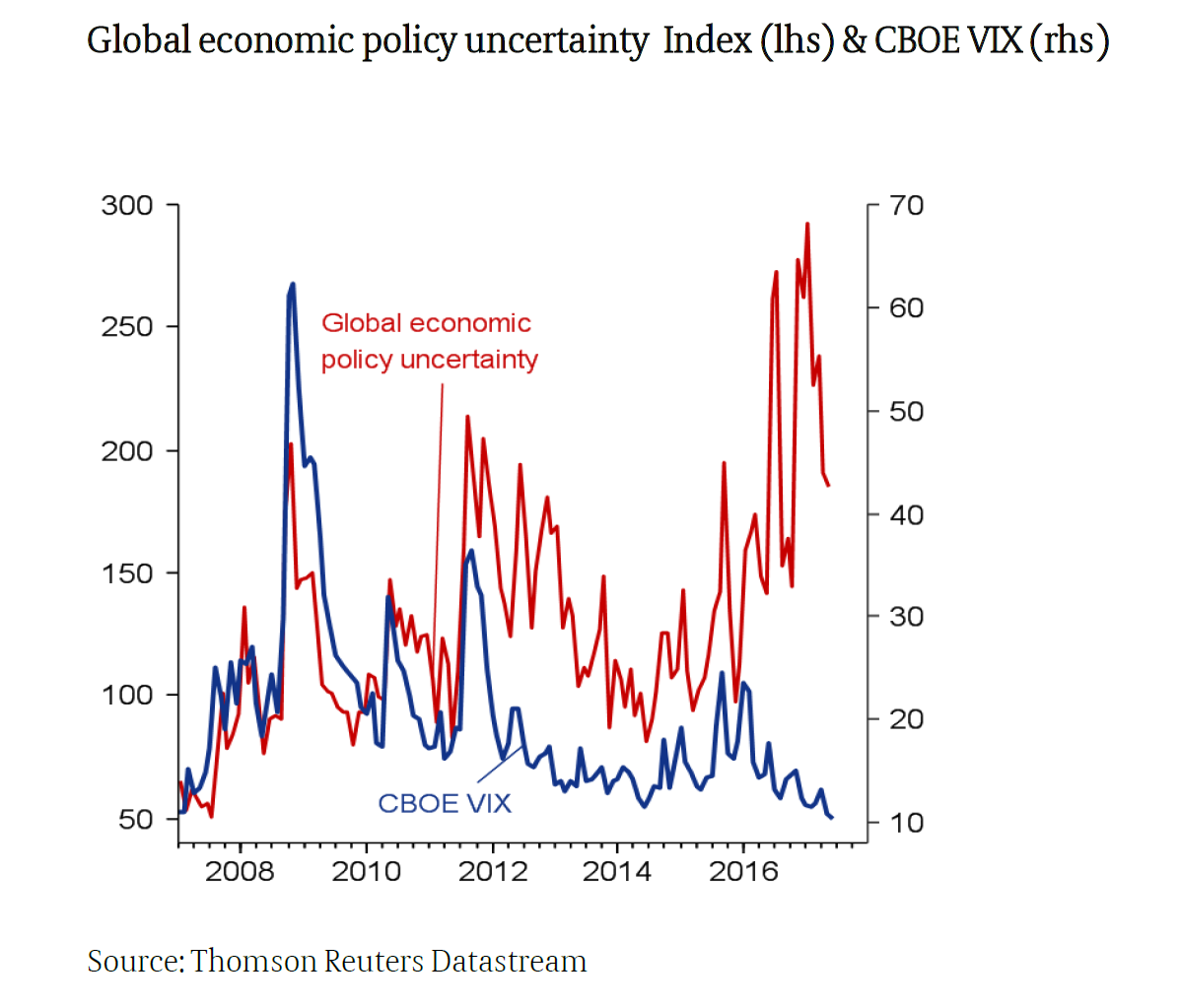

Higher uncertainty is often associated with a broad-based decline in economic activity, and in particular private investment. Also, studies suggest that political uncertainty can have as big an impact on economic outcomes as actual political events. Despite various uncertainties, the global economy is in its best shape for ten years. Positive economic news seems to dominate over worrying political developments in investors’ minds. Why is this the case? There are various reasons for this, in our view. These factors partly reinforce each other.

