- Eurozone corporate profit margins reached 40.8% of gross value-added at end-2022 (+0.6pp above the long-term average). But the devil is in the details. Italy and Spain seem better positioned compared to Germany and France, notably in the manufacturing sector. However, excluding sectors with strong pricing power (such as transportation services and energy), margins are much lower and hit their lowest level since the mid-1980s in Q1 2023 in France.

- Margins remain well below the pre-pandemic average in consumer services, with France being worst positioned (28% vs 37% in the EU and 45% in Italy). Despite resilient demand for services, companies face stiff competition, rapid wage increases and negative productivity growth (since the pandemic), limiting the extent to which they can increase their selling prices above input costs.

- German companies appear best in class in terms of profitability in the agriculture and construction sectors. Construction companies in particular have used the general upward trend in prices to significantly expand their profits to reach 53% of gross value added – even compared to other large European economies (36% in France, for example).

- Corporate profits should be past the peak amid strong wage pressures and diminishing pricing power (and even deflationary forces in metals, chemicals). While producer prices are decelerating strongly amid lower commodity prices, normalizing supply chains and growing deflationary fears in China, wage growth will remain high at least until early next year, which will contribute to squeezing corporate margins. The exception will be the services sector, which will delay the fall in service price inflation.

In focus – Past the peak – European corporate margins down again?

Higher oil prices yet Europe is closing its energy gap

Oil prices should increase until the end of 2023 in response to persistent demand and supply uncertainties. A resilient global economy is keeping oil demand strong and the prospect of a positive summer season in the West will also support demand for transportation fuels. While oil prices have declined since the start of the year, short bets are likely to unravel in the coming months as the supply outlook has been shifting, too:

- The US shale industry, a key player in global oil supply, is prioritizing profits over volume. Although crude oil prices are still above the breakeven price for US shale players (estimated at about USD55/bbl), higher interest rates and growing wage bills have led the already highly leveraged sector to focus on profitability. This strategic shift will limit US oil output, thereby widening the supply-demand gap

- Saudi Arabia, the world's leading oil exporter, just decided to cut its oil production during last week’s OPEC+ meeting. This move is a strategic gambit aimed at stabilizing the global oil market and supporting oil prices. Saudi Arabia's commitment to reducing output will deepen the deficit, potentially pushing oil prices higher. But it will also pose risks to the country’s market share around the world.

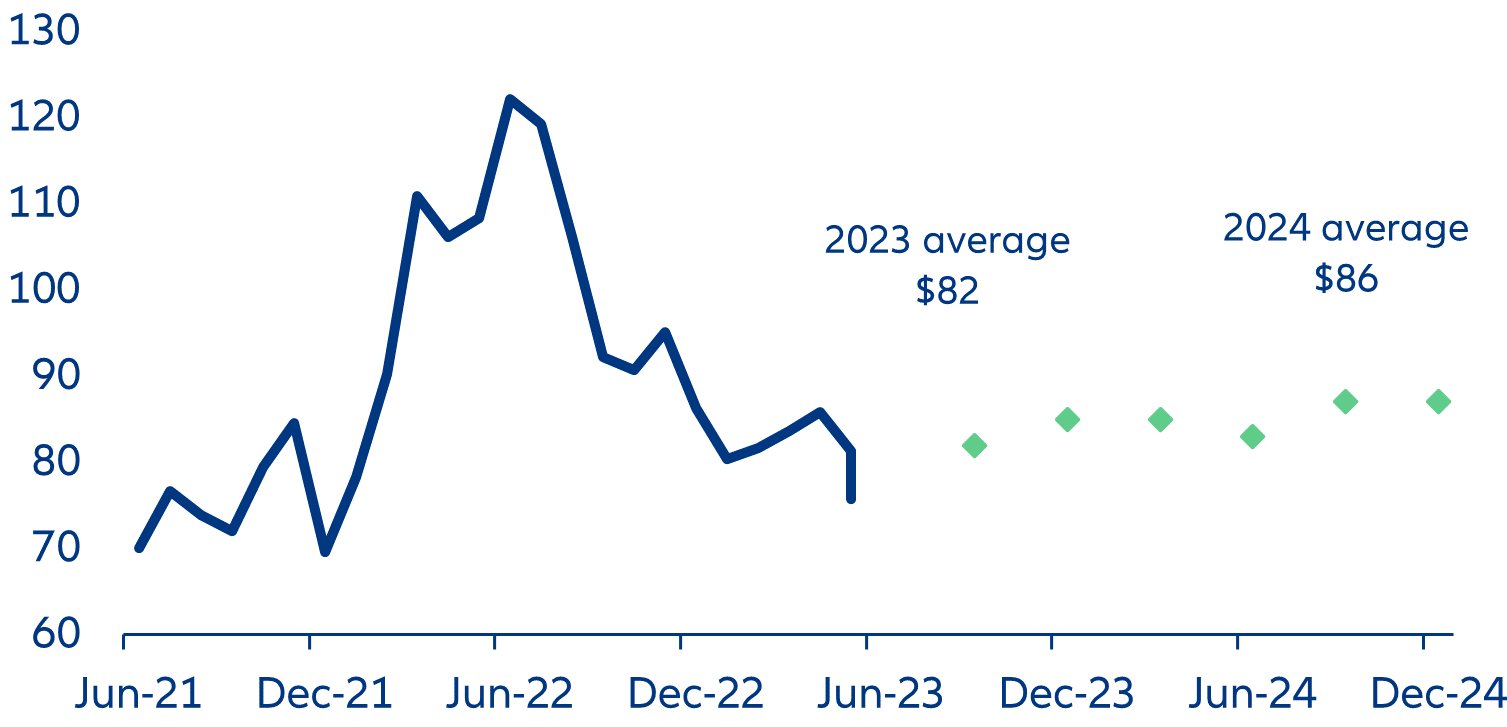

Although all recent signals point toward higher oil prices, markets remain volatile. Geopolitical developments are adding a layer of complexity, with Russia holding the key to stabilize markets through compliance on its own production targets, and also paving the way to more Saudi exports towards Asia to ease some of the tension between OPEC+. Overall, we expect Brent prices to increase throughout the year and average USD82 for 2023 (Figure 1). Nevertheless, these rising prices are unlikely to fuel an inflation spiral as oil prices are likely to remain 20% below 2022 prices.

Figure 1: Brent crude oil price forecast (USD/bbl)

Sources: Refinitiv Datastream, Allianz Research.

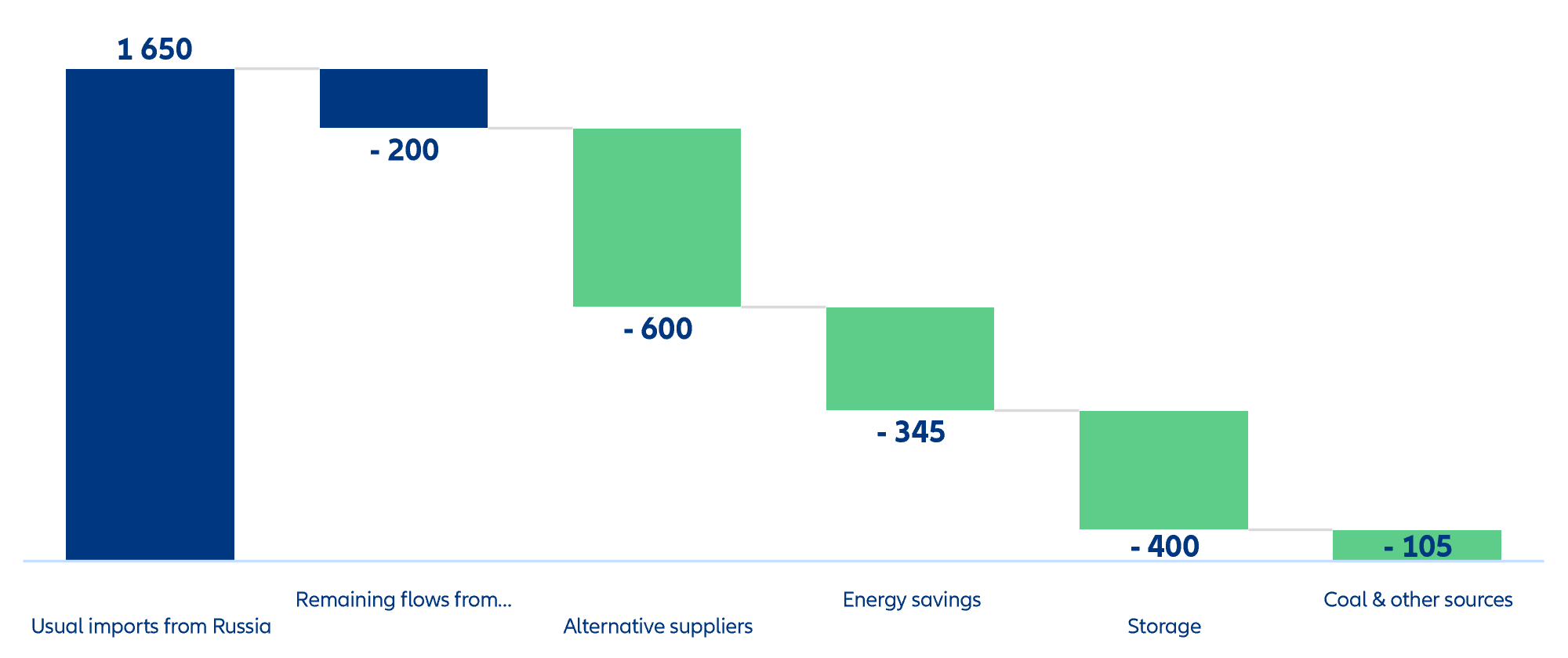

No energy gap in sight for next winter. Europe managed the energy transition from Russian gas over the 2022/2023 winter, decreasing its gas consumption by about -10%. The mild winter also allowed for some extra savings. As a result, gas storage levels are high (over 70% as of 06 June). Considering that energy savings made last winter are sustainable, we expect no energy gap for the next one. In the event of a very cold winter, Europe would probably face price tensions and dig deep into storage but we believe the region will overcome that eventual hurdle (Figure 2). It is likely that China will compete in the race for LNG as it imported -20% less compared to normal in 2022, which could divert some of the supply from Middle Eastern countries or Australia towards China, and create upside price tensions.

Figure 2: Gas substitution in Europe (TWh)

Sources: Eurostat, Allianz Research.

