After a decade of pension reforms in Western Europe and the establishment of new systems in Eastern Europe and Asia, the structure of a retirement income for individuals has begun to change. The recently published Allianz survey, “Allianz Demographic Pulse” reveals, that the second and third pillars, income from financial assets and employment – as well as the rise of the elderly in the workforce – are gaining importance. Nevertheless, currently it is not clear whether the complementary incomes are strong enough to compensate for decreasing levels in the first pillars in absolute terms. “For future retirees to achieve retirement income levels comparable of those of today’s retirees, they will have to change their working and savings behavior. The individual must take more responsibility to arrive at an adequate retirement income and Rethink Retirement”, says Jay Ralph, Chairman of Allianz Asset Management and a member of the Board of Management of Allianz SE.

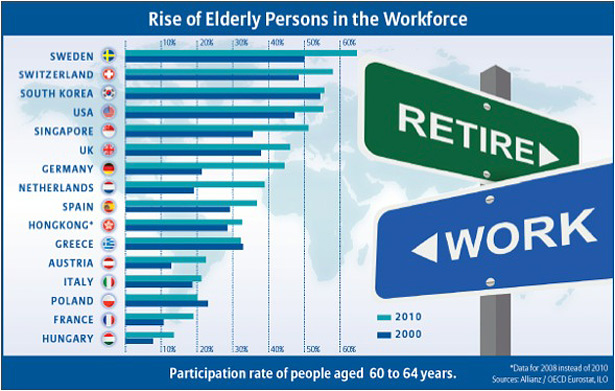

Participation rate of people aged 60 – 64 years has risen

The financial crisis put the changing structures of pension provisioning systems to the test and the reform path is still feeling the pressure of the debt crisis, high volatility of markets and low interest rates. The challenges that this environment poses for funded pillars are considerable. In other words, it is not only the increase in retirement ages that has had an influence on the number of people staying longer in the workforce; so have the setback of pension assets and the need to save longer for retirement. Whether in Europe, Asia or the United States, the participation rate of people aged 60 – 64 years has risen over the last ten years. In Europe, the biggest increase can be observed in Germany and in the Netherlands, where participation rates more than doubled.