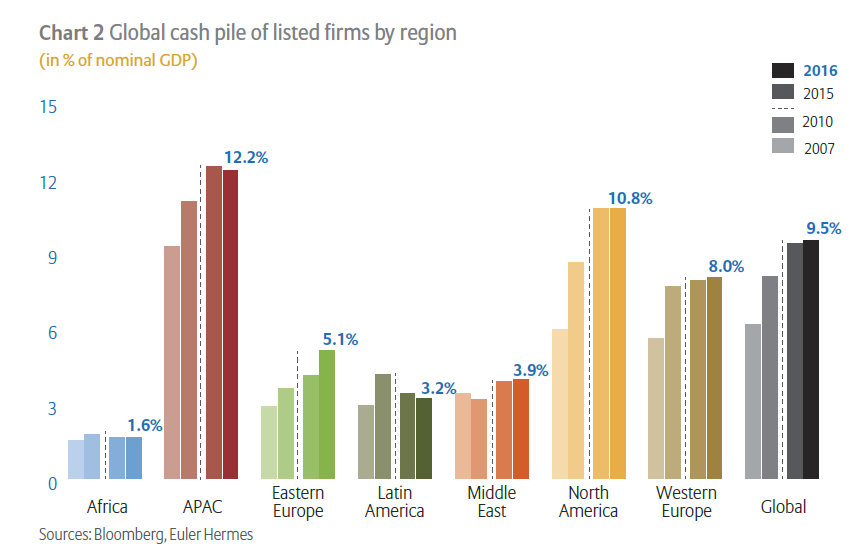

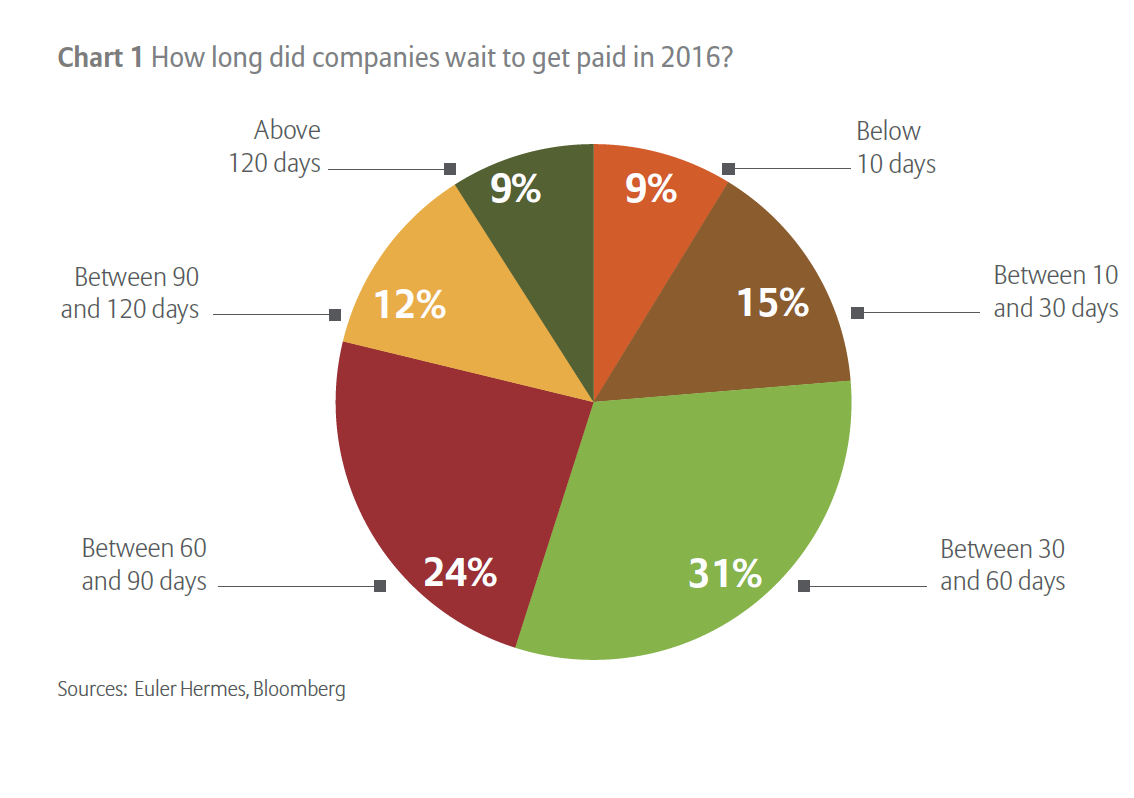

Despite a new record being set for non-financial company cash hoarding, continued high payment delays and a sharp rise in major insolvencies (companies with > 50 million euros turnover) demonstrate that global economic momentum is not without its challenges, according Euler Hermes, the world’s leading trade credit insurer.

In its latest Economic Outlook report, titled “High Stakes Games”, the company’s economic research department:

- measured cash accumulation across 30,500 listed companies in 94 stock markets;

- analyzed insolvency levels in 43 markets;

- explored payment behavior from a Bloomberg panel of 27,000 listed companies worldwide.