Central Banks are not done – Fed and ECB rates to peak only in September

Ahead of the next round of monetary policy meetings, slowing inflation in both the US and the Eurozone begs the question of whether financing conditions have tightened enough for the Fed and the ECB to alter the policy rate path. While equity markets have retraced half of their declines from last year, considering that the full effects of monetary tightening have yet to materialize, does the current pace of declining inflation warrant further rate hikes at all?

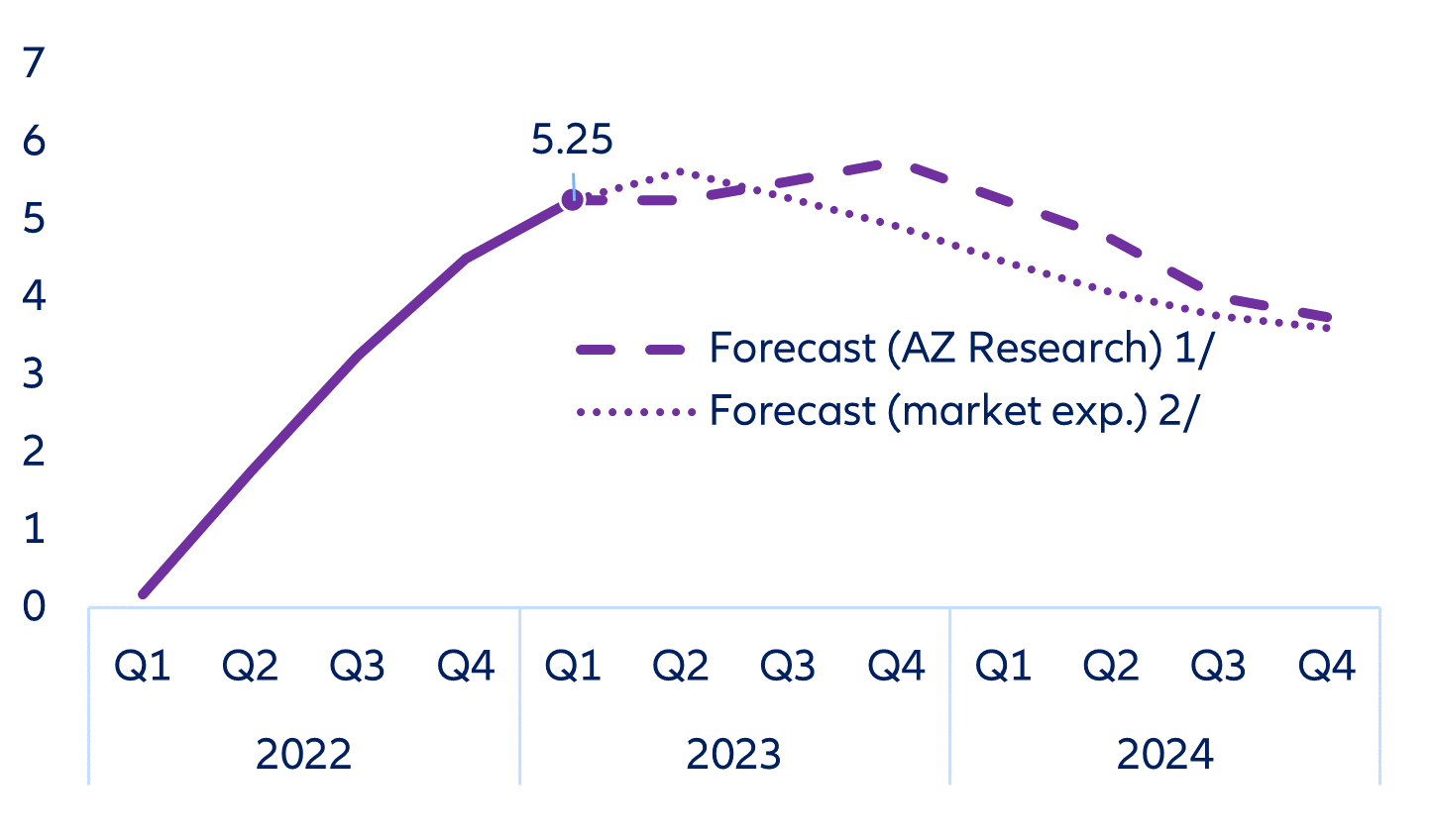

US Federal Reserve: Holding off next week but to deliver two more rate hikes in July and September

With the debt ceiling standoff now in the rearview mirror and hard economic data coming out strong, the Fed might not to pause its hiking cycle at its upcoming FOMC meeting on 13-14 June. According to the payroll survey, the economy created 340,000 jobs in May, the strongest pace since January, while weekly unemployment claims remain subdued, at around 230,000. Meanwhile, real personal consumption-expenditures growth stepped up to a healthy +0.5% m/m in April, and timelier weekly card payments point to continued expansion in May. On the corporate side, non-residential construction is surging, buoyed by new manufacturing plants (especially for battery and semiconductors). Against this backdrop, core inflation and wage growth remain way too high. For instance, average hourly earnings have not cooled persistently, edging up +0.3% m/m in May – about the same pace as the 12 prior months. Finally, overall bank lending continues to increase at a solid clip, although C&I loans to corporates show more signs of weakening in recent weeks.

Figure 3: US – Federal Funds rate (market expectations and forecast) (%)

Sources: Refinitiv Datastream, Allianz Research

However, several FOMC participants poured cold water on the idea of hiking in June, opting for a ‘wait and see’ approach. Phillip Jefferson, who has been nominated to be the Fed’s next Vice Chair, argued that “skipping a rate hike” would allow officials to “see more data before making decisions about the extent of additional policy firming”. FOMC participants are very mindful that monetary policy operates with long and uncertain lags. They are probably worried that the cycle may turn down abruptly in upcoming months. For instance, renewed bouts of stress in the banking sector could trigger a credit crunch. Also, while hard data have come out strong, the latest business surveys point to rapidly cooling momentum, while the household employment survey reported a decline in jobs (in contrast to the payroll survey) in May and an uptick of the unemployment rate. However, we think that the reality of strong economic momentum will strike back at the FOMC in upcoming weeks. Business surveys have tended to send excessively downbeat messages over the past few months (negative sentiment and softer goods price probably bias the results).

Whether or not the Fed delivers another rate hike is a close call, but overall, we think that FOMC participants will hold off this time (Figure 3). However, we expect the Fed to resume hiking both in July and September by delivering two final 25bps rate increases as still elevated wage and price pressures force its hand. Weaker momentum should materialize in end 2023-early 2024. As a result, the Fed should reverse course in Q1 2024.

ECB: Two more rate hikes before the summer break and a final back-to-school hike

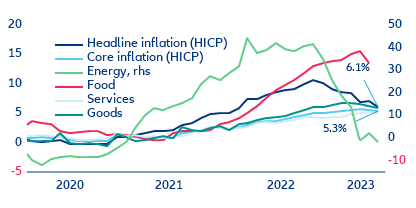

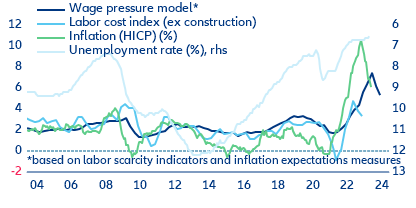

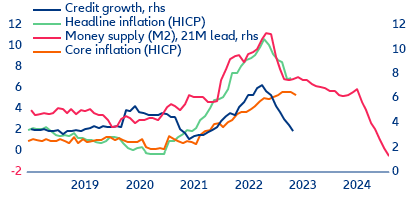

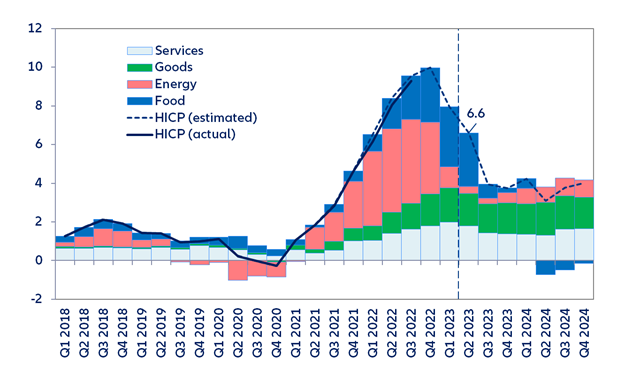

In the Eurozone, inflation keeps declining but still remains far too high (Figure 4). The drop in headline inflation to 6.1% y/y in May (down from 7.1% in April) was larger than expected due to deflationary energy prices (-1.7%) and declining food inflation (12.5%). More importantly, however, core inflation, the ECB’s guidepost for calibrating its monetary stance, declined to 5.3% (down from 5.6%), which was below consensus expectations and marked a four-month low. Unlike in April, selling-price expectations now show less divergence between goods and services. While core goods inflation decreased further to 5.8%, suggesting that the easing in supply bottlenecks and falling energy prices are increasingly feeding through, services also surprised on the downside at 5.0% (after 5.2% in April) despite continued tightness in the labor market, with the unemployment rate edging down to a record low of 6.5% in April. Thus, we expect price pressures, especially for services, to remain strong and elevated during the remainder of the year. This is also when inflation uncertainty is the highest, with wages still accelerating and robust demand, for tourism notably (Figure 5). The base effects from the nine-euro-ticket for public transport in Germany last year will also push services inflation up in June. As a result, the core inflation rate will decline only slowly. As money supply keeps contracting, it is hard to see a relapse of inflation, even though some bumps along the way of normalizing prices cannot be ruled out (bar any financial sector accidents or potential crisis event) (Figure 6). Over the medium-term, inflation will remain above the ECB’s 2% price-stability target, with headline inflation averaging almost 6% this year and about 3% next year.

Figure 4: Eurozone – headline inflation components (%)

Sources: Refinitiv Datastream, Allianz Research

Figure 5: Eurozone – labor market developments (%)

Sources: Refinitiv Datastream, Allianz Research

Figure 6: Eurozone – money supply, credit growth and inflation (y/y %)

Sources: Refinitiv Datastream, Allianz Research

Broad price pressures still create a challenging environment for monetary policy in the Eurozone. The conspicuous decline in inflation is unlikely to dissuade the ECB from further raising interest rates. Also the lack of spillover effects from US banking-sector stress means that financial stability concerns will be insufficient for the ECB to abandon its restrictive monetary stance. However, the disappointingly small rebound in German industrial production in April, deteriorating business confidence, and stagnant investment suggest that the ECB would need to decide on a policy rate path that does not excessively slow aggregate demand (considering that the impact from rapidly tightening financing conditions operates with considerable lag).

