Please note: Historical publication – forecasts reflect the outlook as of January 2023. In the event of discrepancies in calculations and figures, the most recently published value shall apply.

FEATURE - OVERVIEW:

Eurozone: quantitative tightening and sovereign debt servicing cost.

- The ECB will start quantitative tightening (QT) in March, but the balance sheet reduction is likely to be limited at the planned run-off rate of government bond holdings. While the stock effect is relatively small due to capped reinvestments of amortizing assets, the flow effect will significantly impact the term premium (due to the flat term structure), and, thus, raise sovereign borrowing costs. We estimate that the current run-off rate could raise the term premium of the 10-year German Bund by about 90 bps until end-2024.

- Government debt burdens have increased massively in 2022 after years of favourable financing costs and will increase further in 2023-24-despite some relief from lower rollover risk due to longer debt maturity profiles. We estimate that higher expected policy rates and term premia will increase the debt-servicing cost by 0.7% of GDP in Germany, 1.1% in France, 1.2% in Spain and 1.6% in Italy until 2030.

KEY DEVELOPMENTS

US debt ceiling, Elysée Treaty 60th Anniversary, outlook for Brazil, bankruptcies in the construction sector, and clouds over the capital market rally

- US debt ceiling—rising tensions until May, with last-minute compromise on modest fiscal tightening the most likely scenario

- Elysée Treaty 60th anniversary—recharging the Franco-German partnership to respond to the energy challenge and lead an imperiled Europe?

- Insolvency forecast - construction leading the global rebound

- Outlook for Brazil—ready for a roller-coaster ride?

- Capital markets—entering a challenging earnings season

US debt ceiling - raising tensions until May, with last-minute compromise on modest fiscal tightening the most likely scenario