• None of the current political risks are immediate or tangible enough to trigger a big confidence shock in face of strong economic data.

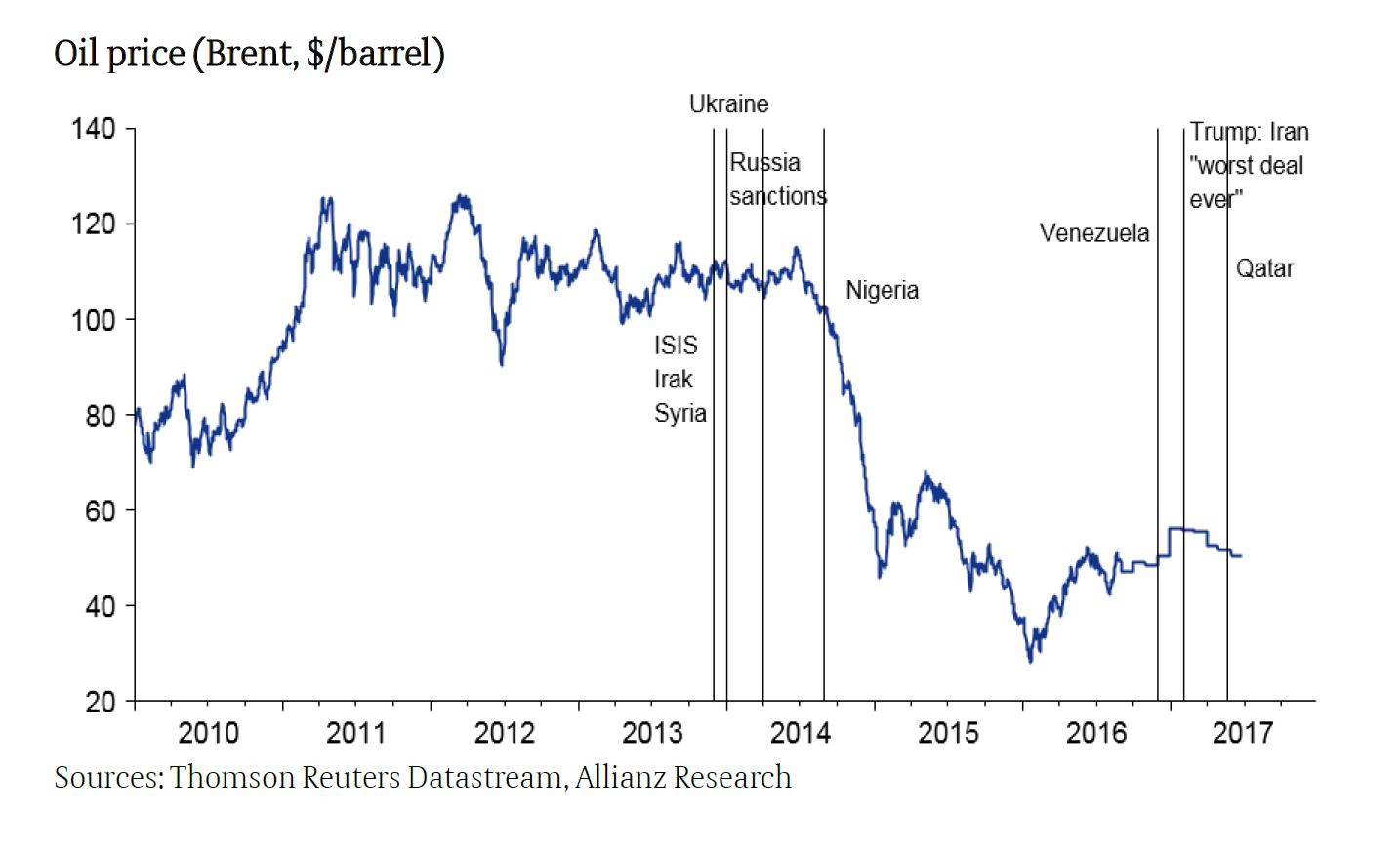

• While ongoing wars and tragedies in the Middle East and parts of Africa may create a sense of gloom, the turmoil in geopolitics has had little impact on global economic prospects. Taken together, the most unstable regions in the world, make up less than 10 percent of the global economy.