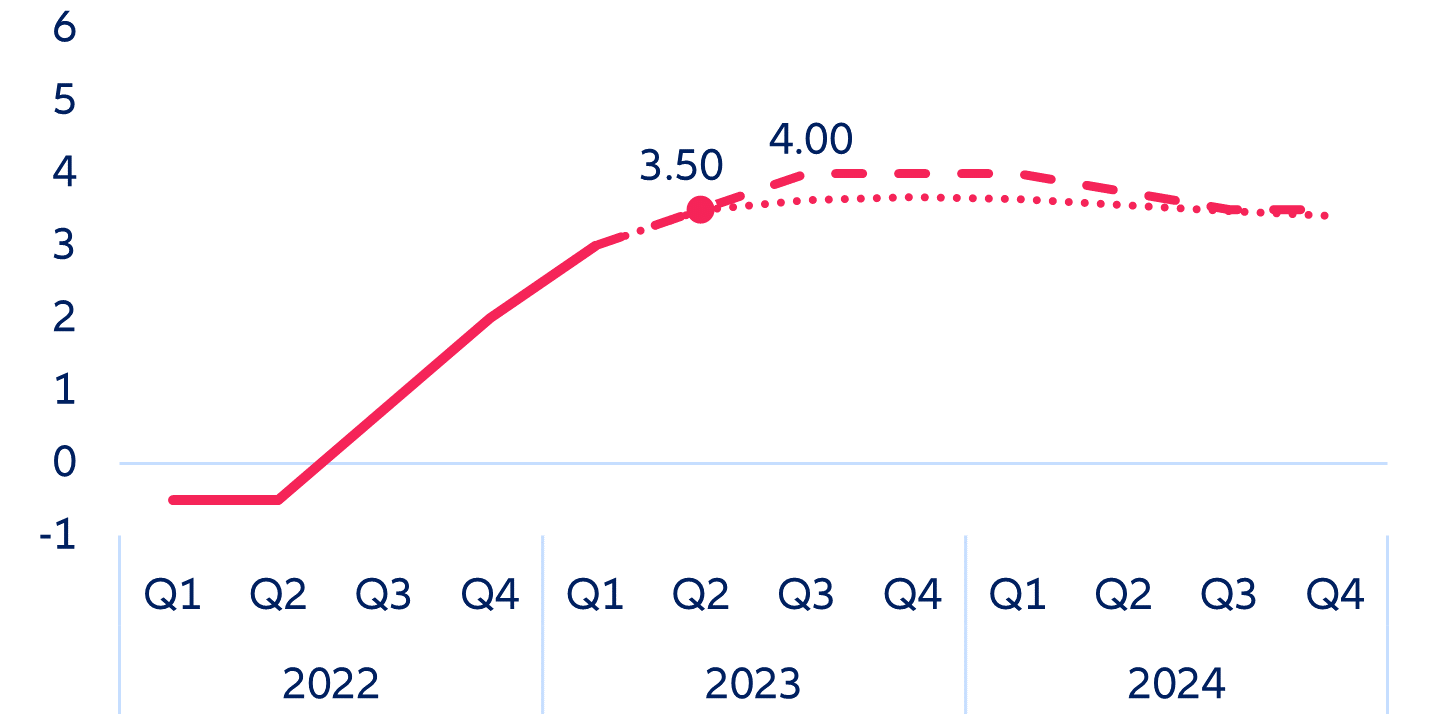

Since the normalization of inflation is more protracted than in the US, high core inflation will reinforce the ECB Governing Council’s conviction that further rate increases are still needed (Figure 7). After the 25bps hike at the last meeting we forecast three more 25bps hikes in the next policy meetings in June, July and September for a terminal rate of 4.0%. This would mean the ECB maintains a restrictive stance in 2023 despite stagnating growth until Q1 2024.

Figure 7: Eurozone – headline inflation forecast (y/y %)

Sources: Refinitiv Datastream, Allianz Research

Figure 8: Eurozone – ECB deposit facility rate (market expectations and forecast) (%)

Sources: Refinitiv Datastream, Allianz Research

Bank of Japan’s change of heart – only slight changes in 2023 to remain supportive and possibility of important shift in 2024

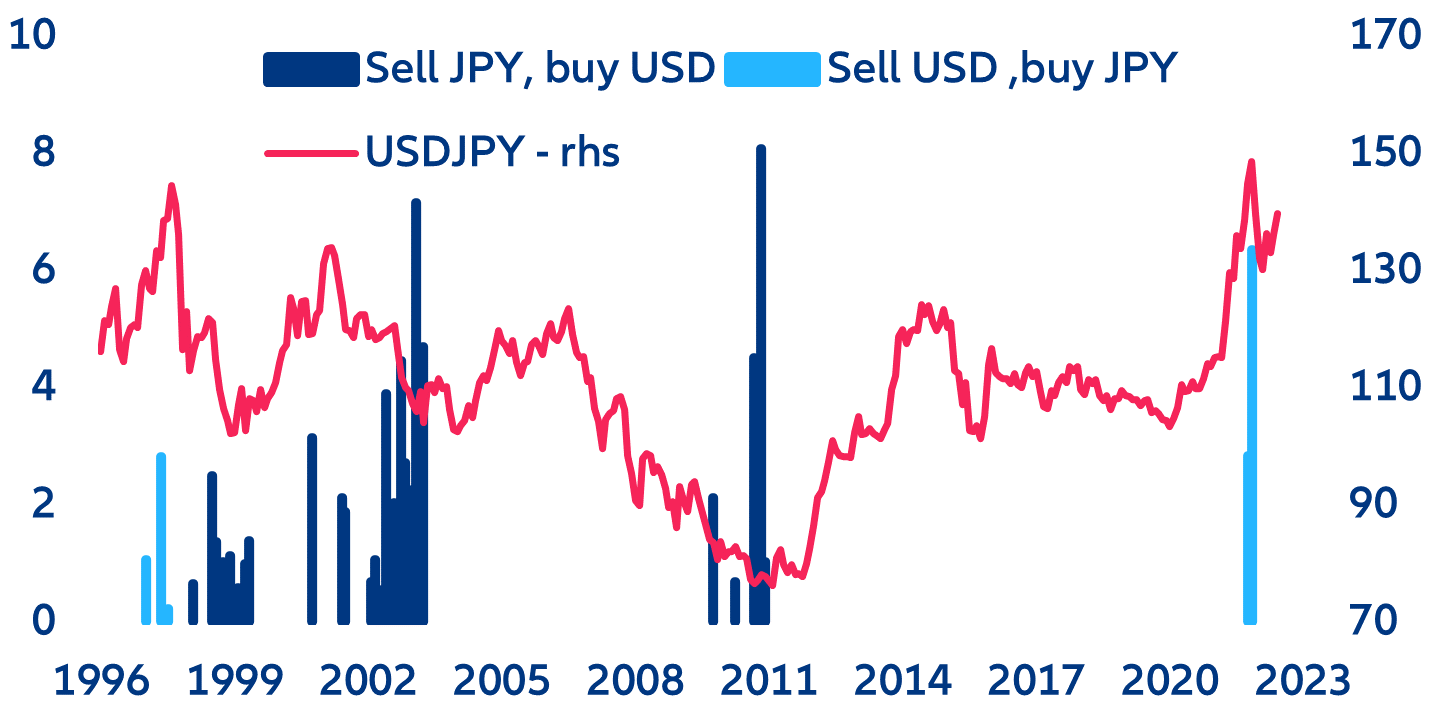

Unlike most other central banks, the Bank of Japan (BoJ) stood firm on its ultra-loose monetary policy stance and resisted the multiple headwinds that led to a 26.5% JPY depreciation vs the USD since the end of 2020 – FX intervention included (Figure 9) – and speculative attacks on the Yield Curve Control (YCC) policy. As inflation starts to recede (after peaking at 4.4% y/y), we think that the BoJ policymakers will refrain from making a sharp turn this year. Instead, we expect them to opt for a further relaxing of the YCC objective, proceeding with a small hike that ends the policy of negative interest rates (though real interest rates remain negative for now).