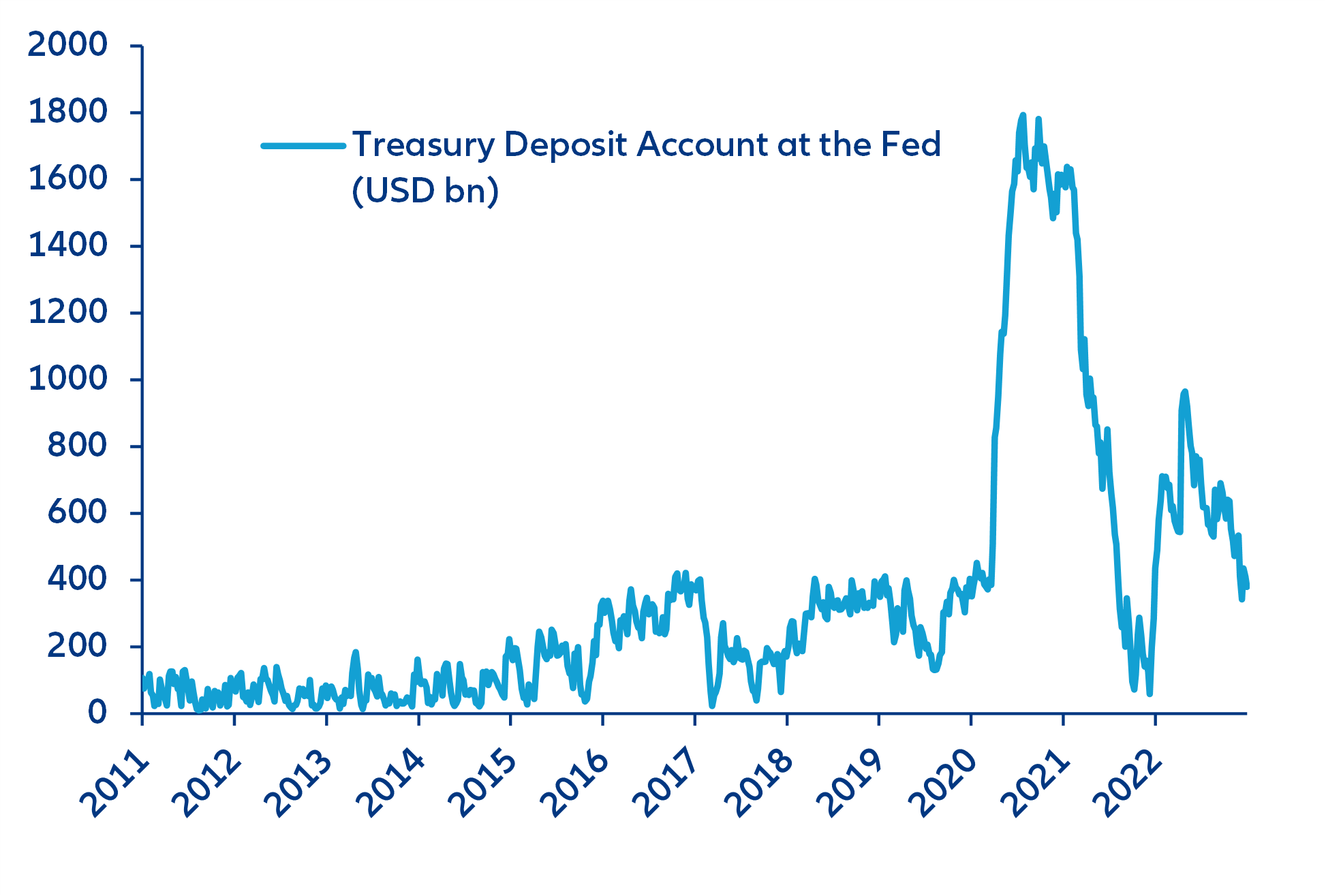

Concern about the US Administration breaching its debt ceiling is coming back to the fore yet again. According to Treasury Secretary Yellen, the Federal debt statutory limit – set at USD 31.4trn – has been hit this week. However, the government will not default on its debt in the near term since it still has ample cash buffers of USD380bn to draw upon at its account held at the Fed (Figure 1). Also canceling some earmarked investments and budget cuts to government entities seem likely. Political infighting in Congress between the Republicans and Democrats, but also among Republican members of Congress, means that a deal to lift or suspend the debt ceiling is unlikely in the next couple of months. Thus, we should brace for repeated bouts of political drama.

Figure 1: US Treasury deposit account at Federal Reserve (USD billion)

Sources: Refinitiv, Allianz Research

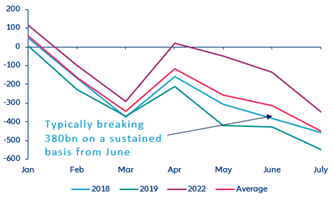

We maintain our view[1] that a deal will be eventually reached at the last minute in Q2, when the Treasury’s cash buffers are exhausted. According to past deficit patterns, funding the projected cumulated deficit should lead to a breach of the debt limit in June (Figure 2). However, our expectation that the US is already slipping into a recession means that we expect a higher deficit than usual. Failing to reach a compromise with the Democrats would be politically costly for the Republicans, not least because they could be blamed for triggering a government shutdown or, worse a sovereign default, at a time when we expect the US economy to reach the trough of a shallow recession. Nevertheless, ahead of the expected debt-ceiling compromise, interest rates on Treasury securities maturing during the summer could rise sharply.

[1] US midterms: Republicans are back, (fiscal) policy impasses too (allianz.com)

Figure 2: US Federal government deficits (cumulative, USD bn)

Sources: Refinitiv, Allianz Research

We now expect the bipartisan deal to agree on a modest net fiscal tightening (against our previous expectation of a modest net easing), amid more political divisions within the Republican party. Conservatives fiercely oppose government spending increases, so it would require at least some spending cuts agreed upon with the Democrats to get them to sign the deal. Fiscal tightening reinforces our call that the US economy will muddle through a recession this year, albeit a moderate one (we expect a -0.3% GDP drop).

Elysée Treaty 60th anniversary—recharging the Franco-German partnership to respond to the energy challenge and lead an imperiled Europe?

On Sunday, France and Germany will celebrate the 60th anniversary of the Elysée Treaty, which aims to strengthen the cooperation between the two nations after centuries of rivalry and conflict. However, the anniversary gives little reason to celebrate. Recent months have been marked by rising political tensions between the EU’s largest economies, which culminated in the cancellation of a Franco-German Council of Ministers in late October. Yet, with war raging just a few hundred miles away from Berlin, the very genesis of the Treaty has become an obligation for both countries to reaffirm their shared values in shaping Europe’s response to its multiple crises.

On the occasion of the anniversary, both countries have pledged to set out a common roadmap, which could provide a common vision and strategy for both countries but also more broadly for Europe. Beyond PR and wishful thinking, observers will especially be looking for common positions on topics that were divisive in 2022, ranging from more integrated energy systems and closer security cooperation to common industrial and trade policy.