• The rise of populist forces worries many, but historically populist economic policies have often been good for growth and markets, at least in the short term. This certainly seems to be the case in the U.S., where Donald Trump’s promises of tax reform, deregulation and infrastructure spending have created a positive confidence shock, especially among investors and small busi-nesses.

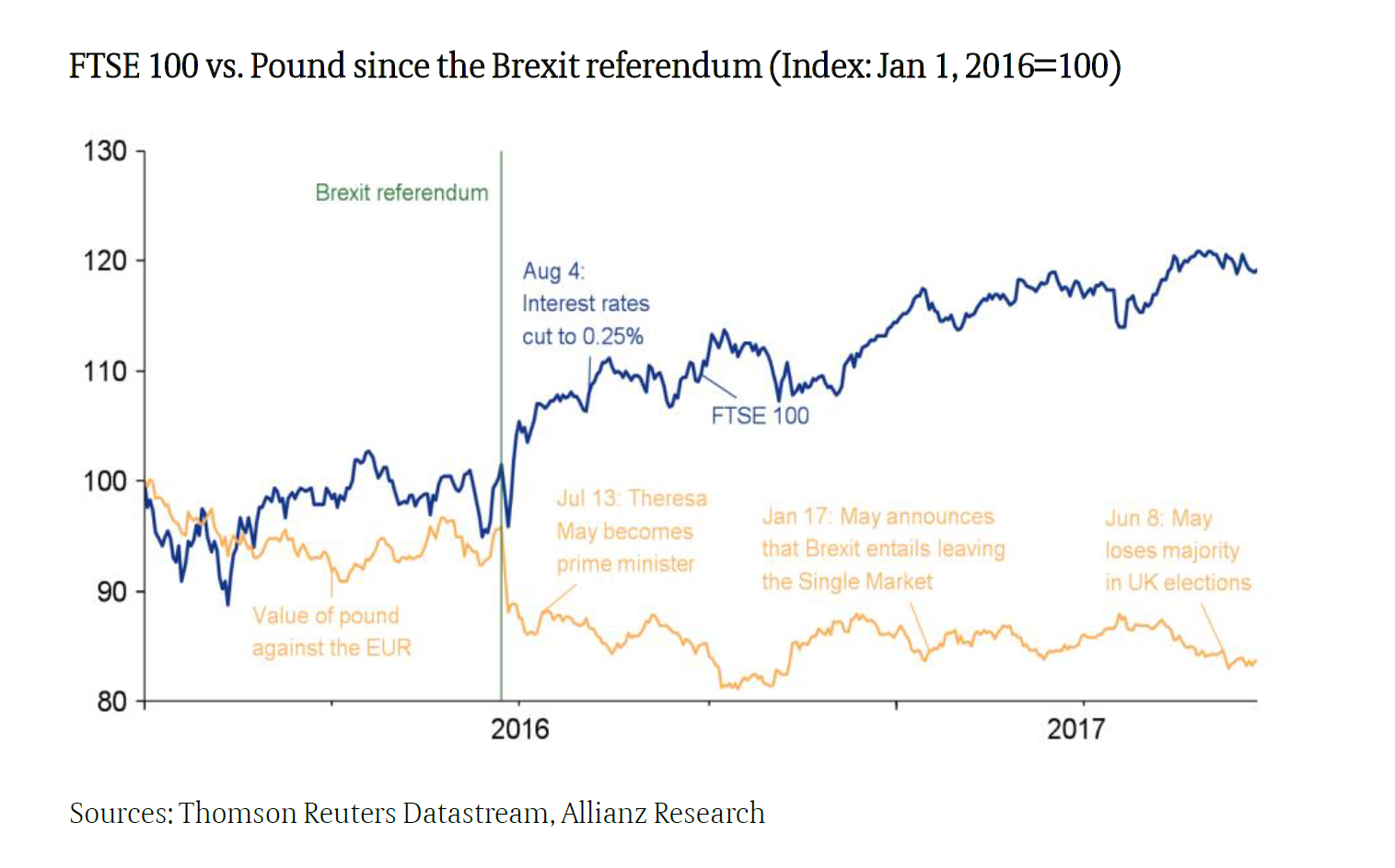

• The Brexit vote came as a shock to many. But Brexit is a process not an event, so the vote itself did not affect economic fundamentals. The Bank of England stepped in quickly to quieten nerves, while the swift government handover also helped to shore up confidence.