Figure 9: Yen exchange rate fluctuation and FX interventions

Sources: Ministry of Finance Refinitiv, Datastream, Allianz Research

Figure 10: Share of Japan sovereign bonds owned by the BoJ

Sources: BoJ, Ministry of Finance, Refinitiv Datastream, Allianz Research

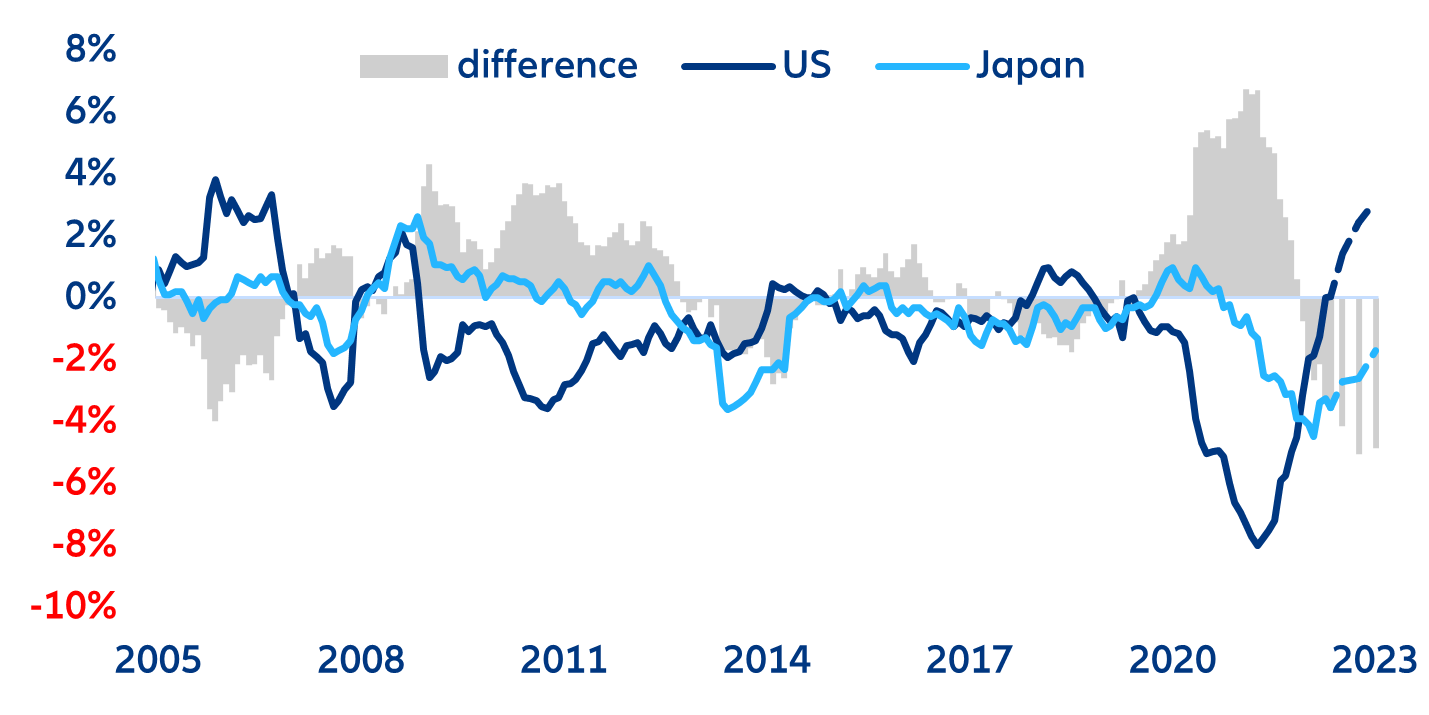

Once the Monetary Policy Review launched by the new governor Kazuo Ueda sheds some light on the effectiveness of the unorthodox monetary policy and the externalities it has created in other areas of the economy, we could see a fundamental policy change in 2024. Especially since the results are expected by the first half of 2024, once the path of the economy and inflation is clearer and once the first effects of the slow adjustment of monetary policy are visible. A strong economy coupled with wage growth, 2% inflation expectations and the smooth functioning of financial markets would be the best scenario to kick off the path to a full normalization. However, further pressures on Japanese yields due to a large interest rate differential to the US dollar (Figure 11) and, thus, structural JPY weakness (hampering the current account surplus) or the need to increase even further the participation in local financial markets could also trigger the normalization.

Figure 11: Real interest rate differentials between the US and Japan

Sources: Refinitiv, Allianz Research

The BoJ decisions will have implications for the rest of the world, given Japan’s creditor status and its large holdings of foreign assets. The increase in yields that would follow the exit (total or partial) from YCC would increase the investment appetite for Japanese bonds. The return to the market would be welcomed by both Japanese investors repatriating their money or overseas investors in search of attractive yields on a safe-haven asset. Furthermore, it would coincide in time with the gradual withdrawal from the market of other central banks in advanced economies. For instance, Japanese investors (both public and private sector) hold around 6% of French sovereign debt.

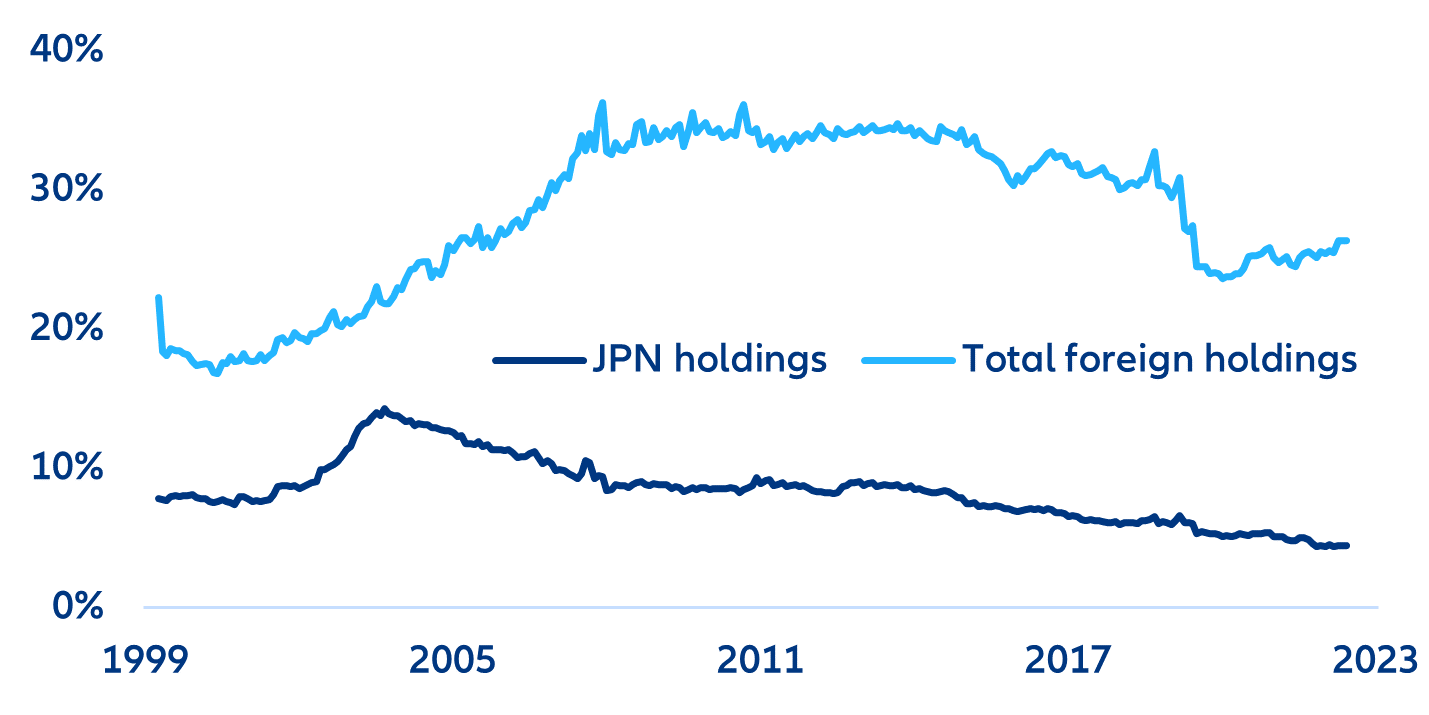

At the same time, the BoJ might rebalance asset purchases towards US Treasuries to contain a potential appreciation of the JPY (as they did in the early 2000s). It is rather in the event of continued inaction when Japanese intervention to avoid a further depreciation puts upwards pressure on US yields. After all, Japan is the second- largest holder of FX reserves and the main foreign holder of US debt (although very close to China, and with a share that has decreased over time (Figure 12)).

Figure 12: Holdings of US treasuries

Sources: BoJ, Ministry of Finance, Refinitiv Datastream, Allianz Research

In focus – Past the peak – European corporate margins down again?

