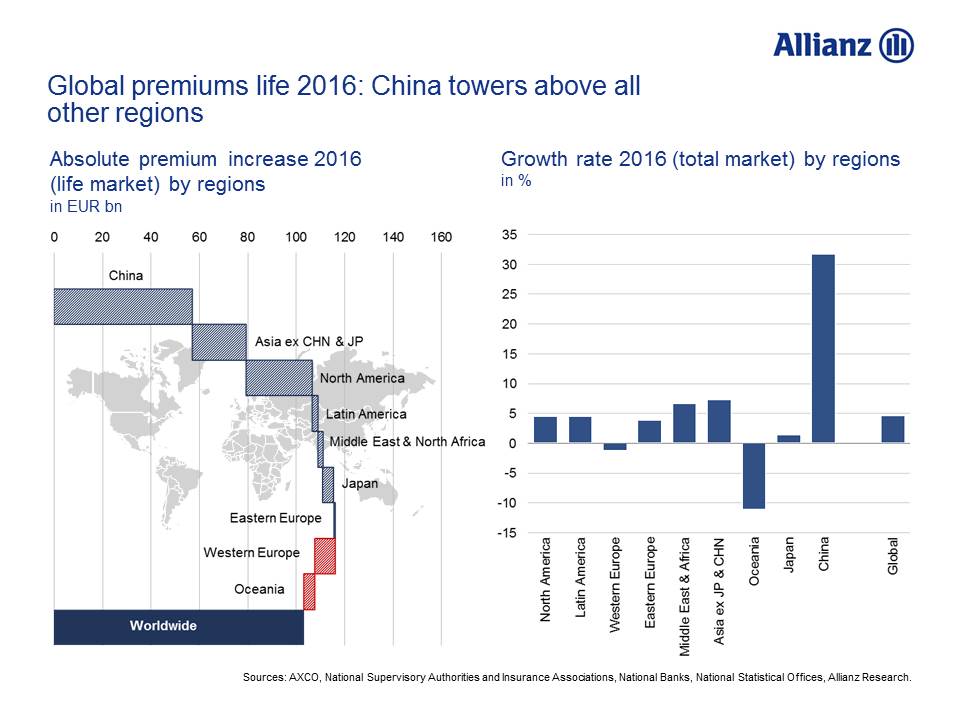

The "China effect" was particularly pronounced in the life insurance business, where excluding the Chinese contribution from the equation would more than halve the rate of global growth from a respectable 4.7 percent to 2.3 percent in 2016. This is due, for one thing, to the rapid development in China itself: last year saw the Chinese life insurance market report the highest rate of growth seen since 2008, at over 30 percent. Although per capita spending on life insurance products (at around 170 euros) still has a long way to go before it catches up with the average for the developed countries, China has already overtaken Austria in terms of the insurance penetration rate, i.e. gross written premiums expressed as a percentage of economic output, and with 2.4 percent is also within striking distance of the Germans, who are often described as real life insurance enthusiasts: the life insurance penetration rate in Germany came to 2.7 percent last year (which, incidentally, is also well below the western European average of 4.7 percent). But this certainly does not signal the end of China's catch-up process.

After all, just like their Chinese neighbors in Hong Kong and Taiwan, where the penetration rates top the international league table at 15 percent and 16 percent, respectively, the mainland Chinese are also having to set an increasing amount of money aside for their old age.

Second, this Chinese dominance can definitely also be attributed to the slump on the life insurance markets elsewhere in the world. In western Europe, premium income is expected to have dropped by 1.2 percent overall in 2016, the first negative trend seen since 2012. And this certainly isn't a predicament that is limited to western Europe.

The markets also contracted in parts of eastern Europe (i.e. in Poland and the Czech Republic, both for the fourth year running) and Australia (for the second year in a row) last year. On the other hand, Russia, Turkey and many of Asia's emerging markets - India, Indonesia and Vietnam for example - are reporting double-digit growth rates, with the US also reporting solid development. This means that, all in all, global premium income in the life insurance sector increased by an estimated 4.7 percent to total 2,300 billion euros.