“Against the backdrop of overall global stability and with economic recovery finally beginning to gather steam, lurks a high degree of divergence and risk,” said Ludovic Subran, chief economist at Euler Hermes. “This becomes increasingly extreme as concentration of cash in some regions and industries sets new records, and the severity and frequency of major company failure rises."

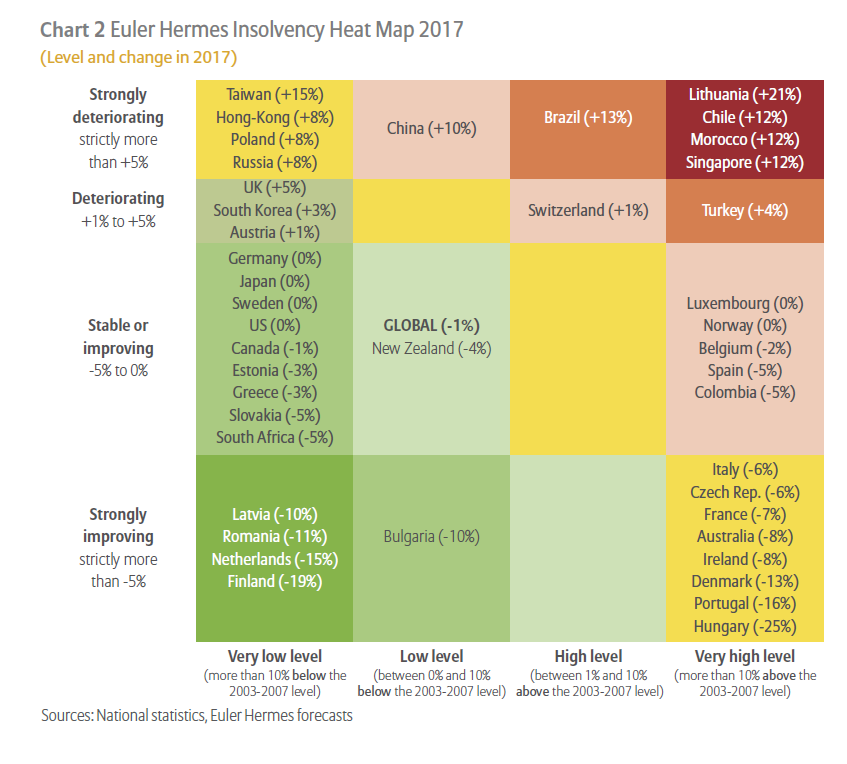

“From major insolvencies in the retail and services sectors, particularly in the U.S., increasing bankruptcies in China and Brazil through to extended payment delays in China and the Aeronautics sector worldwide -- this adds up to bigger tail risks. The severity and frequency of extreme cases is on the rise and will need to be carefully monitored in the months ahead,” added Subran.