Allianz International Pensions has created the Retirement Income Adequacy (RIA) Indicator, which ranks 49 countries according to their potential to provide an adequate retirement income for future retirees. It analyzes a number of income sources (state, occupational, private pension, financial assets, real estate) as well as spendings relevant in old age, such as out-of-pocket expenses for health care.

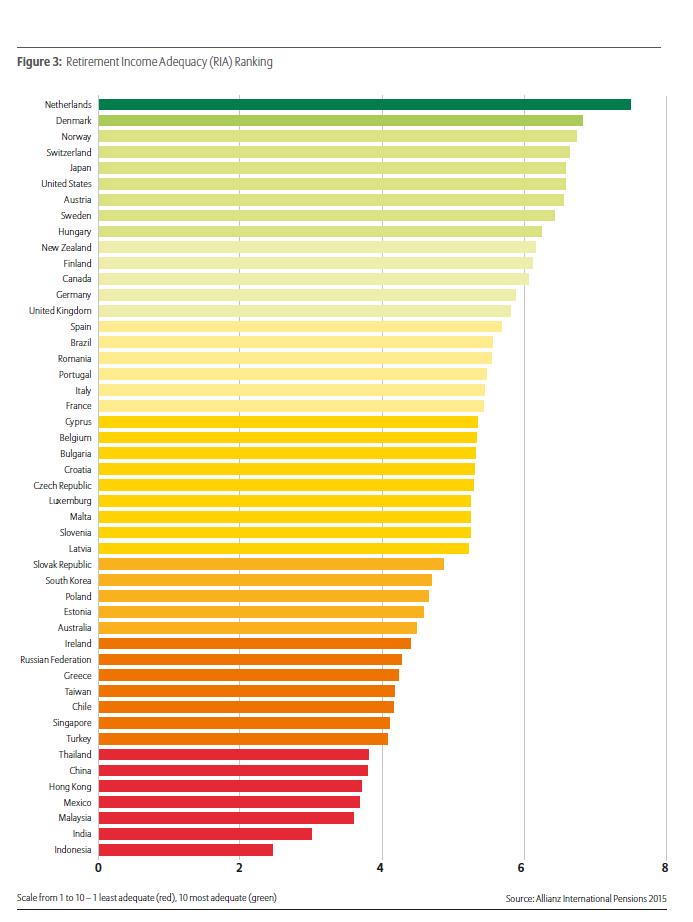

Pension systems with mature funded and balanced state, occupational and private pillars rank at the top, meaning that it is highly likely such systems can provide an adequate retirement income. Top 3 are the Netherlands, followed by Denmark and Norway. Germany is ranked in the middle of Western European countries and in the top thirteen overall. At the bottom of the list are developing countries without comprehensive pension systems: Indonesia and India score lowest, Malaysia a bit higher. A couple of countries in between are characterized by just one strong pillar (state, occupational or private pension), Austria is an example.

Rethink retirement income streams

“We already know that diversification of retirement assets is crucial for savers”, says Dr. Renate Finke, Senior Economist at Allianz International Pensions and author of the study. “Thus the RIA approach not only focuses on one factor of the retirement income, let’s say the state pension, but provides an integrated view across all income streams. Why? Because pension provision has become a delicate balancing act between keeping the public pensions systems financially sustainable (compare: Pension Sustainability Index) and ensuring a certain level of retirement income for future generations.”

Governments have undertaken reforms that will generally leave people with lower retirement income relative to pre-retirement income compared with today’s pensioners. In the future, pensioners’ income mix will differ: the previously dominant state pensions are giving way to funded elements; the emphasis on defined benefit plans is shifting towards defined contribution schemes and family support structures are moving towards more formalized public ones.

But the question remains the same: How much retirement income is enough? “There is no ‘one-size-fits-all’ answer”, explains Finke. “Some countries define adequacy as a social standard, such as the poverty line or as a percentage of pre-retirement income, in others it implies maintaining a certain standard of living.”