In its latest study, Allianz SE and Euler Hermes analyze the impact of monetary normalization on debt service payments of the private sector in the eurozone. In contrast to the public sector (and big companies), the bulk of smaller companies and households cannot shield themselves against rising rates by issuing long-term debt, locking in current ultra-low interest rate levels. For them, dependent on bank loans, the “pass-through” is much faster; in fact, even today roughly 80 percent of new corporate bank loans have a rate fixation of less than one year (if at all); the notable exception relates to mortgage loans in a number of eurozone countries, including Germany.

We use regression analyses to estimate how an increase in the European Central Bank (ECB) key interest rate will impact average interest rates on bank loans for households and the corporate sector. In doing so, we have built three scenarios for the development of the ECB key interest rate up to 2022. Our base scenario is one of “soft normalization,” with the ECB only starting to hike the key rate from 2019 onwards; the other two scenarios are called “moderate” and “hard normalization”. Based on our assumptions, the key rate would reach 2 percent at end-2022 in the base scenario, 3 percent in the second and 4.25 percent in the third scenario. At the same time, we have assumed that the years of deleveraging have also come to an end: with the moderate recovery in the euro area continuing, private debt will rise in sync with overall economic activity.

“The days of extremely low interest rates are numbered,” said Michael Heise, Chief Economist at Allianz SE. “So fears in the market are growing that the withdrawal of cheap money could bring the economy crashing down – because it rests on a foundation of debt and economic players are hooked on the "drug" of cheap money. But our study clearly shows: the additional interest burden for the private sector in the eurozone remains moderate on the whole. It is certainly not an excuse for continuing to print money: from this perspective, there is nothing standing in the way of a return to normal monetary policy.”