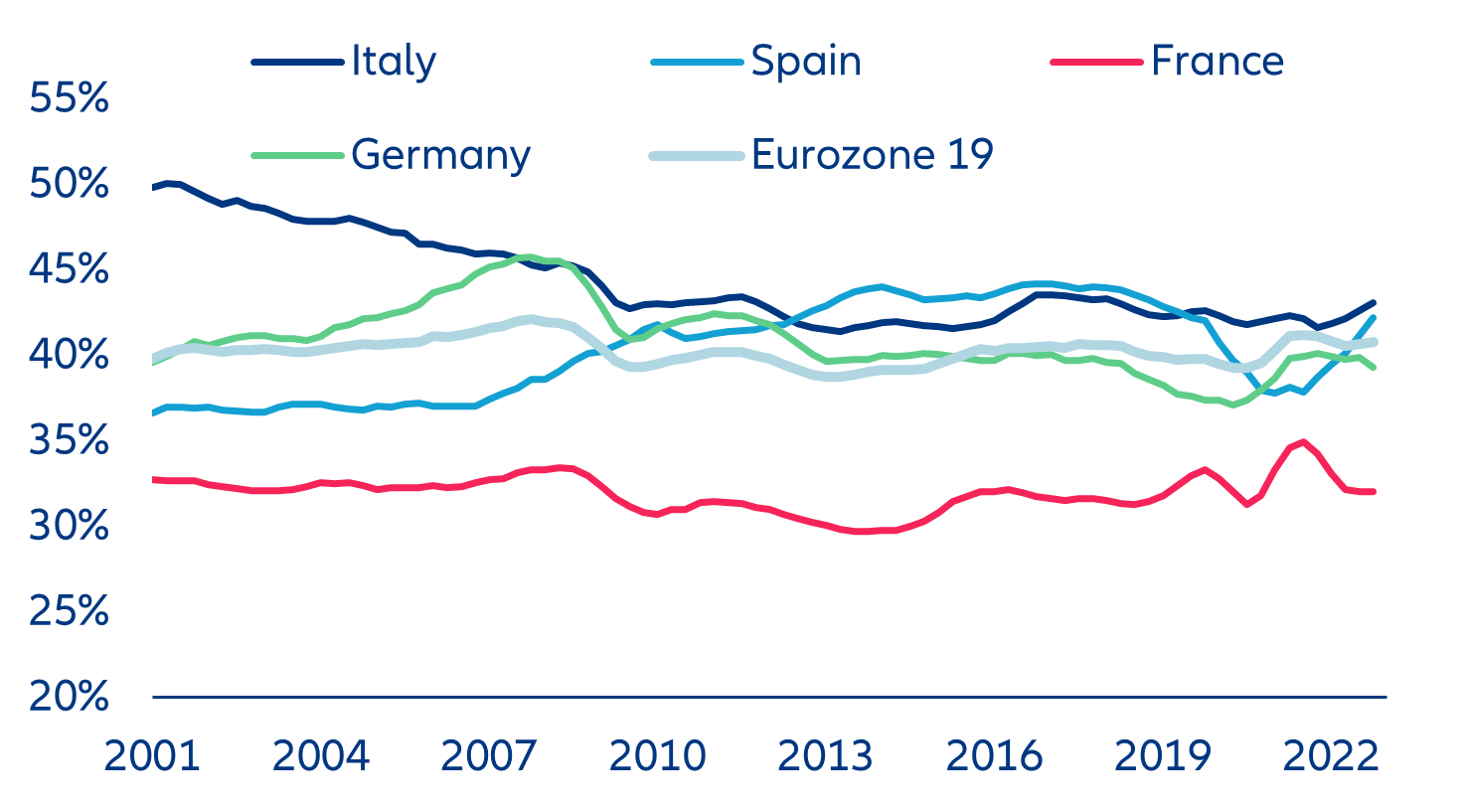

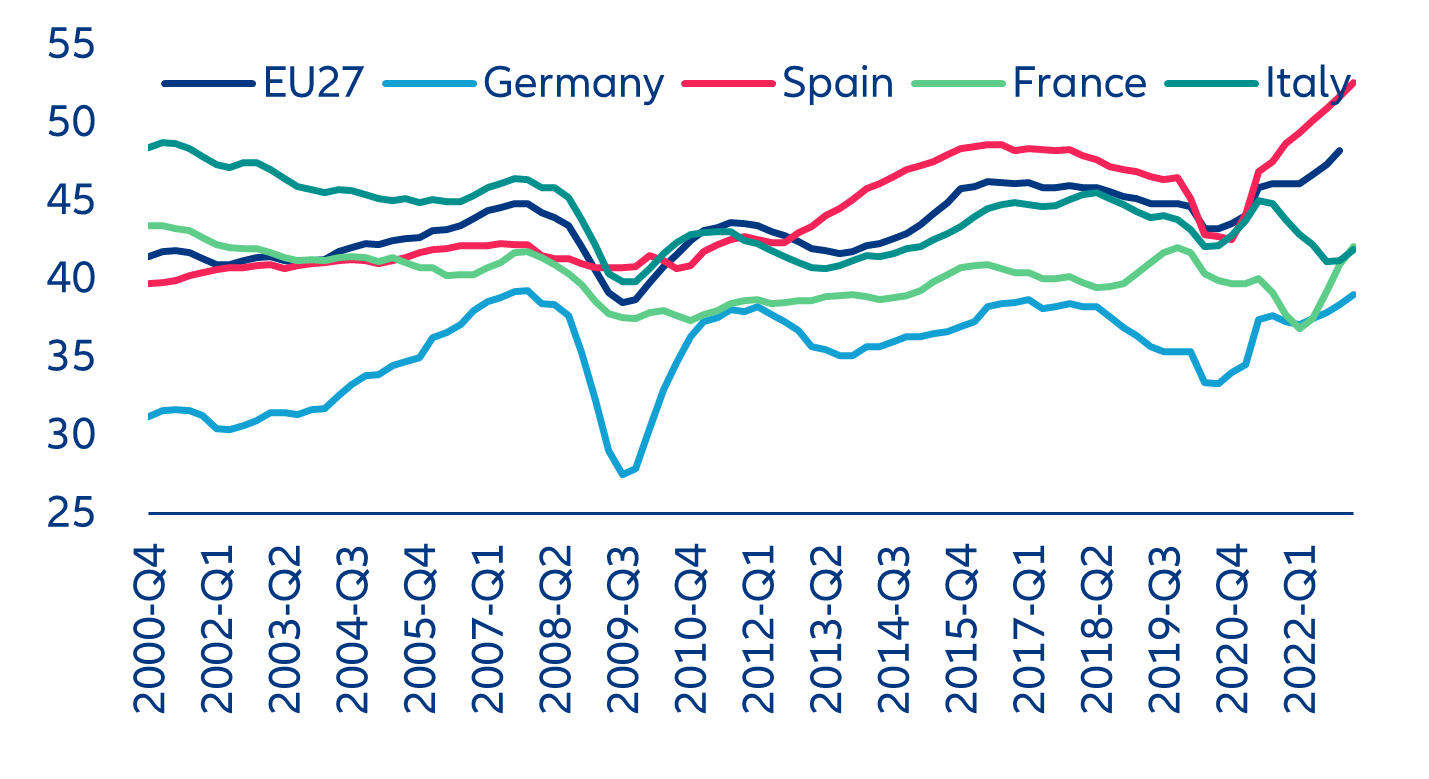

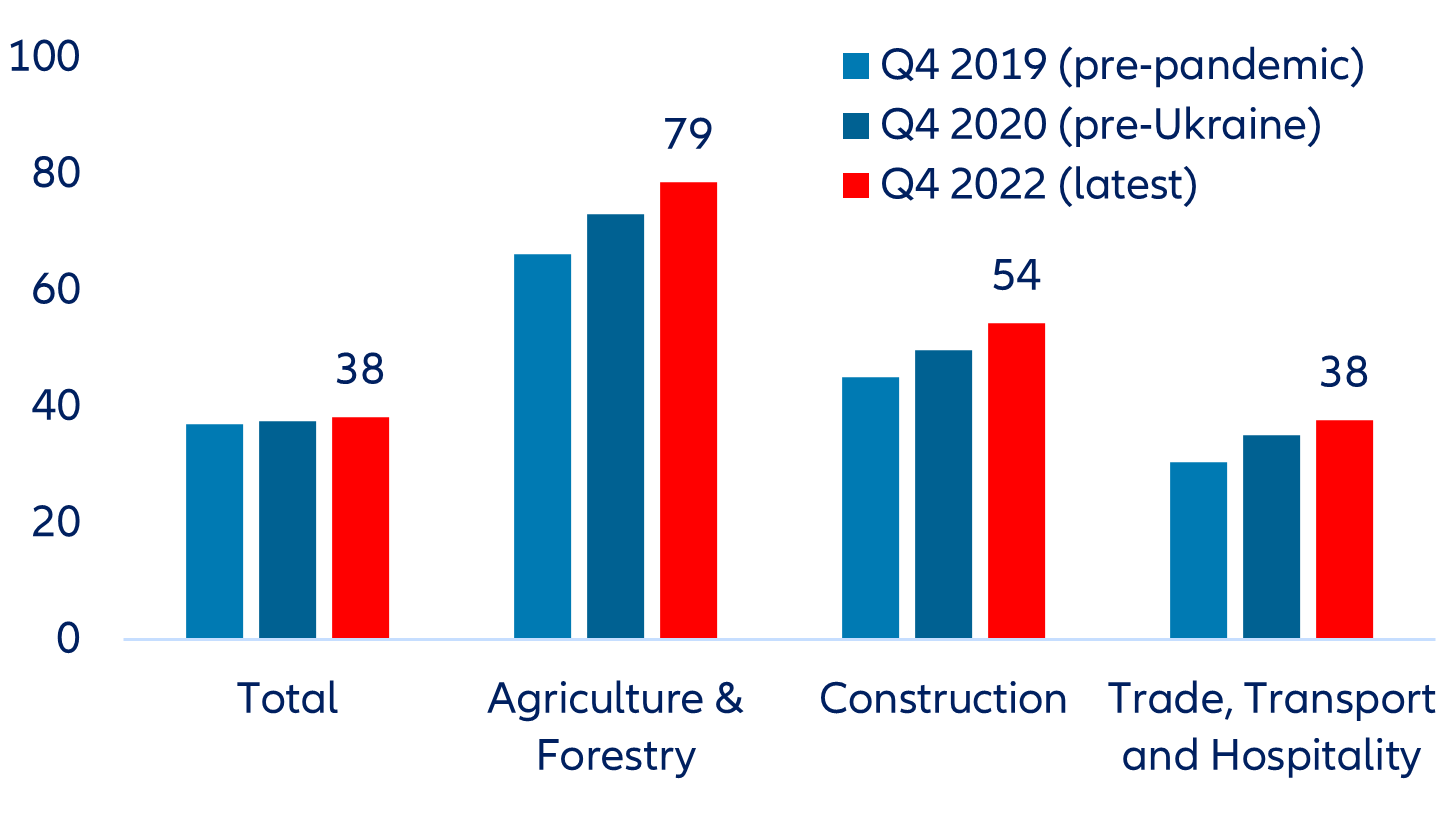

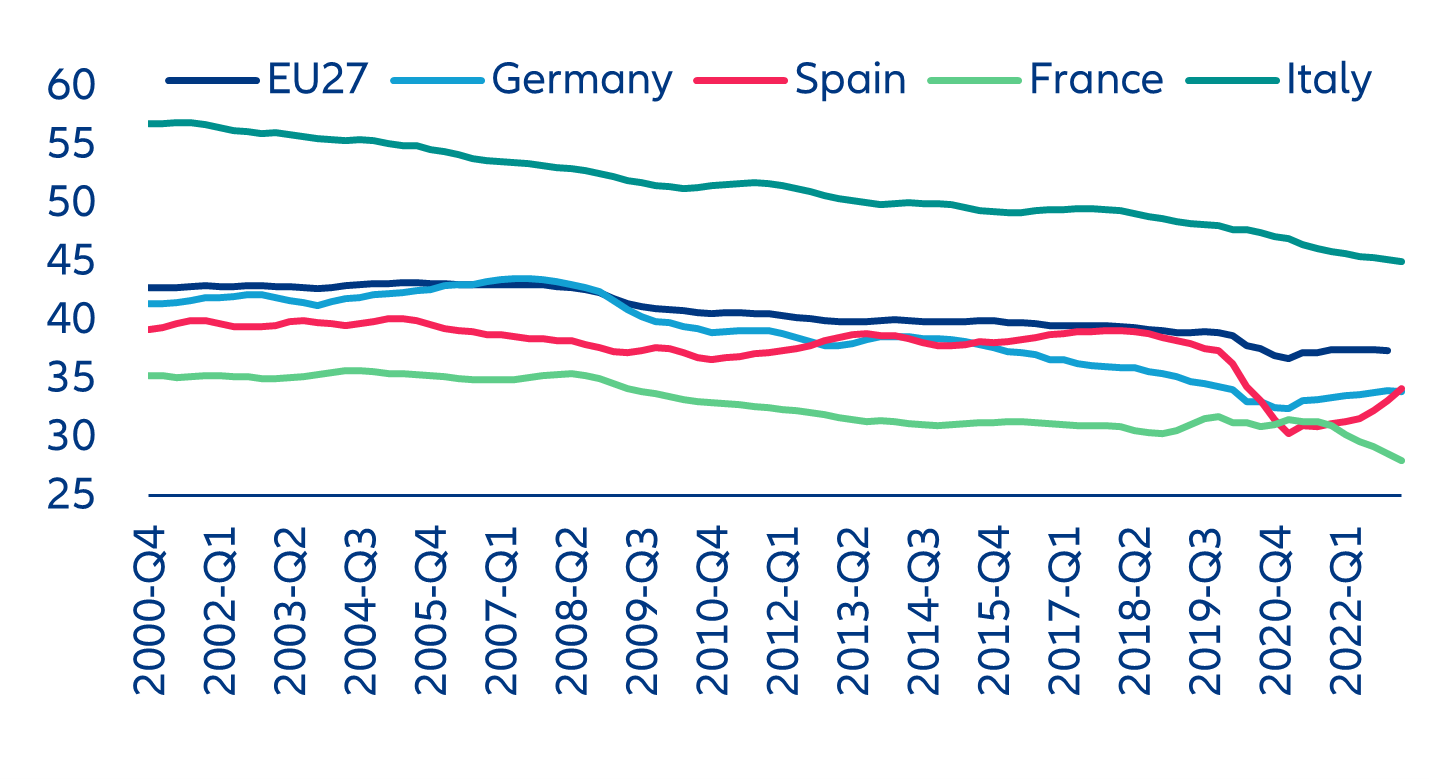

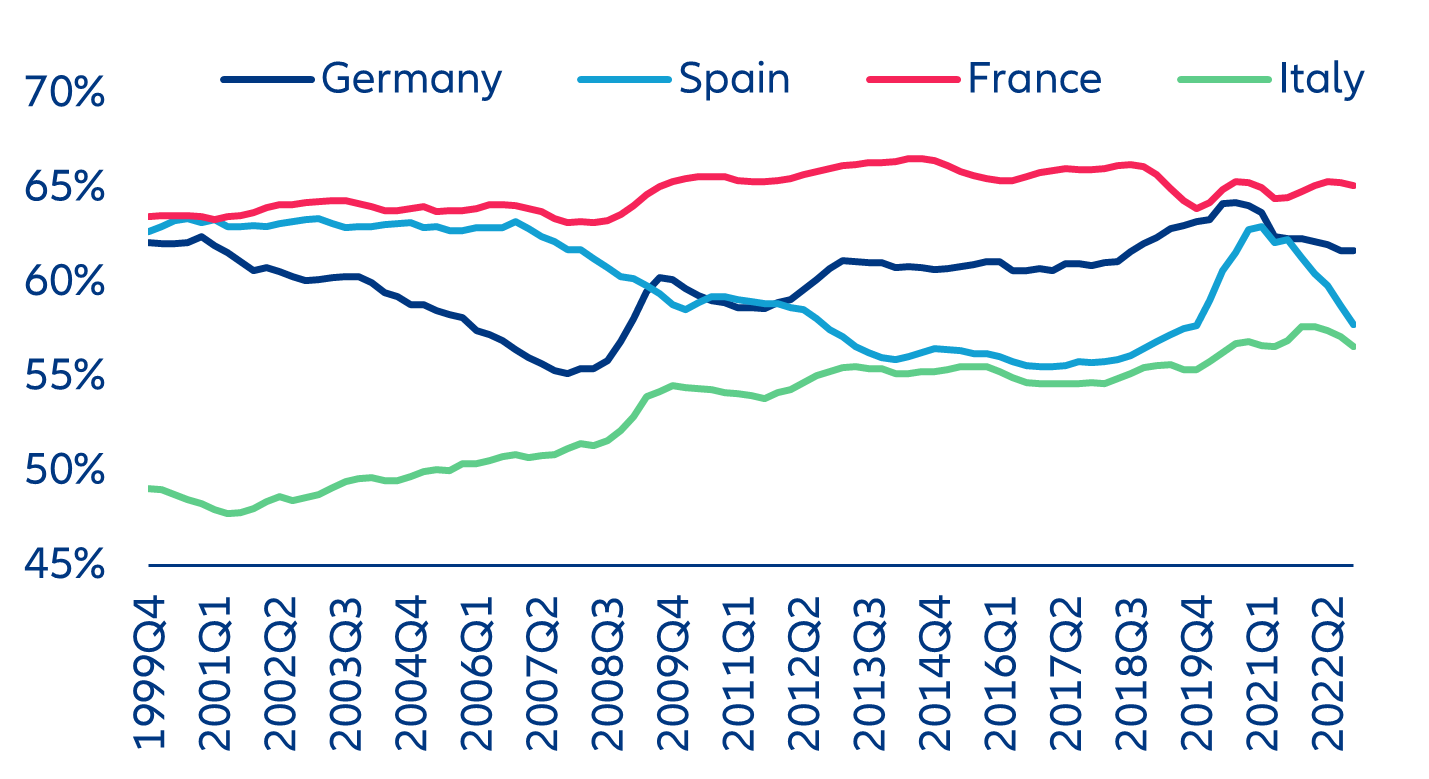

Corporate profit margins in the Eurozone have improved during the recent crises. At 40.8% of gross value-added as of end-2022, the margins of non-financial corporates are on average +0.6pp above the long-term average, with Italy and Spain better positioned compared to Germany and France. However, there are significant differences across sectors. Profit margins have widened particularly in agrifood, where retailers were able to increase their margins to 78.6% in Q4 2022 (12.3pps higher than the pre-pandemic level in Q4 2019). Similarly, in construction, the share of profits stood at 54.4% (9.3pps higher than pre-pandemic levels). In the manufacturing sector, Spain remains best positioned, given its competitive edge and the implemented reforms (Figures 13 and 14). In the food industry in particular, the French margin rate now sits well above its pre-pandemic average (at 48.1% in Q1 2023, versus a pre-pandemic average of 40%) as input costs are falling (including energy), while the actors in the sector are bumping up their selling prices. Similarly, in Germany, sales prices in many industries have increased significantly more than would have been justified by the development of purchase prices. However, the current increase in profit margins is remarkable considering their secular decline over the last two decades. In fact, two sectors contributed massively to supporting the aggregate margin rate since 2021: transportation services and energy. Stripping out these two sectors, in France, the total margin rate remained depressed at its lowest level since the mid-1980s in Q1 2023.

Figure 13: Non-financial corporates’ margins, % of gross value added

Sources: Eurostat, Allianz Research

Figure 14: Proxy of margins for corporates in the manufacturing sector, % of gross value added

Sources: Eurostat, Allianz Research

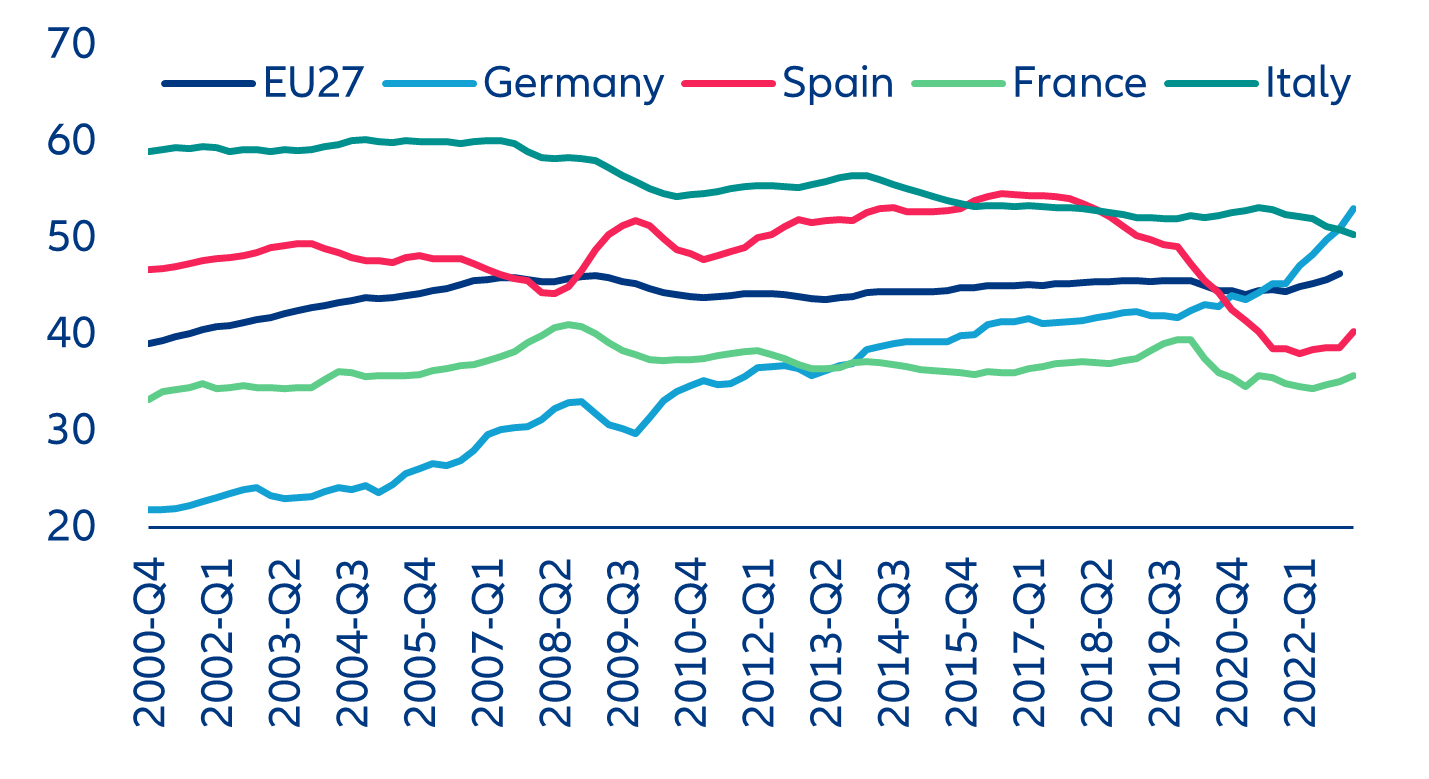

In Germany, construction companies in particular have used the general upward trend in prices to significantly expand their profits. Besides the agricultural sector, construction has seen the largest increase in profit margins on average – also compared to other large European economies (Figures 15 and 16). While there was still a high order backlog in German construction – both in terms of volume and value – dating back to before the pandemic and the war in Ukraine, it was amplified by low capacities, increased building-material prices and delivery bottlenecks. The cost of material has dropped again after supply-chain disruptions were resolved, and persistently low salaries in combination with strong prices increases have led to increased margins in the sector, particularly in civil engineering.

Similarly, Italy’s construction sector was able to increase prices given the pick-up in demand in the last couple of years. Indeed, the tax credit related to the “super bonus” measure implemented to improve the environmental efficiency of the housing stock pushed up demand but at the same time inflated construction-related prices. Even though we expect the housing-efficiency investment to continue, also supported by the NGEU resources, and so demand to remain buoyant, we expect a correction in the coming quarters, given also that the generous government support has been fine-tuned and re-targeted.