• For every political shock, there was one risk that did not materialize, allowing investors to relax and focus on economic fundamentals.

• Market euphoria, in turn, feeds economic confidence, creating a virtuous circle to some extent.

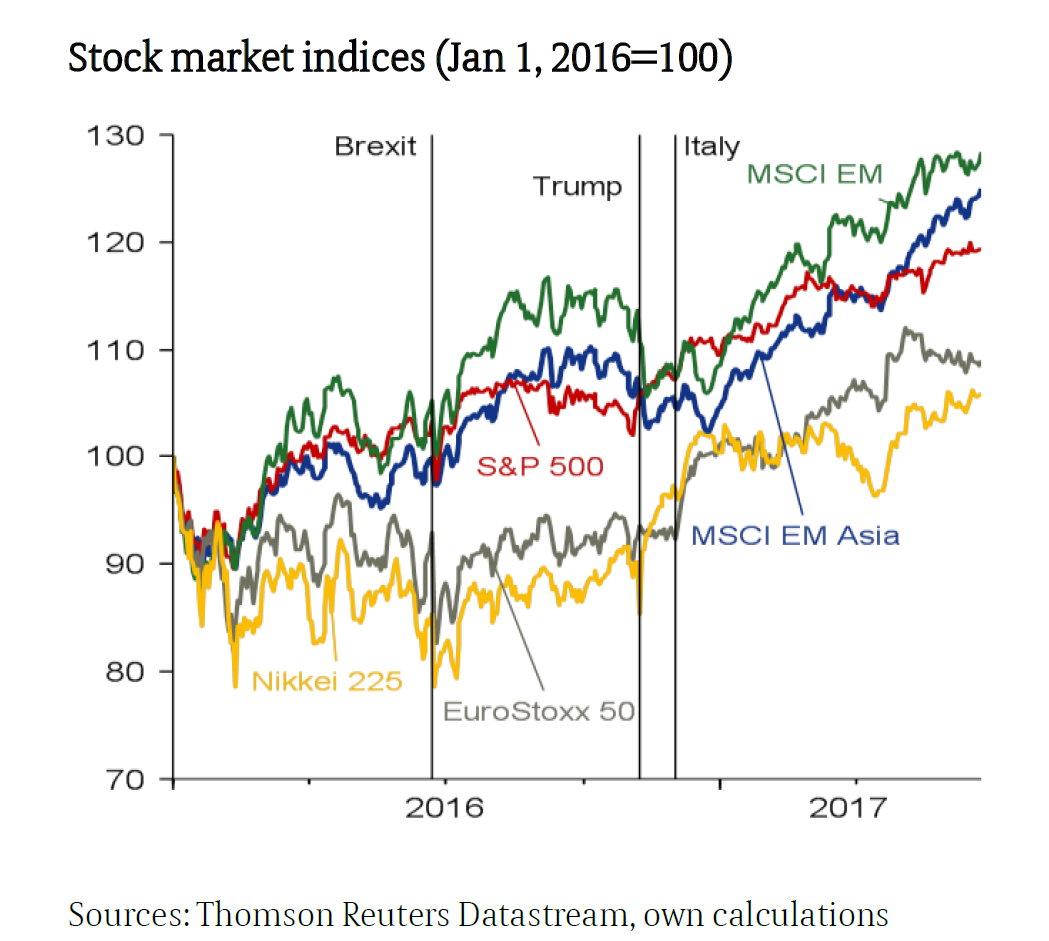

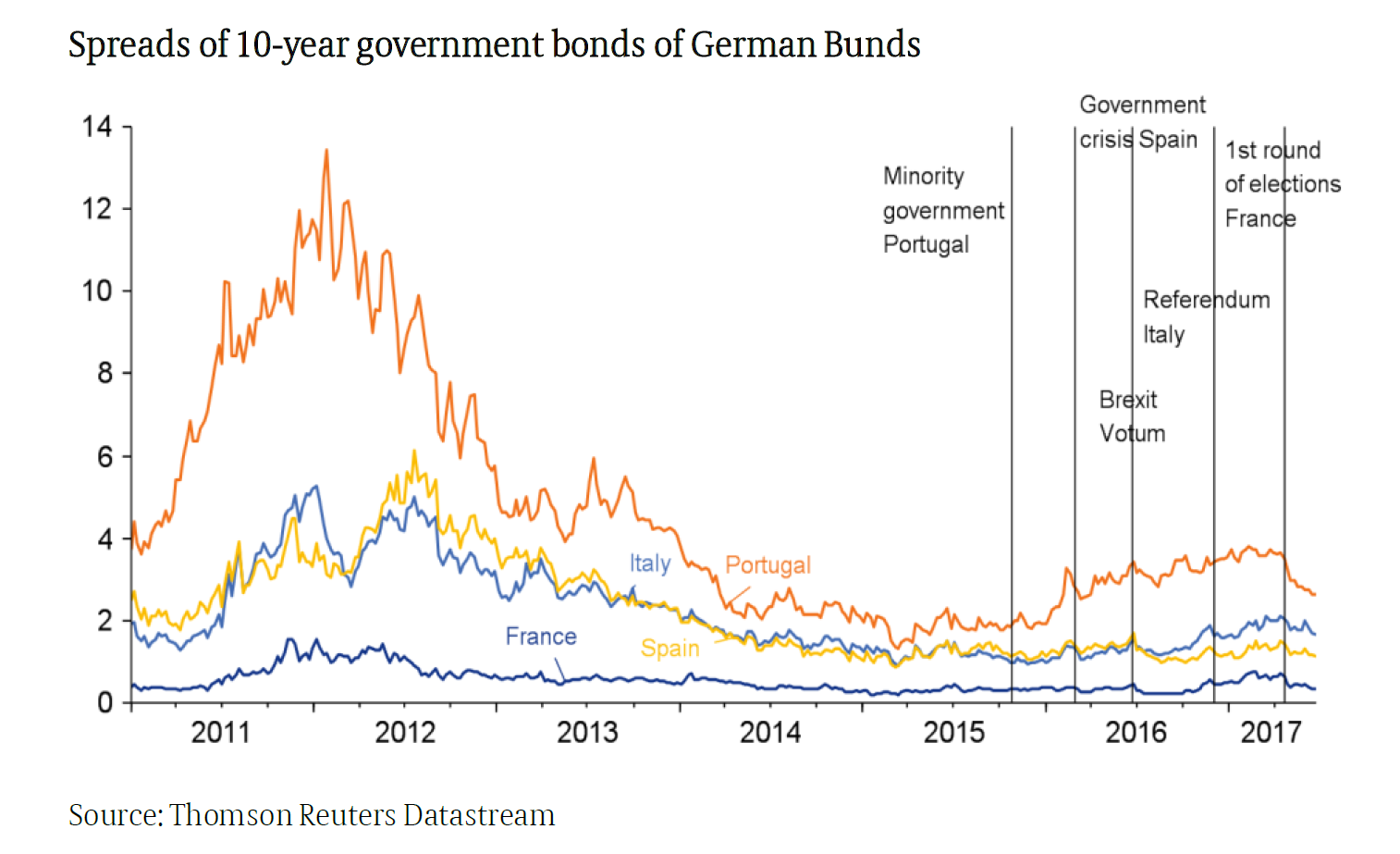

Immediate political risks in Europe are receding after the Dutch, French and British elections returned mainstream governments, although Italy remains a concern for many investors. In the U.S., investors will continue recalibrating the balance between upside and downside risks associated with the Trump presidency. The assumption is, however, that there are few plausible political scenarios that could derail the current economic upswing. Those that could do so, such as a military confrontation with North Korea or a massive cyber attack on the U.S., are in the realm of tail risks that are too vague or far-fetched to affect economic confidence directly.

Looking into the future, if and when the global cyclical recovery peaks, economic fundamentals will no longer provide such solid support for rising markets. A sharp market correction looks unlikely, in our view, given that we do not detect a broad-based credit boom or major imbalances, while global capital flows appear moderate. Nevertheless, investors will have to adjust their expectations downwards. The real test for financial markets will come once other major central banks follow the Fed’s lead and start normalizing monetary policy.