its fluff, it is a good time to revisit consumption behavior, which is starting to lose steam in Europe and the US. The wealth effect is a behavioral economic theory that suggests that asset-price fluctuations affect household spending. However, we find that the income effect overshadows the wealth effect in France, Germany, Spain and the US. The marginal propensity to consume (MPC) per 1% difference in disposable income is 0.21% for France, 0.71% for Germany, 0.78% for Spain and 0.35% for the US. This highlights the importance of supporting household income as a tailwind to attain the much-desired economic soft landing.

- However, the wealth effect of housing prices clearly dominates that of stock market prices almost by a factor of ten in France, Germany, Italy, Spain and the US. For continental Europe, keeping inflation at bay holds the answer to consumption, while in the US the prospect of diminishing wealth weighs on the Fed’s hopes for a stormy soft landing.

FEATURE - OVERVIEW:

Consumption: what’s wealth got to do with it?

KEY DEVELOPMENTS

US GDP data, gasoline price pressures, high-yield corporate spreads ignore recession bells

- US GDP data came out stronger than expected, but underlying cracks appear—Household and government spending surprised on the upside but we still expect a recession in Q1 2023 in line with recent hard and soft data. This deteriorating momentum should comfort the Fed in slowing the pace of rate hikes during the FOMC meeting next week.

- No relief in sight for gasoline prices—As the European embargo on Russian diesel is about to begin, refiners' margins are also increasing and pointing towards expensive fuel for longer.

- High yield – High-yield investors have missed the recession memo and are already pricing in the recovery phase.

US economy ends 2022 on a strong footing, but more and more cracks appear under the surface

US GDP overshot expectations in Q4 2022, growing +2.9% q/q annualized (after +3.2% in the previous quarter). This is more than twice the pace we expected in our December 2022 scenario. Household consumer expenditure (+2.1%) and government consumption (+3.7%) both surprised on the upside. However, other components of expenditures were weak, notably residential investment (-19%), and business investment growth (+0.7%) slowed markedly from the previous quarter. Net trade and inventories provided large boosts to GDP growth, with the fall in imports outstripping the fall in exports.

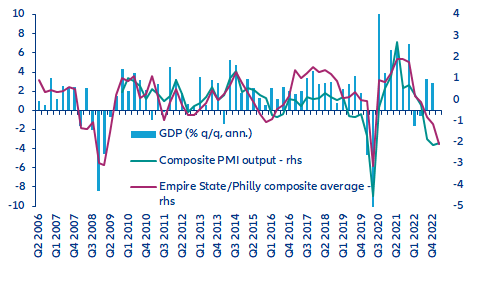

Soft data point to a recession beginning in Q1 2023, with hard data catching up fast. Business surveys released in January suggest the economy is currently entering a recession (see Figure 1), consistent with our forecasts. However, the surveys are probably overestimating the depth of the downturn as business sentiment tends to deteriorate excessively when gloomy talk of recession increase. Meanwhile, hard data released for December 2022 show that economic momentum was rapidly fading, with both retail sales and industrial production showing outright declines. We expect GDP to contract -0.8% (annualized) in Q1 2023.

Figure 1: GDP q/q growth (annualized) and business surveys (standardized)

Sources: Refinitiv, Allianz Research

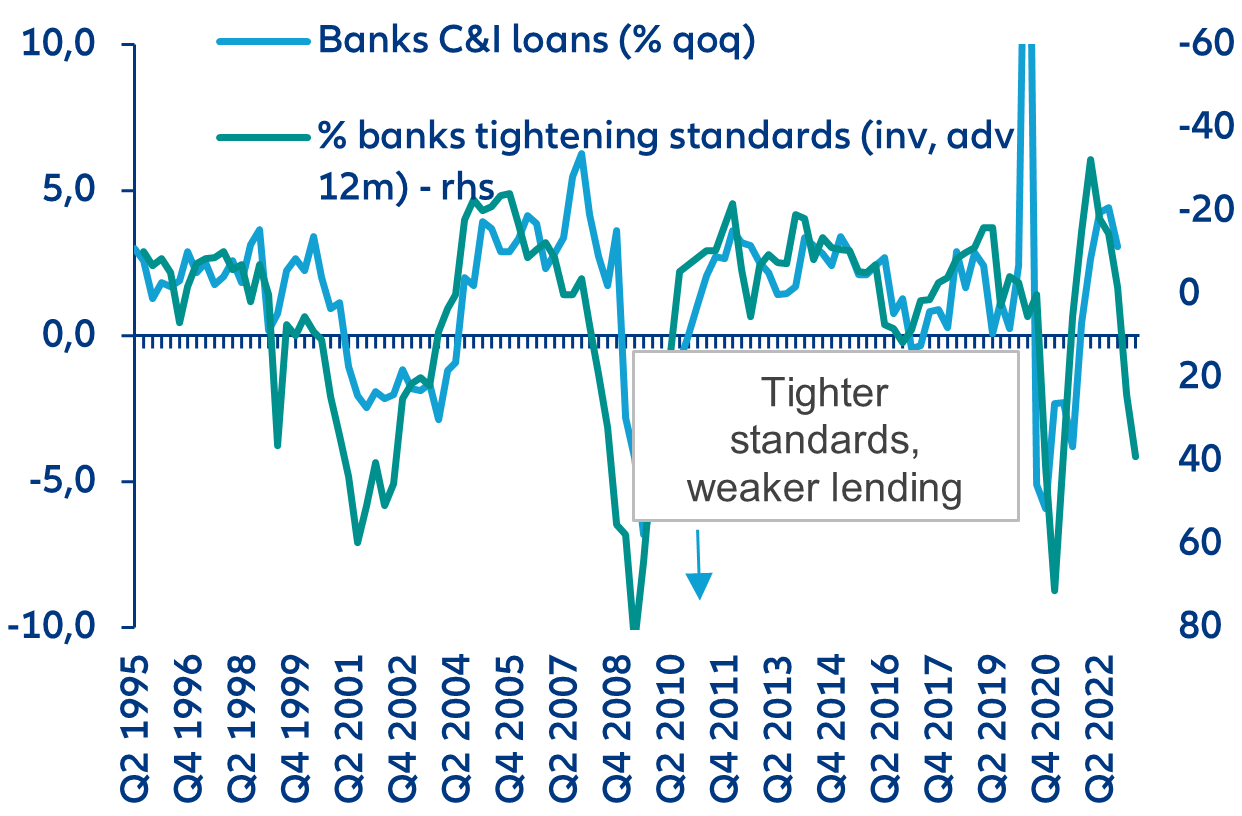

We see GDP falling through Q3 2023, with a peak-to-trough loss of around -1%. The monetary-policy-induced tightening of credit conditions is rapid. The proportion of banks tightening credit standards for commercial and industrial loans is at level only seen during previous recessions (2001, 2008-09 and 2020), according to the Fed’s Senior Loan Officer Opinion Survey (see Figure 2). Business investment is set to decline in the next few months, as hinted by outright drops in capital-expenditure intentions. On the household side, pandemic-related excess savings are being depleted at a fast clip while still-declining real wages depress income. Property prices have started to come down on a sequential month-to-month basis and given our expectation of a 10-15% peak-to-trough decline, negative wealth effects will be powerful in dragging down consumption expenditures in the coming months, as highlighted in our feature below.

Figure 2: Banks’ credit standards & C&I loans

Sources: Refinitiv, Allianz Research

We now expect the bipartisan deal to agree on a modest net fiscal tightening (against our previous expectation of a modest net easing), amid more political divisions within the Republican party. Conservatives fiercely oppose government spending increases, so it would require at least some spending cuts agreed upon with the Democrats to get them to sign the deal. Fiscal tightening reinforces our call that the US economy will muddle through a recession this year, albeit a moderate one (we expect a -0.3% GDP drop).

Oil prices may have decreased, but there is no relief in sight for the consumer

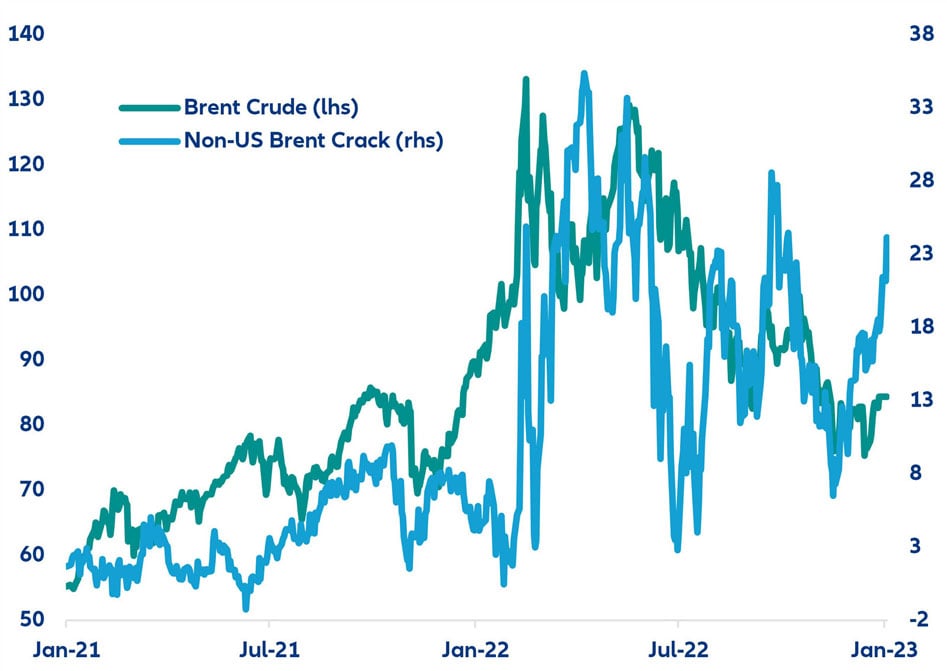

The embargo on Russian diesel and increasing refiners’ margins suggest gasoline prices will remain elevated. Oil prices are currently well below their 2022 peaks – Brent prices are around 84 USD/bbl versus close to 130 USD/bbl in early June 2022. We still expect oil prices to average 95 USD/bbl this year on the back of higher Chinese demand, stock replenishing (strategic reserves are at decade-low levels in the US and in Europe) and tight supply from OPEC+ members. While OPEC+ is due to meet virtually next week, we do not expect any increase in target output. Beyond crude oil, from 01 February, European countries will stop importing Russian diesel. As fuel supply remains an issue for the region, this means potentially more expensive fuels for longer. Furthermore, refiners’ margins for both the US and the rest of the world are picking up (Figure 3), meaning that demand remains steady while refiners’ capacities remain stretched. All in all, consumers should not see major declines in fuel prices over the next few months.

Figure 3: Brent prices and refiners margins (USD/barrel)

Sources: Refinitiv, Allianz Research

Some asset classes continue to ignore the recession memo

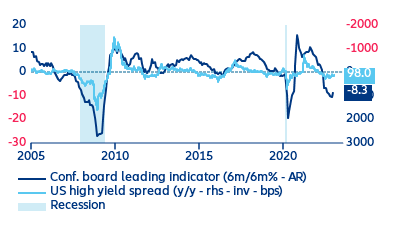

High-yield markets are already over the upcoming recession, being already positioned for the subsequent recovery phase. With economic leading indicators continuing to point towards a recessionary environment, especially in the US, it is hard to reconcile the current high yield market positioning with the rather pessimistic economic and fundamental news-flow. Taking the US Conference Board leading indicator, a good recession predictor, as a reference, the continuous decline suggests that high-yield spreads should be much wider. However, and inconsistent with underlying economics, the spread widening has not only been muted but has also mostly reverted since the beginning of the year. Similarly, the spread between high-yield credit spreads and investment grade has been narrowing, indicating that the market perception of credit risk may be far too optimistic. Such a pattern tends to be consistent with a post-recession recovery environment rather than a recessionary environment, thus indicating that high-yield markets may be far too complacent and bullishly positioned (Figure 4).

Figure 4: US economic leading indicator and HY corporate spreads

Sources: Refinitiv Datastream, Allianz Research

Taking this into account, and acknowledging that our baseline scenario comprises a non-negligible increase in insolvencies and a deterioration in companies’ balance sheets as a direct consequence of our recession call for 2023, we view the current positioning as unsustainable. We would expect risky assets to underperform in the near term, reverting the bull run seen since the beginning of the year. Specifically for high yield, we expect a short-term spread widening in the order of +50bps to +75bps to levels close to 500bps (vs current levels of 450bps for EUR HY and 435bps for US HY).

With the cash cushion that was built during the pandemic losing its fluff, it is a good time to revisit consumption behavior, which is starting to lose steam in Europe’s largest economies (France, Germany, Italy, Spain) and the US. Changes in income are not the only driver of household consumption; in some markets, wealth impacts can play a role, with asset-price fluctuations affecting spending even if income does not change. In the US, for example, the Federal Reserve has for long included the wealth effect in its macroeconomic forecasting. As shown in the scatterplot below, as wealth increases, the savings rate tends to decrease – and vice versa. In this context, could recent fluctuations in financial asset prices and the potential fall in housing prices drag down consumption even further? To find out what is on the cards for consumers, we look at the relationship between household assets, income and savings.

Figure 5: Household financial assets to personal disposable income ratio and savings rate in Europe and the US (period 2000-2021)

Sources: Allianz Global Wealth Report 2022, Refinitiv Datastream

Fluctuations in asset prices – real or financial – rarely come without any other macroeconomic developments. To measure both the income and wealth effects on consumption, we drew from Caceres (2019) and his macro estimations to measure both impacts in France, Germany, Italy, Spain and the US. Generally, we find that the income effect overshadows the wealth effect in all countries and it is statistically significant, as expected. The marginal propensity to consume (MPC) per 1% difference in disposable income is 0.21% for France, 0.71% for Germany, 0.78% for Spain and 0.35% for the US. These income effects highlight the importance of supporting household income as tailwinds to attain the much-desired soft landing.

Another feature that is common for most countries is that the wealth effect of housing prices clearly dominates that of stock market prices almost by a factor of ten in France, Germany, Italy, Spain and the US, as shown in the table below. This is in line with expectations as stock market prices are more volatile than real estate prices. Looking at home sales turnover or the structure of savings might hold some of the answers for further analysis. For Germany, we find that the wealth effects materialize with a lag of two years, while for the US and France there is both a lagged and instantaneous effect.

Table 1: Marginal propensity to consume (MPC) results for short-run wealth effects, in %

Sources: Allianz Research

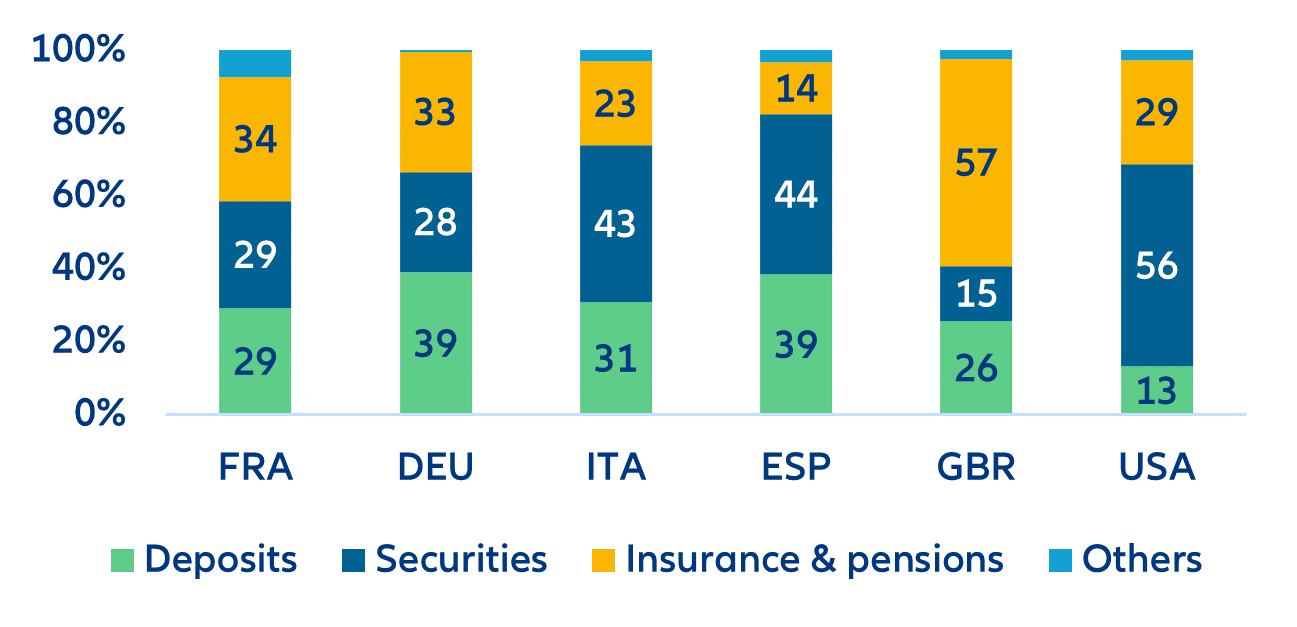

Differences in household portfolio structures also have an impact on how they react to fluctuations in asset prices, which might explain the unconventional reaction to house prices in Germany, for example, where only 44% of households are homeowners as compared to France’s 58%. US households have a larger share of their wealth in securities (bonds, stocks, mutual funds etc.). However, the experience of the subprime mortgage crisis might make households more susceptible to fluctuations in real estate prices (see Figure 6 below).

Figure 6: Household financial asset portfolio structure

Sources: Allianz Global Wealth Report 2022, Refinitiv Datastream

Using our macroeconomic expectations and forecasts for asset prices, while drawing from the income and wealth effects described above, we estimate real consumption growth in 2023 and 2024. For continental Europe, we are mostly looking at flat consumption growth in line with the region’s economic slowdown. Because disposable income has the stronger effect, it appears that the inflation genie holds the answer as households are impacted by high prices and the economic effects of the war in Ukraine. For the US, as we expect inflation to come down sooner, despite the strong labor market, consumption might lose steam and park for the next two years at the stagnation station because of the impact of asset prices on households’ internalized net worth function.

Methodology appendix

We ran vector autoregressive models for each of the countries that can be algebraically shown as Δ𝑿𝑡 = 𝑩0 + ∑ 𝑩𝑖 Δ𝑿𝑡−𝑖 𝐿 𝑖=1 + 𝝐𝑡 where 𝑿𝑡 is a vector containing series on real growth series of: consumption, the MSCI stock price indices, the house price indices and disposable income of each of the five countries from 1980 up until our scenario expectations of 2024.