Figure 15: Proxy of margins for corporates in the construction sector, % of gross value added

Sources: Eurostat, Allianz Research

Figure 16: Germany: corporate profits (by sector), % of gross value added

Sources: Statistisches Bundesamt, Refinitiv Datastream, Allianz Research

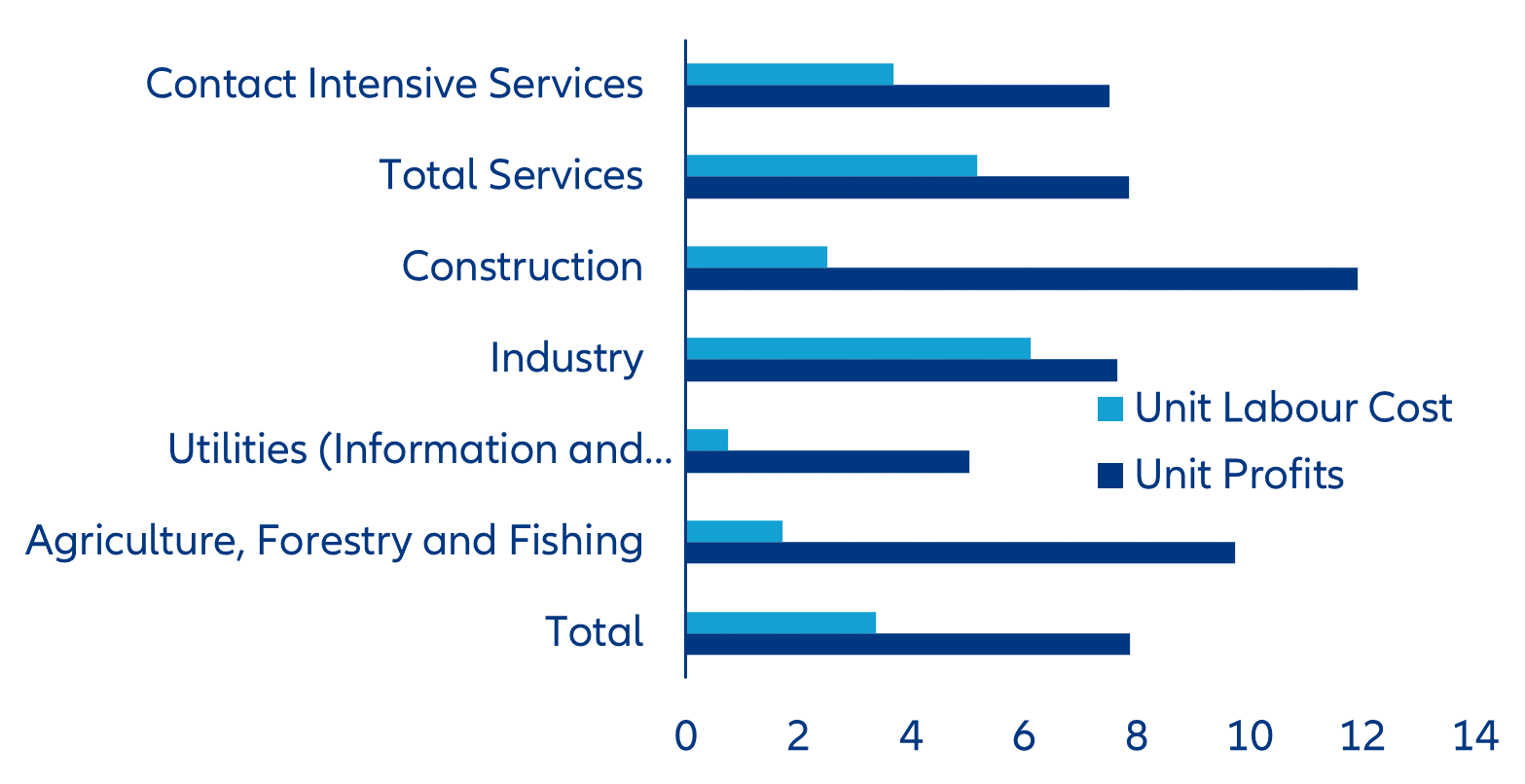

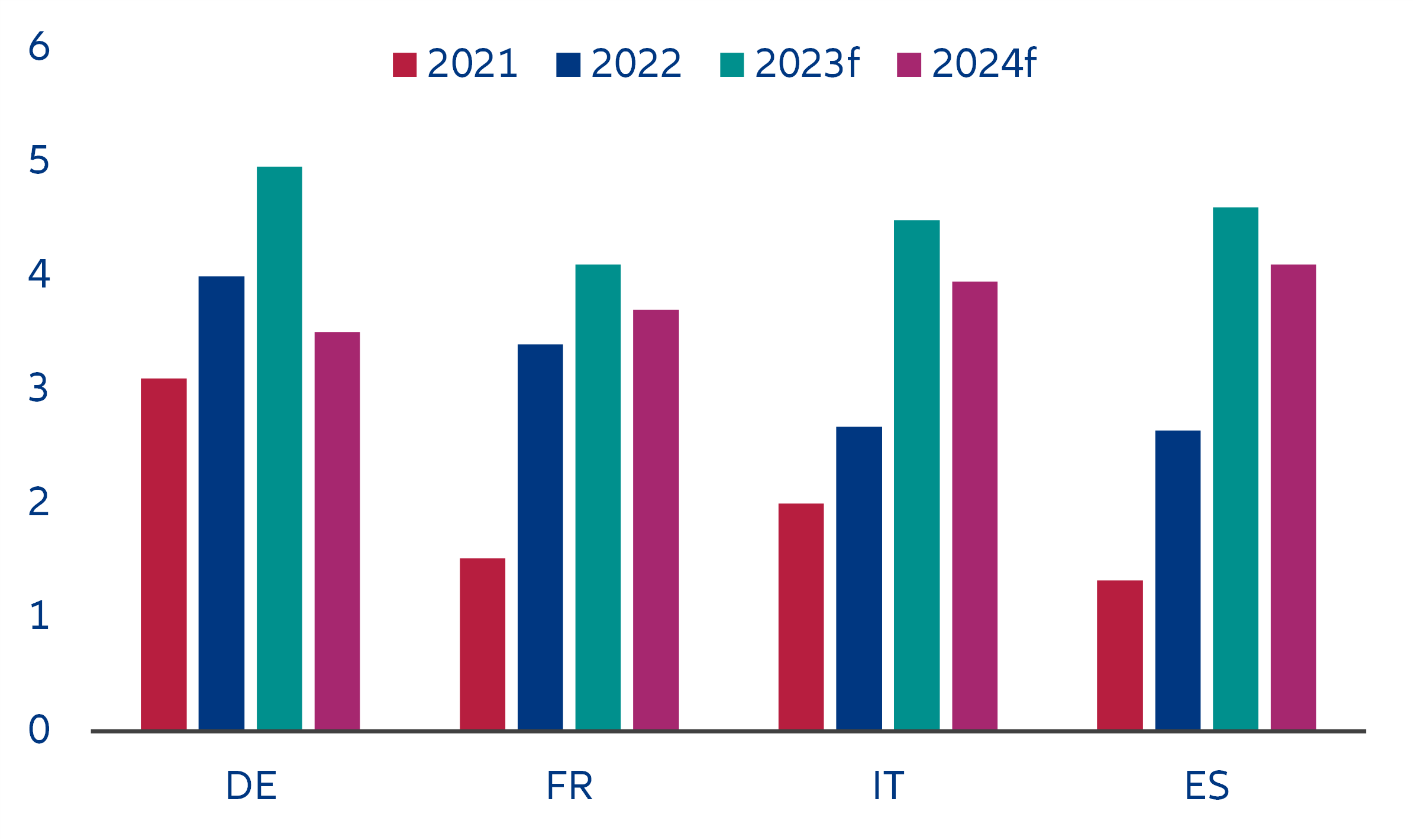

In contrast, corporate margins in services have been under heavy pressure. While energy and transportation services are oligopolistic sectors with strong market pricing power, the services sector, including hospitality, B2B services and ICT, has struggled, with margins sitting well below their pre-pandemic averages (Figure 17). In addition, these sectors have suffered from accelerating wage (amid a high share of minimum-wage earners) and input costs (Figure 18), as well as stiff competition and negative productivity growth (since the pandemic). This has limited the extent to which they can increase their selling prices above input costs, despite resilient demand for services. Indeed, business surveys in Spain show that expectations of future prices are falling. With non-negligible wage increases expected in the four major Eurozone economies for at least the next two years (Figure 19) to offset last year's real income losses caused by high inflation, pressure on margins will continue.

Figure 17: Proxy of margins for corporates in retail and services, % of gross value added

Sources: Eurostat, Allianz Research

Figure 18: Unit labor costs vs unit profits (Eurozone, 2022)

Sources: ECB, Allianz Research. NB: Unit profits are calculated as gross operating surplus / real value added

Figure 19: Eurozone big four – wage growth dynamics

Source: Allianz Research

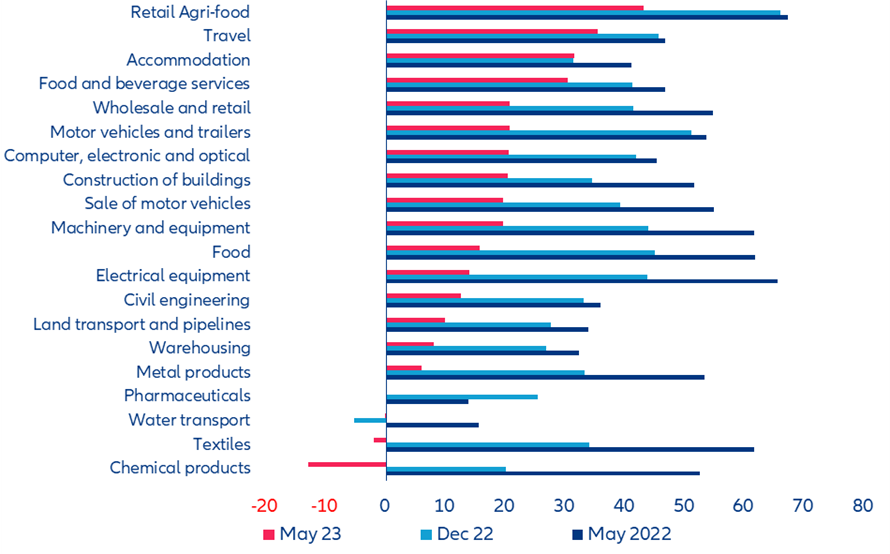

We should be past the peak in corporate profit inflation amid diminishing pricing power. The decade before the pandemic did not allow corporates to increase prices amid a regime of globalized production designed to reduce costs while real wages were stagnating. ‘Just-in-time’ strategies have also supported lower costs. The commodity price shock that followed the pandemic, the energy crisis and supply-chain bottlenecks in critical inputs (chips, freight transportations) gave firms in downstream sectors a sort of monopoly to support strong and immediate profit inflation. Several upstream sectors also acquired systemic significance, such as logistics and trucking. However, the latest indicators on pricing power suggest that a certain deceleration is gaining traction (Figure 20), and even deflationary forces are starting to become visible (metals, chemicals, textiles). Thus, the potential loss of value added in terms of total wages – as activity is slowing down (Figure 21) – would still give a limited impulse for price increases.