One area of focus is likely to be how both countries can from a unified response to the US Inflation Reduction Act, which has already been discussed at the recent Franco-German economic and financial council meeting. There is shared concern on both sides of the Rhine that US subsidies could draw European companies to the US, in particular by the IRA’s most important provisions, such as its incentives for electric vehicles and zero-carbon electricity, which are “uncapped” tax credits and could reach up to USD800bn according to recent estimates. After considering the amount of private investment federal spending tends to catalyze, the IRA could boost total climate spending to roughly USD1.7trn over the next 10 years (almost twice the size of the EU’s Green Deal, which was announced with great fanfare three years ago).

The EU’s immediate response to the IRA has focused on seeking exemptions from the discriminatory clauses. It has attempted to do so by using the threat of a counter-subsidy package, which is unlikely to be effective as leverage. The European Commission has been given a mandate to come up with a plan early this year, which seems to include a further relaxation to the Temporary State Aid framework to facilitate scaled-up government support to key industries and technologies.

Enhancing the EC’s central fiscal capacity would be another plank of the EU strategy at a time when tightening financing conditions will constrain fiscal space in supporting climate-smart public investment. In our recent research, we found that, except for Germany, the largest Eurozone economies are already struggling to stabilize elevated government debt levels. As we show in this week’s feature (see below), even if government debt ratios remained unchanged, a lasting interest-rate shock (reflecting the ECB’s current hiking cycle) would mean that interest expenses will amount to 2% GDP in these countries by 2030. To put these figures into perspective, this additional budget burden due to higher financing costs alone exceeds total public investment.

Insolvencies in construction leading the global rebound

Rising insolvencies since last year are now affecting also large companies.[1] According to our internal reporting, while business insolvencies massively concern SMEs, insolvencies of large firms, those with over EUR50mn of turnover, posted a noticeable rebound at the end of 2022 globally. In Q4 2022, the number of major insolvencies surged by +30 cases compared to the previous quarter, and +17 compared to Q4 2021, to reach 88 companies. This is a record high since Q4 2020 and slightly above the pre-pandemic average (74 over the period 2015-2019).

We expect larger insolvencies to remain broad-based but there are geographical (Europe) and sectoral (construction, retail) pockets of higher vulnerabilities. Globally, major firms benefit from larger cash buffers and higher pricing power, but the global context of slower macroeconomic growth, weaker financing conditions and specific issues (e.g. energy mix, supply-chain dependencies, FX, Covid-related policies) is increasing the risks for the earnings and cash flow of the most vulnerable ones, notably those most indebted or with a low-profit business model. In Q4 2022, all regions contributed to the rebound in major insolvencies, but Western Europe already stood out with the largest increase (+15 cases q/q to 46), ahead of Asia Pacific (+6 cases q/q to 22) and North America (+6 cases q/q to 11). The full-year outcome has almost the same ranking, with Western Europe registering more than half of the global count (138 cases out of 270) ahead of Asia (70), Central and Eastern Europe (32) and North America (27). China continues to post the highest number of top insolvencies, with nine out of the top 10 insolvencies in terms of turnover for 2022, including seven firms in the construction sector due to the real estate downturn. Globally, construction has already proved to be the most affected in 2022, with 64 major insolvencies (+17 cases compared to 2021), notably in Western Europe (30 cases) and Asia (24). In the last quarter, however, retail recorded the largest increase in major insolvencies, ahead of construction, metals (esp. in Western Europe) and services (esp. in the US).

[1] See our report Energy crisis, interest rates shock and untampered recession could trigger a wave of bankruptcies

President Lula’s new term is off to a rocky start. But it is not vandalism by Bolsonaro supporters that is shaking markets so much as worries over the ballooning fiscal deficit. With Brazil's debt-to-GDP ratio at 88%, compared to an average of 45% in other major countries of the region, the recently approved BRL145bn (1.6% of GDP) spending package (known as Transition PEC) is putting the country's fiscal credibility at risk.

The beginning of the new administration has created some alarming points for investors: The decision not to privatize Petrobras and the upcoming change in fuel-pricing policy; contradictory statements from ministers, pointing to a lack of policy coordination; the extension of the federal tax exemption on fuel and Lula's conspicuous lack of comment on fiscal reform and debt management. As a result, Brazilian assets have not fully benefited of the positive mood in global markets. The financial sector and some of the big companies especially vulnerable to more interventionist policies have been the most affected (notably Petrobras).