Rising interest rates: Nothing to fear but fear itself

Downloads

Related links

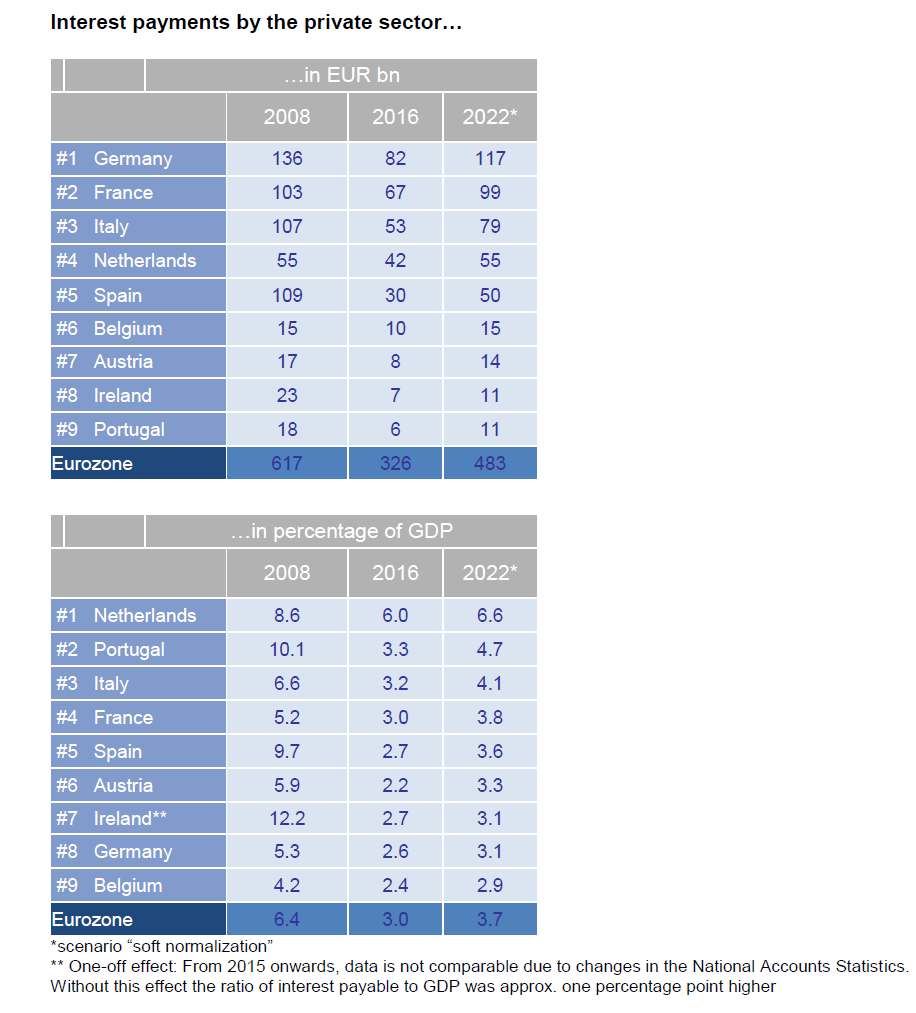

In contrast to the public sector, the private sector has taken the last few years as an opportunity to whittle down its debt level. In relation to economic output, private debt in the eurozone has dropped back by no less than 16 percentage points since reaching its peak in 2009. In combination with ultra-low interest rates, this resulted in a significant drop in interest payments: The debt service ratio (interest payments expressed as a percentage of GDP) dropped by 3.4 percentage points to only 3.0 percent; this was also down considerably on the values for the pre-crisis years when it hovered around 5 percent and higher. The absolute numbers are eye-watering: the annual payments fell by around 300 billion euros between 2008 and 2016; on a cumulative basis, the private sector “saved” roughly 1,550 billion euros in these eight years. “All in all, the ECB did a lot to support private debtors”, said Kathrin Brandmeir, economist at Allianz SE and co-author of the study. “The relief for private debtors was most pronounced in the crisis countries: In relation to GDP, besides Ireland, Spain and Portugal reaped the greatest benefit from the drop in interest rates, with their interest burden falling by around seven percentage points. On the other hand, the relief for the core EMU countries, Germany, the Netherlands, France and Belgium, has been much less pronounced, but substantial nonetheless at 2.3 percentage points on average.”

However, in the future, interest rates and debt levels will increase again. This will naturally result in higher debt service payments for the private sector. This will not, however, simply mean that the previous relief is "reversed". Even in the least favorable scenario of “hard normalization”, the interest payments will "only" increase by roughly 280 billion euros – this means that, even 14 years down the line, in 2022, their absolute value still falls short of the level reached at the peak of the credit boom in 2008. In the more likely event of “soft normalization”, on the other hand, interest payments are only expected to increase by around 160 billion euros, leaving them almost one quarter lower than in 2008 in absolute terms. In relation to economic output, the increase in the euro area is likely to come to between 0.7 (“soft”) and 1.6 percentage points (“hard”), reaching 3.7 percent or 4.7 percent respectively. The upshot: for the eurozone as a whole, the relative interest burden is set to stay not only below the peak in 2008, but also generally lower than in the years before the crisis – even in the risk scenario.

However, the average number masks rather huge differences between the eurozone members. Portuguese households are in for a rather bumpy ride. For them, the increase in interest payments could be – in the risk scenario – a hefty 4 percentage points of disposable income, more than doubling the relative interest burden.

Turning to the corporate sector, French and Italian companies are the most exposed to rising interest rates, for two reasons: Interest payable as a percentage of operating surplus is already high, well above the European average, and the expected increase is also rather sharp. However, even in the most adverse scenario, the relative interest burden of French and Italian companies will remain comfortably below the peak in 2008. Moreover, the corporate sectors in both countries sit on rather high cash piles as additional buffers. “At the end of the day, a return to rising interest rates will not come as welcome news for private debtors,” said Ana Boata, economist at Euler Hermes and co-author of the study. “The extent to which households and companies in the euro area are affected will vary. All in all, however, the private sector in the euro area has the constitution to digest the normalization of monetary policy. The extra interest burden will not be substantial enough to fuel fears of another economic slump: so there is no reason to fear a rise in interest rates.”

About Allianz

The Allianz Group serves 86 million retail and corporate customers in more than 70 countries, making it one of the world’s largest insurers and asset managers. In 2016, over 140,000 employees worldwide achieved total revenues of 122.4 billion euros and an operating profit of 10.8 billion euros. Allianz Group managed an investment portfolio of 653 billion euros. Additionally our asset managers AllianzGI and PIMCO managed over 1.3 trillion euros of third-party assets. Allianz customers benefit from a broad range of personal and corporate insurance services, ranging from property and health insurance to assistance services to credit insurance and global business insurance. As an investor, Allianz is active in a variety of sectors including debt, equity, infrastructure, real estate and renewable energy. The Group’s long-term value strategies maximize risk-adjusted returns.

Further Information

Forward Looking Statement disclaimer

As with all content published on this site, these statements are subject to our Forward Looking Statement disclaimer: