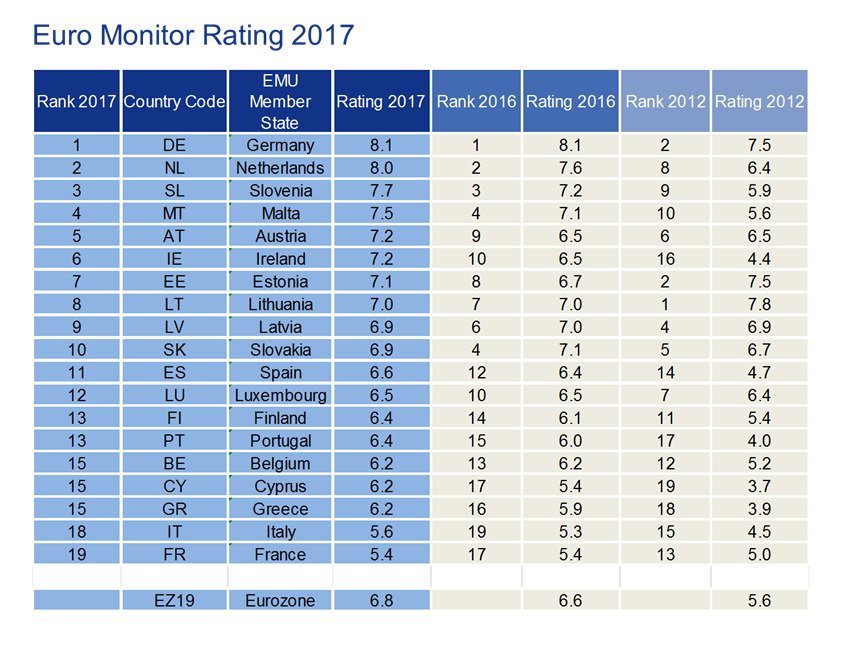

From an economic point of view, the eurozone could hardly be in better shape than it is today. The upswing seems likely to continue, the peak has just begun. This development is reflected in the results of this latest Euro Monitor, with which we measure the state of the euro economies on the basis of 20 indicators every year. The average rating for the euro area now stands at 6.8 points in the good midfield of the scale of one to ten. Furthermore, no EMU country is located in the critically defined depreciation area (1-4 points).

The strong improvement in the overall indicator since 2012 is not only due to the recent economic upswing, but also in particular to the crisis-related structural reforms of the labor and product markets in the former programme countries.

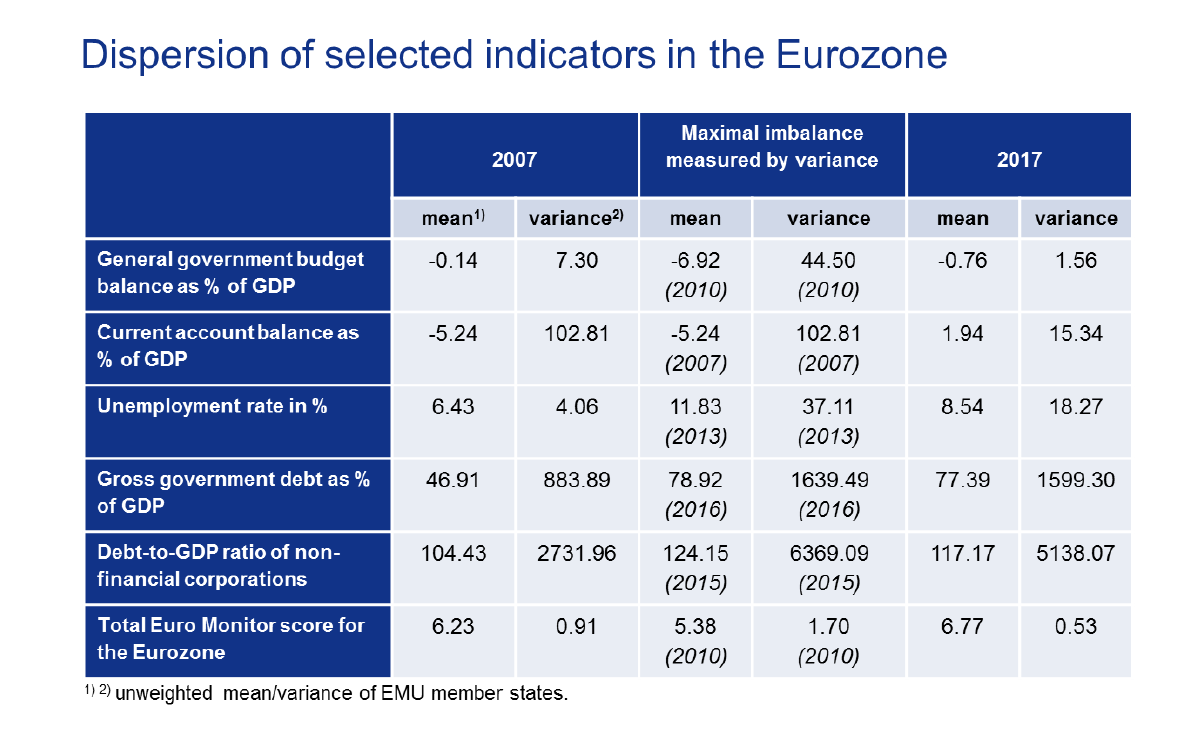

Macroeconomic imbalances have been reduced and, above all, the internal adjustment mechanisms of the monetary union have been strengthened in the long term by higher wage and price flexibility. This should also increase the convergence of key macroeconomic variables, which is the most important prerequisite for a stable currency area. The Euro Monitor data supports this thesis.After the harsh setbacks in the crisis years, the economic rapprochement of the EMU members has intensified again. Although the development of the individual indicators was not uniform, according to our calculations the economic divergence between the national economies is even lower today than it was before the crisis.

“The thesis of many critics that the necessary adjustment processes in the euro area cannot take place due to political or social constraints can be refuted. The crisis of the years around 2012 was not caused by the monetary union itself, but triggered by the misguided policy mix in some countries, which in turn resulted in excessive debt, foreign trade deficits and a loss of competitiveness. The problem was not the currency, but economic and fiscal policy,” said Michael Heise, chief economist at Allianz.