In response to market stress, the government switched to a more conciliatory tone, and Finance Minister Fernando Haddad has taken measures to reduce the fiscal deficit in 2023 (estimated at 1.9% of GDP for now). But Brazil still has a long way to go. The measures focus mainly on the short term, focusing on increasing revenues rather than cutting expenses. Moreover, there is no guarantee the estimated targets are going to be achieved. In this context, we do not expect public debt to stabilize: it could reach close to 100% of GDP by the end of President Lula's mandate.[1]

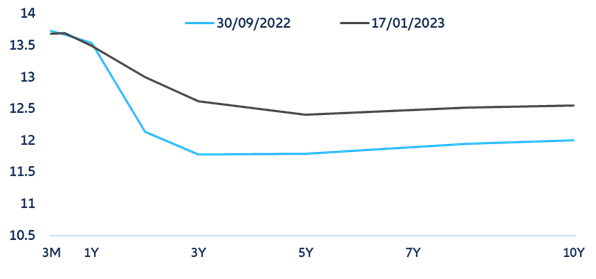

It is likely that the announcement was designed to give the government more time to work on a tax reform and a new spending cap rule, which could be announced in April, according to Minister Haddad, or no later than June). More structural measures like this will be fundamental to anchor expectations and leave room for the central bank (BCB) to reduce interest rates. A survey carried out by the BCB shows that markets have raised their inflation forecasts and foresee lower cuts for the Selic rate in 2023, clearly signaling markets' concern with a mismatch between monetary and fiscal policy. This has been observed as well in the movements experienced in the bond market where yields of medium and long-term maturities have move upwards since Q3 2022 (Figure 3), in dissonance with global sovereigns where the inversion has deepened, and the yields of long-term maturities have been stable or have fallen.

[1] See “Brazilian elections: The calm before the storm?” for further details.

Figure 3. Brazil-BRL sovereign yield curve (%)

Sources: Refinitiv, Allianz Research

As the government faces heavy pressure to ramp up spending, including an expensive readjustment to the minimum wage, we expect the volatility in Brazilian markets to continue until a credible fiscal plan is made. Although the turmoil generated by the protests has not had a strong impact on markets, the scrutiny of foreign investors will deepen and we could see a slowdown in new investments – Spanish companies, and in particular its financial sector, are the ones with the highest exposure to the country.

Capital markets: A peek into a challenging earnings season

Markets enter the earnings season in the wake of the 2023 “policy-pivot-fueled” bull run. With the earnings season just starting and showing a mixed bag of outcomes so far, markets continue to focus on macro-driven fundamentals rather than corporate fundamentals. As was the case in 2022, the inflation- and growth-driven changes in monetary-policy expectations continue to be in the driving seat of the broad market performance, responsible for the current 2023 bull run, and will continue to drive performance until a clear economic and policy path is defined (+5 to +10%ytd).

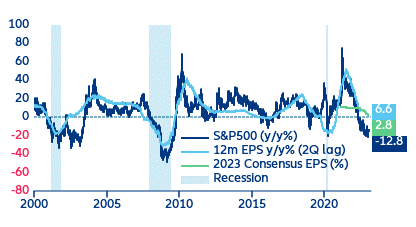

However, we should expect some market readjustments as analysts readjust to both reported earnings and earnings forward guidance. This will especially be the case since earnings expectations for 2023 remain high and inconsistent with the current market pricing. According to our own modeling and consistent with the current market pricing, we should expect earnings growth to trough at -3 to -5% in 2023, bringing the overall 2023 earnings growth close to 0% (Figure 4).

Figure 4: US earnings and earnings expectations vs equity performance

Sources: Refinitiv, Allianz Research

Despite a deteriorating outlook for corporate margins during the next months, we expect macro-fundamentals (i.e. monetary policy, inflation, growth, etc.) to continue driving market performance -for as long as the policy pivot is not hardwired into market pricing (i.e. until Q3 2023). Thus, we expect corporate fundamentals to start only driving market performance late in the year, leading to an overall 2% and 6% total return for the US and Eurozone, respectively.

FEATURE

Eurozone: quantitative tightening and sovereign debt servicing cost

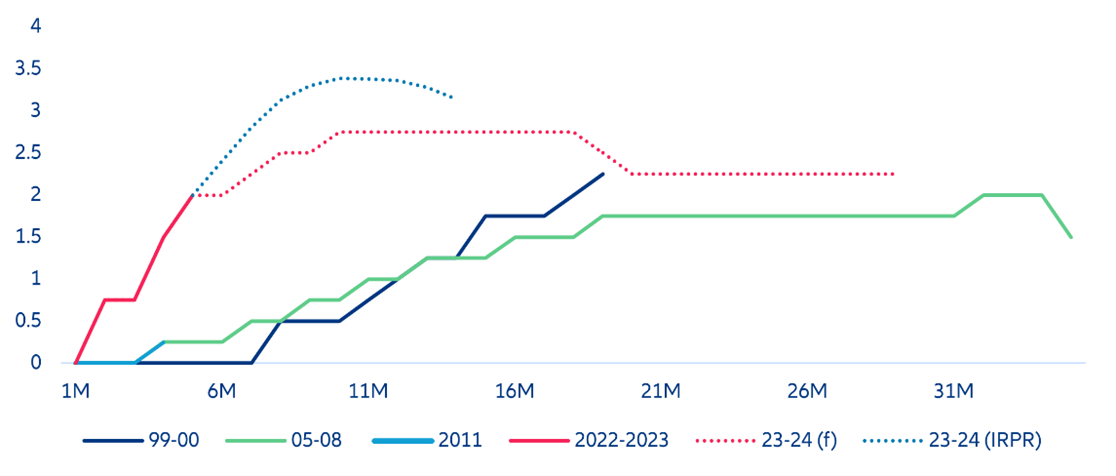

Strong inflation dynamics will require a hawkish ECB. Despite a sharp decline in food and energy prices in the Eurozone in December, which led headline inflation to decrease to 9.2% y/y (down from 10.1% during the previous month), inflation will remain uncomfortably high, averaging about 6% this year, with core remaining rather sticky until next year. Slowing growth and rising unemployment have helped mitigate wage-price pressures as supply-demand imbalances gradually subside. Thus, we expect the ECB to slow the pace of rate hikes to reach a terminal rate of 3.0% for the effective policy rate (deposit rate) until May 2023 and delay potential interest rate cuts to 2024 (Figure 5).

Figure 5. Eurozone—Current and past policy rate hiking cycles (%)

Sources: Refinitiv, Allianz Research

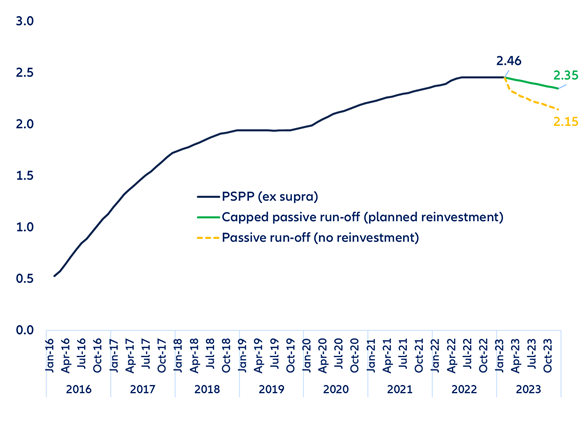

The restrictive monetary stance is bound to accelerate the tightening of financing conditions once the ECB starts reducing its balance sheet in March. One year after the US Federal Reserve, the ECB will commence a passive run-off based on scheduled redemptions by reducing its reinvestments of principal repayments of current asset holdings. Unwinding its asset purchases will focus on the “old” asset purchase program (PSPP) while asset purchases during the pandemic (PEPP) will remain untouched. The current amortization schedule of government debt securities held under the PSPP suggests a redemption volume of EUR246bn in 2023 (or EUR20bn/month), which would result in an average monthly run-off of about 0.9% of the starting balance of EUR2.5trn (without supranational debt) without reinvestment. Applying the planned reduction of reinvestments (currently set at EUR15bn/month for Q2) would halve the amortization rate, resulting in a (rather small) decline of government debt holdings by only EUR132bn in 2023—about 1.6% of the ECB’s current balance sheet of EUR8.5trn (Figure 6).

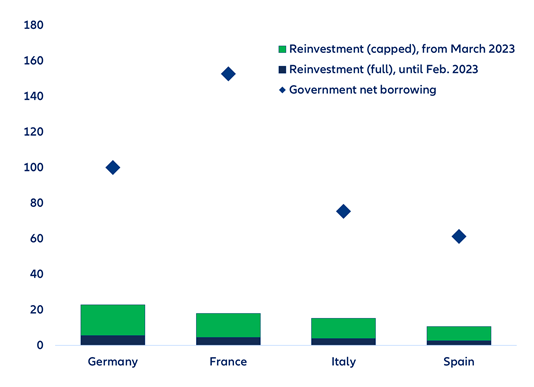

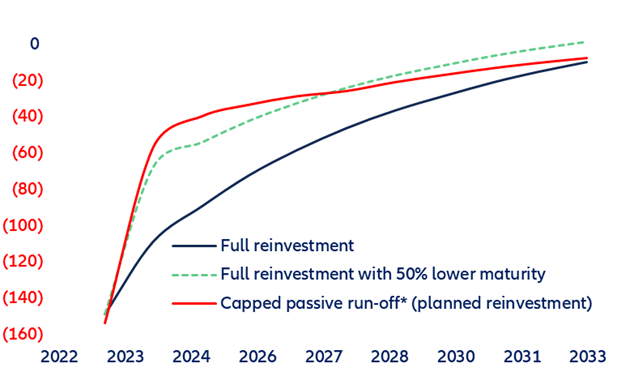

Despite a small reduction of the overall balance sheet (based on current plans), the flow effect of QT will significantly impact the term premium (due to the flat term structure) and, thus, raise sovereign borrowing costs. For the first time in more than five years, expected asset purchases under the capped run-off will no longer absorb the net financing requirements of Eurozone governments, with higher net supply of government debt likely to widen sovereign credit spreads (Figure 7). Eurosystem central banks will purchase only slightly more than EUR60bn of debt issued by the four largest economies (EUR23bn (Germany), EUR18bn (France), EUR16bn (Italy) and EUR11bn (Spain)), assuming consistency with the ECB’s capital key. Thus, we estimate that the current run-off rate could raise the term premium of the 10-year German Bund by about 90 bps until end-2024 (Figure 8).

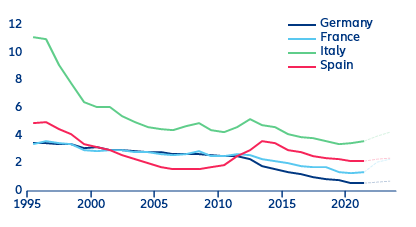

Even with higher overall debt levels, sovereign interest payments have continued to decline as a share of GDP until 2021, but we expect this trend to have reverted in 2022 and in the coming years. In fact, over the recent months, rapidly rising interest rates have significantly increased the debt-servicing costs of Eurozone governments and raised concerns about debt sustainability. We estimate the public debt burden to have already increased notably last year, at least in France and Italy (from 1.4% to 2.1% of GDP and from 3.6% to 4% of GDP, respectively) (Figure 9). Despite debt management agencies having secured increasingly longer maturities (weighted average maturity ranges between 7.9 years in Germany and Italy and 8.6 years in France), contributing to reduce rollover risks, debt sustainability will remain in the spotlight.

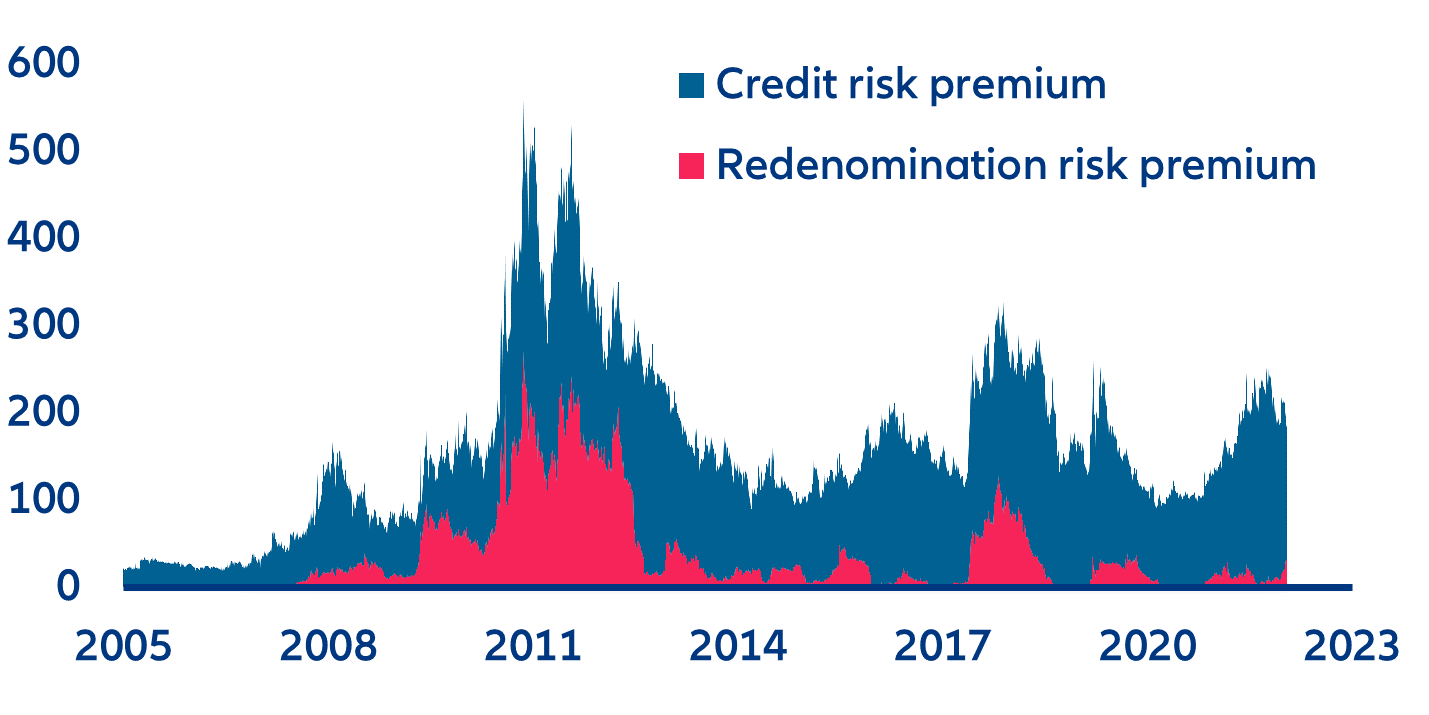

Higher borrowing costs will put more pressure on government budgets and could raise fragmentation risk. Scaled-up public sector support since the onset of the pandemic and throughout the energy crisis has widened budget deficits and delayed much-needed fiscal consolidation. Moreover, we expect fiscal adjustment to happen only gradually in all large Eurozone economies (except in France which will see its budget deficit increase to 5.5% of GDP in 2023), making it difficult for countries to reduce elevated government debt levels. Over time, this could also increase fragmentation risk as more vulnerable Eurozone economies, such as Italy, experience a widening of their sovereign spread. However, our estimates suggest that this risk remains rather small, also thanks to the signaling effect of the ECB’s transition protection instrument (TPI) (Figure 10). All the draft budget plans submitted to the European Commission at the end of last year still point to fiscal expansion in 2023, given the extension of measures to mitigate the impact of high energy prices on households and firms in the Eurozone in 2023.

Figure 6. Eurozone—Projected Eurosystem holdings under the PSPP (EUR trillion)

Sources: Refinitiv, Allianz Research

Figure 7. Eurozone—Projected Eurosystem reinvestment of PSPP holdings and government net borrowing (2023)

Sources: Refinitiv, Allianz Research

Figure 8. Germany—impact of QT on the 10Y Bund term premium (bps)

Sources: ECB, Eser and others (2019), Refinitiv, Allianz Research. Note: assuming full reinvestment since end of overall asset purchases in mid-2022 and start of tapering in March 2023; based on the current weighted average maturity of the Eurosystem's government bond holdings under the PSPP; */ reinvestment capped to EUR15bn/month.

Figure 9. Government debt burden (% GDP)

Sources: Refinitiv, Allianz Research

Figure 10. Decomposition of Italy’s risk premium* (10y vs Germany, bps)

Sources: Refinitiv, Allianz Research. Note: */ based on variance decomposition.

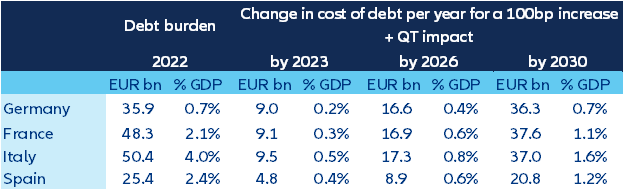

The combined impact of increasing policy rates and QT will adversely impact medium-term debt dynamics (Table 1 and Figure 11). Assuming both government debt ratios and average maturity are kept constant over the next 10 years, a lasting increase in interest rates by 100bps (together with a progressively higher term premium due to QT across countries) means that the additional financing costs in relation to GDP will tally up to 0.7% in Germany, 1.1% in France, 1.2% in Spain and a significant 1.6% in Italy by 2030.

Table 1. Government debt current and additional financing costs

Sources: Refinitiv, Allianz Research. Note: */ based on variance decomposition.