Figure 20: Price expectations by sector – Eurozone countries

Sources: Eurostat, Allianz Trade

Figure 21: Wage pressures, % of gross value added

Sources: Eurostat, Allianz Research

Box - Is greedflation over in France?

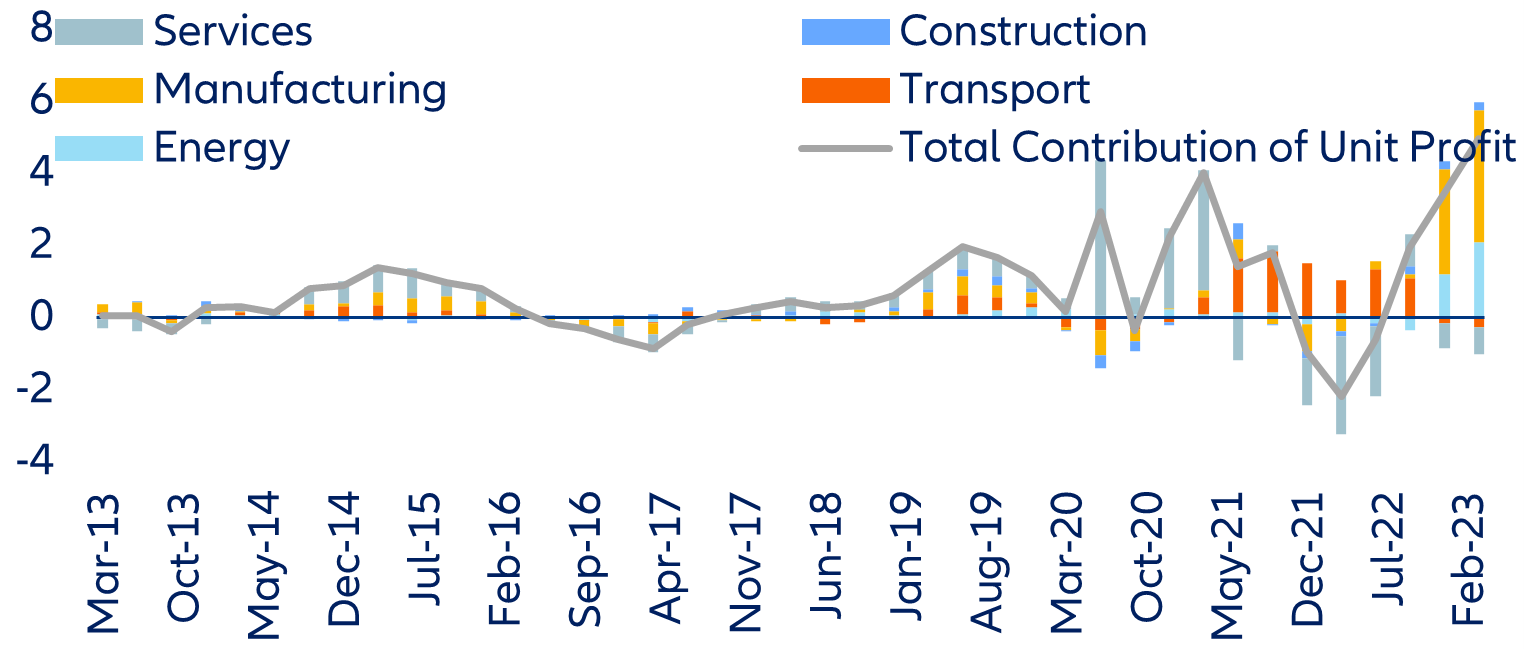

Profits are an increasingly large driver of French inflation despite a depressed margin rate: transportation services, energy and manufacturing contributed to profit-led inflation, while services had a pull-down effect. We break down the contributions of unit labor costs, unit margins, unit taxes, the terms of trade (i.e. the difference between export prices and import prices) and other factors to CPI inflation (Figure 22). We note that, on average, between Q4 2021 (just prior to the war in Ukraine) and Q1 2023, the contribution of unit margins to CPI inflation was nil. Unit labor costs contributed 50%, the terms of trade 27% (owing to a spike in import prices) and taxes 20%. However, on a sequential basis, the contribution of profits to inflation turned positive since Q3 2022. In Q1 2023, unit margins contributed 2.8pps to inflation (which was +6%), around the same as labor costs, while the contribution of the terms of trade eased to 0.8pp. The fact that margins are increasingly contributing to inflation despite a subdued margin rate is because the gross operating surplus is nevertheless growing much faster than output volume, pushing up the price contribution of margins.

Figure 22: France’s CPI inflation breakdown (% y/y)

Sources: Insee, Allianz Research

Looking at the decomposition of unit profits by sector (Figure 23), we note that the contribution of manufacturing and energy sector margins to total unit profits has soared over the past two quarters, while unit profit in the services sector remains depressed. Overall, since the war in Ukraine in early 2022, transportation services, energy and manufacturing contributed to profit-led inflation, while services had a pull-down effect.

Figure 23: France’s unit margin breakdown, contribution to CPI inflation (% y/y)

Sources: Insee, Allianz Research

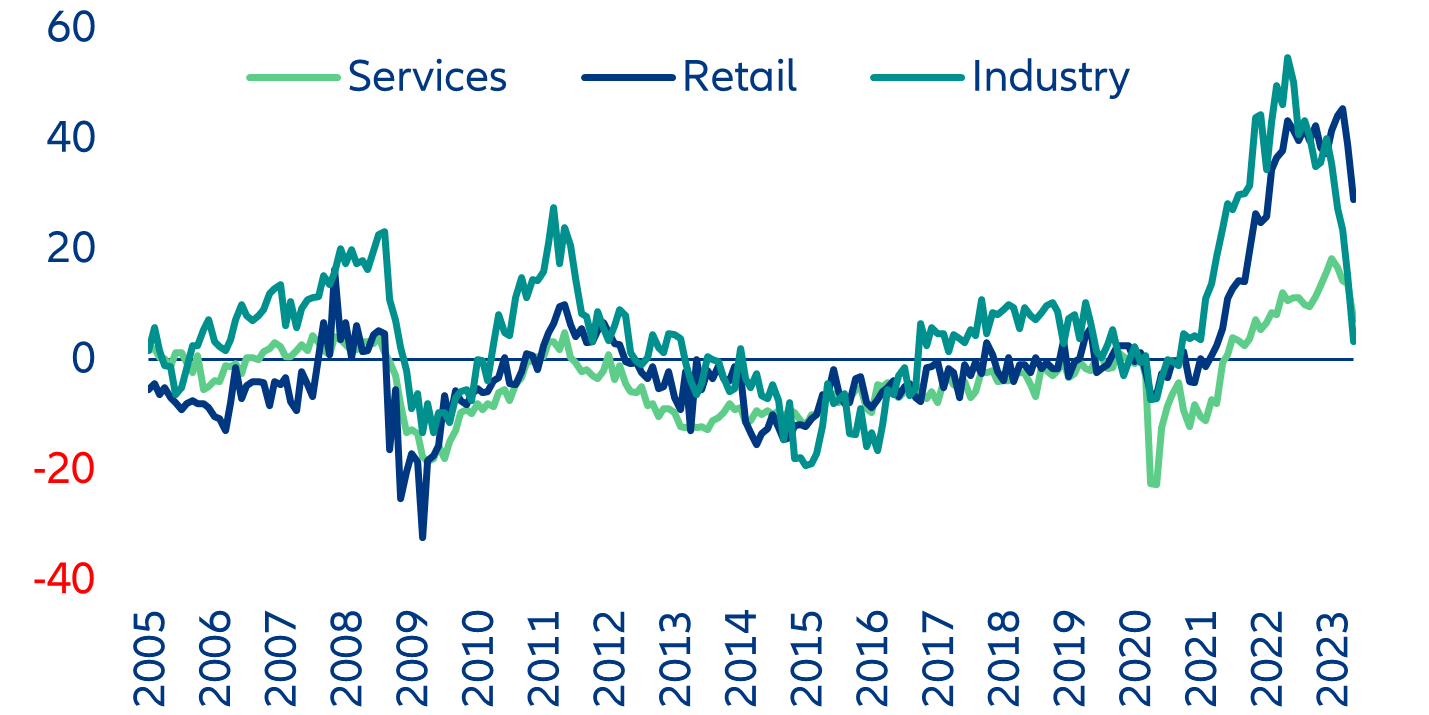

The margin catch-up in the services sector should keep services inflation sticky this year. The latest PMI surveys on prices suggest that margins started to recover in Q2 2023 in the services sector amid easing input costs (such as energy) and improved global supply conditions. According to the latest ESI surveys, corporates in the services sector plan to keep selling prices elevated in the months ahead (Figure 25), which should support margins. Accelerating wages should, however, put a lid on large margin expansion. Overall, we expect the partial catch-up of services margins to limit the decline in services price inflation this year.

However, in other sectors (food industry, manufacturing, energy and retail), we expect some margin squeeze by the autumn, which should contribute to push down headline inflation toward +4-4.5%, from +5.1% in May. Corporates in the retail and manufacturing sectors already expect to ease their selling prices in the months ahead (Figure 24). While for now cooler selling prices largely reflect sharply lower input prices and the ending of supply-chain disruptions, we expect margins to take a hit from the autumn. Demand for manufacturing goods has been declining since mid-2022 and we expect further falls in the months ahead as goods consumption is typically more sensitive to tighter financial conditions than services consumption. Retail manufacturers in particular will be forced to take a margin squeeze as high inventories need to be depleted. In the food industry and retail, we also expect some margin squeeze amid public and government outcry over elevated margins. This should contribute to the rapid deceleration in food inflation that we expect from end-2023. Lower food inflation will be the main pull-down factor to headline inflation by end-2023, dragging it down by around 1pp between May and Q4 2023.

Figure 24: Businesses’ selling prices expectations next three months

Sources: European Commission, Allianz Research