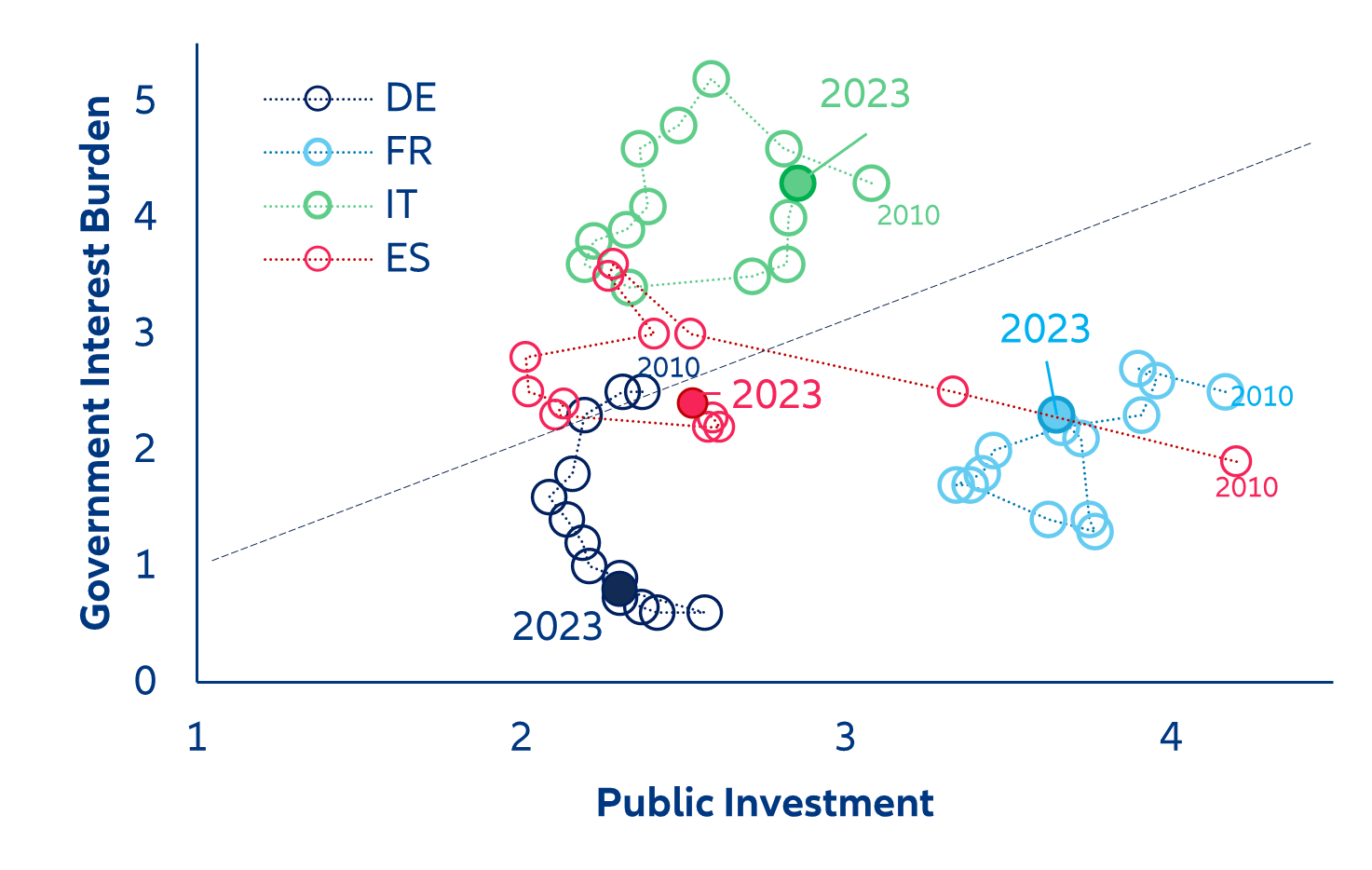

Additional debt-servicing costs could come close to the scale of public investment relative to GDP by the end of the decade. Despite Eurozone economies having benefitted from favorable financing costs in the wake of the sovereign debt crisis, public investment has stagnated despite critical structural challenges that require higher government expenditure in infrastructure (Figure 11). To avoid the interest hangover ahead and protect fiscal space for spending on the much-needed green and digital transition, governments need to enhance fiscal discipline and/or adopt growth-friendly policies that can help boost real growth.

Figure 11. Government debt burden vs. public investment (% of GDP, 2010-2023)

Sources: Refinitiv, Allianz Research. Note: 2022 and 2023 public expenditure rates are kept constant at 2021 levels.